20 Feb 2025 - {{hitsCtrl.values.hits}}

By First Capital Research

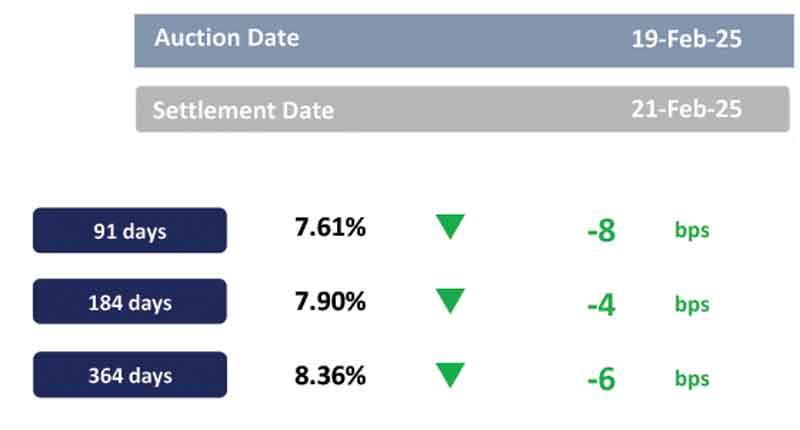

At yesterday’s weekly T-bill auction, the weighted average yields registered a marginal dip.

The weighted average yield rates for the three-month, six-month and 12-month bills stood at 7.61 percent, 7.90 percent and 8.36 percent, respectively, reflecting auction yield drops of 8bps, 4bps and 6bps, respectively.

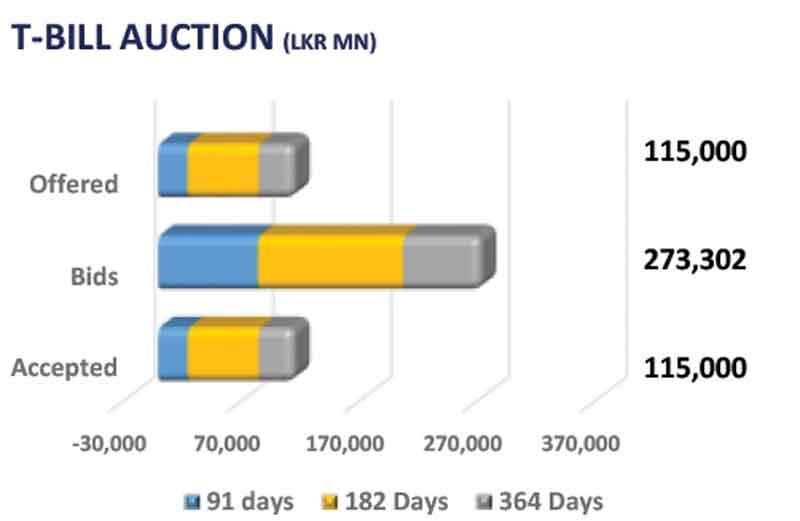

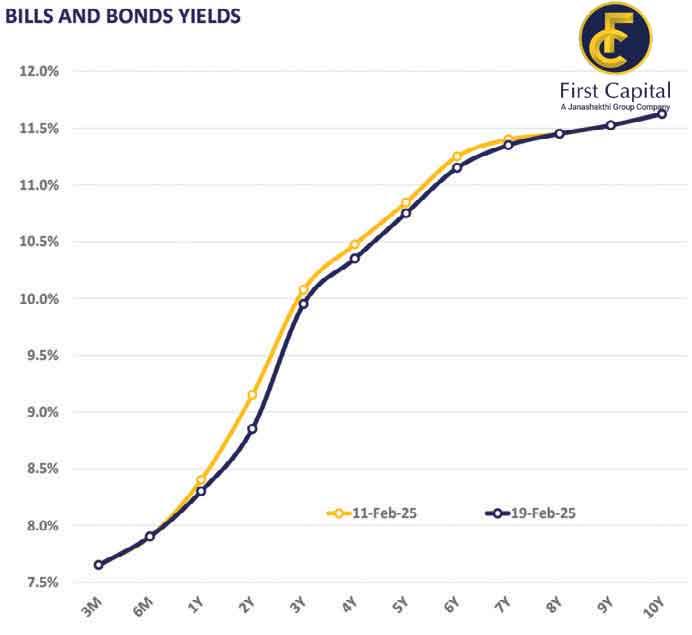

Furthermore, the Central Bank offered a total of Rs.115.0 billion worth of T-bills collectively and this amount was fully subscribed. In the secondary market, participants maintained their buying momentum from the previous day, resulting in both high trading volumes and increased market activity. Amongst the traded maturities in the short end 01.08.2026 and 01.05.2027 maturities traded at 8.65 percent and 9.25 percent, respectively.

Whilst both bond maturities, 15.09.2027 and 15.10.2027 traded at the range of 9.55 percent to 9.45 percent. Towards the belly end of the curve, both 15.02.2028 and 15.03.2028 traded at the rate 10.00percent, whilst 01.05.2028 traded between 10.15percent to 10.07percent.

Furthermore, the 01.09.2028, 15.10.2028 and 15.12.2028 bonds traded between 10.35 percent to 10.25 percent. The 15.09.2029 and 15.05.2030 bonds traded at the rates of 10.75 percent and 11.00 percent, respectively.

Additionally, the 15.10.2030 maturity traded between 11.18 percent and 11.15 percent. The Central Bank holdings of government securities remained unchanged, closing at Rs.2,511.92 billion yesterday. Overnight liquidity in the banking system expanded to Rs.164.8 billion, from Rs.146.7 billion recorded the previous day.

18 Jul 2026 2 hours ago

18 Jul 2026 3 hours ago

18 Jul 2026 4 hours ago

18 Jul 2026 5 hours ago

17 Jul 2026 17 Jul 2026