Reply To:

Name - Reply Comment

The long-term insurance sector in Sri Lanka witnessed its lowest premium income growth rate in five years, with ayear-on-year (YoY) performance increase of 9.4 percent recorded in 2022.

ayear-on-year (YoY) performance increase of 9.4 percent recorded in 2022.

The growth rate in premium income experienced a decline, dropping from 12.5 percent in 2018 to 10.6 percent in 2019, then further to 16 percent in 2020, and 21 percent in 2021.

On the contrary, the General Insurance business showed a contrasting trend with the growth rate in premium income showing a growth of 11.9 percent YoY in 2022. From 2018 to 2021, this segment’s premium income growth rate was 7.7 percent, 7.1 percent, -2.3 percent, and 3.5 percent.

In 2022, the General Insurance business recorded an overall premium income of Rs. 121,829 million, with the majority of this reported income attributed to motor insurance.

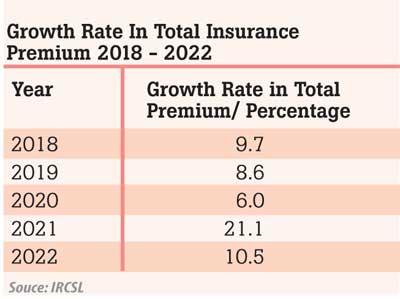

When looking at the total premium income of the insurance sector, a 10.5 percent growth was recorded in 2022, lower than the 12.1 percent recorded in 2021, but higher than the 9.7 percent in 2018, 8.6 percent in 2019, and 6.0 percent in 2020.

“Rising interest rates hampered the loan granting facility and adversely affected the premium growth of loan protection insurance covers,” the Insurance Regulatory Commission of Sri Lanka (IRCSL) said in a statement that highlighted the performance of the industry in 2022.

“The depleted real income of households due to soaring inflation has resulted in a significant drop in new long-term insurance policies issued during the year, resulting in subdued premium growth,” it added.

insurance policies issued during the year, resulting in subdued premium growth,” it added.

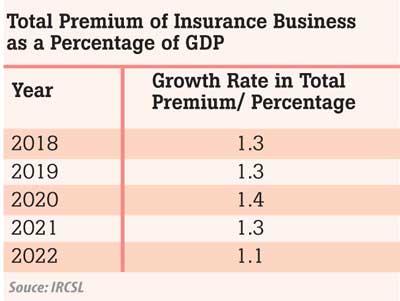

The total penetration of insurance as a percentage of the Gross Domestic Product (GDP) contracted to 1.1 percent in 2022, again, the lowest in five years. In 2018, 2019, and 2021 the penetration was 1.3 percent, while in 2020 the penetration was 1.4 percent.

IRCSL noted that the protection gap is considerably wide in the country which requires proactive measures such as spreading awareness about the benefits of insurance, increasing the accessibility and affordability of insurance services, developing innovative products, improving customer service through technological advancements, etc. to bridge the gap and enhance the penetration level.

“Yet, the implications of current macro-economic turbulence would hamper the growth of the insurance sector in the country mainly as the disposable income of the public has reduced,” it said.

Meanwhile, the insurance premium per person exhibited positive movement from Rs. 10,540 to Rs. 11,636 during the year due to comparatively stable population growth in the country in 2022.

Furthermore, the net claims incurred in the long-term insurance industry recorded Rs. 61,642 million during the year 2022. The growth rate was recorded at 34.1 percent, which is the highest growth rate recorded for the past five years. The increase originated basically from maturity benefits, surrenders, and others.

In 2022, the general insurance industry witnessed a significant increase in total net claims, reaching Rs. 60,172 million (excluding SRCC & T), which indicates a substantial surge of 24.7 percent compared to the amount of Rs. 48,239 million reported in 2021.

According to IRCSL, the claims of the General Insurance sector have witnessed a surge due to multiple factors, including the increase in costs for repairs and replacements resulting from high inflationary conditions in the country.

Additionally, unforeseen riot claims arising from protests have added to the financial burden faced by insurers. Furthermore, the recent lift of pandemic restrictions has resulted in an upswing in mobility, leading to a rise in accidents and subsequent insurance claims, the IRCSL said.