Reply To:

Name - Reply Comment

By First Capital Research

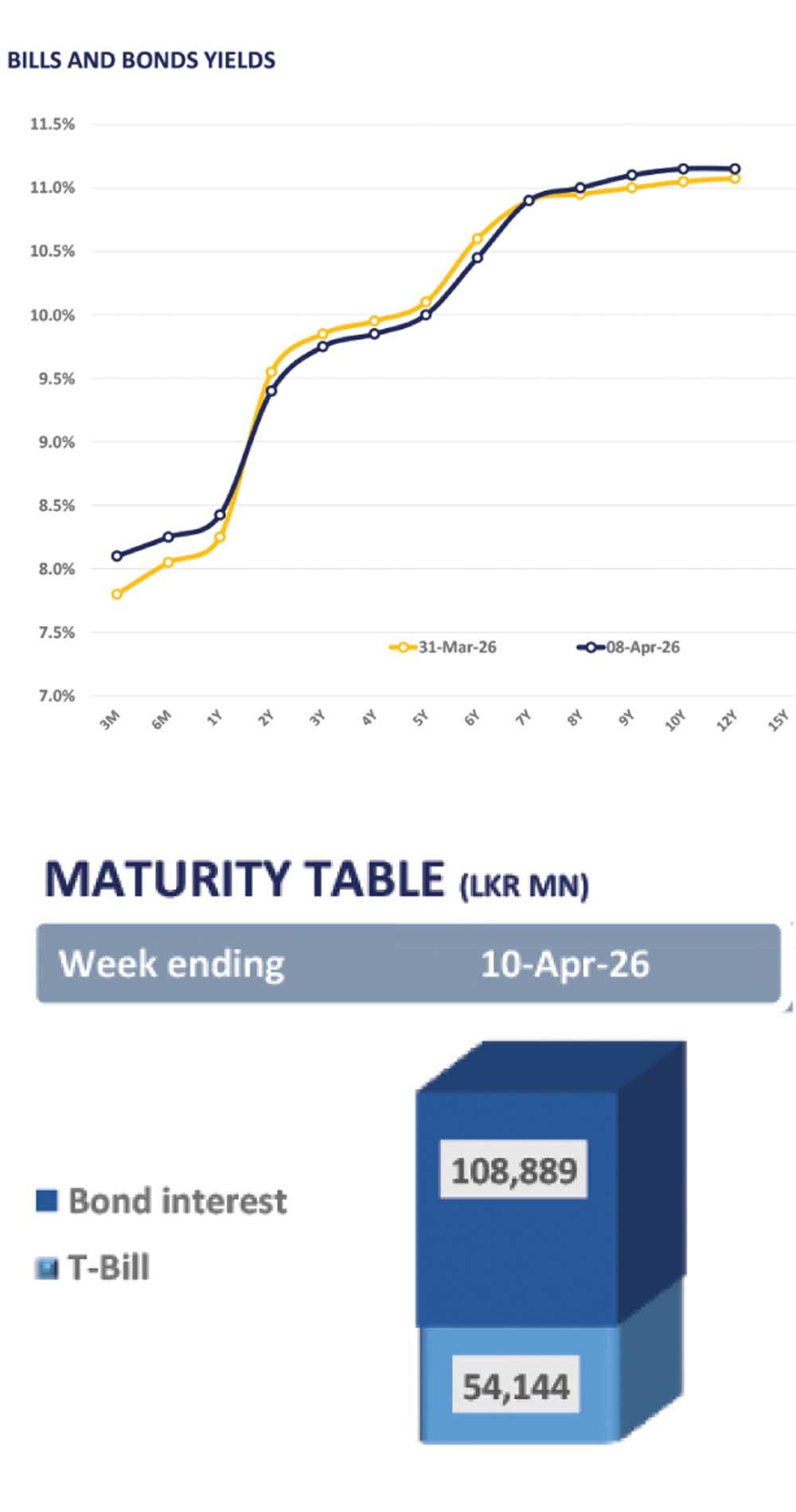

The secondary market witnessed some buying interest yesterday, following the announcement of the US–Iran peace talks and a temporary ceasefire, marking a downward movement in the yield curve.

Among the maturities traded, the 15.06.2029, 15.09.2029 and 15.12.2029 maturities traded between 9.85 percent-9.70 percent. 01.03.2030 and 01.10.2032 traded within the ranges of 9.85 percent - 9.80 percent and 10.65 percent-10.58 percent, respectively.

As the yields edged downward in the short-mid-term maturities, 01.06.2033 and 01.11.2033 were dealt between 10.95 percent and 10.85 percent.

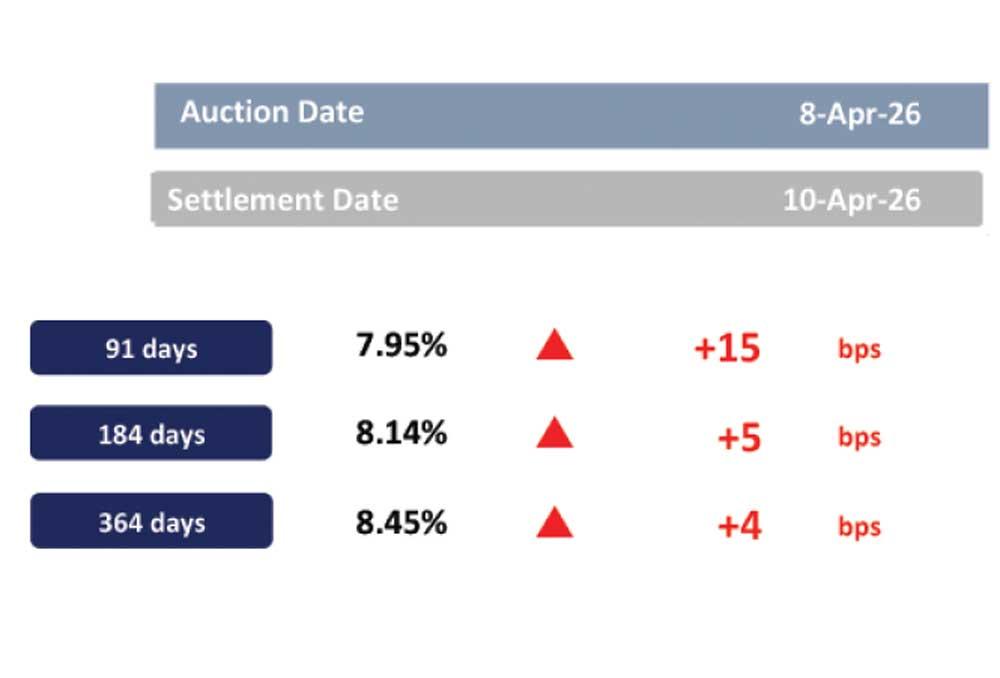

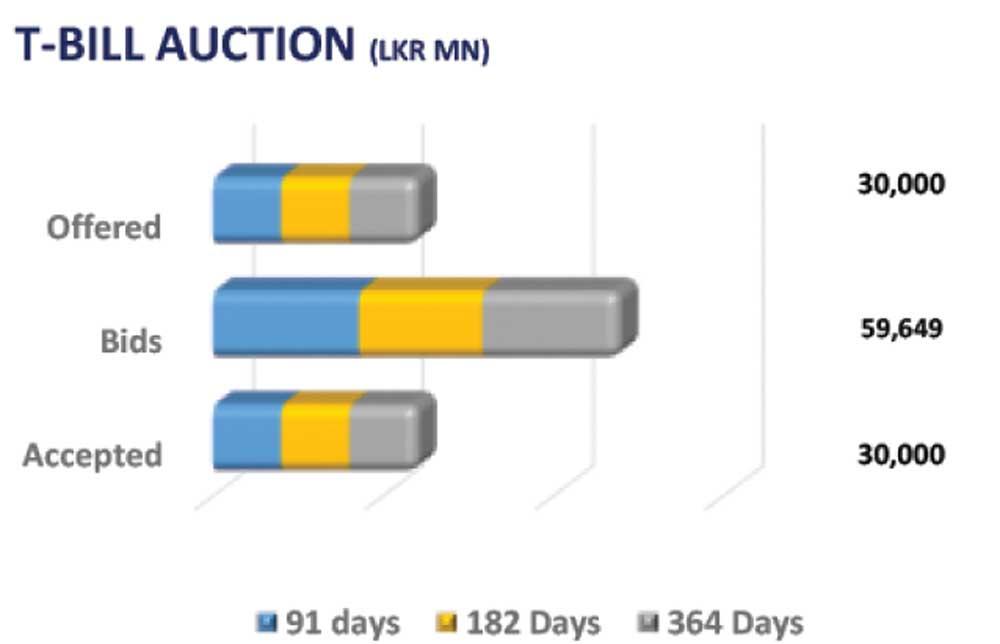

At the T-bill auction, the weighted average yields edged up across all three tenures with the PDMO successfully raising the full offered amount of Rs.30.0 billion.

All three-month, six-month and 12-month maturities were accepted in full, amounting Rs.10.0 billion each. However, the weighted average yields slightly moved up to 7.95 percent (+15bps), 8.14 percent (+05bps) and 8.45 percent (+04bps), respectively.

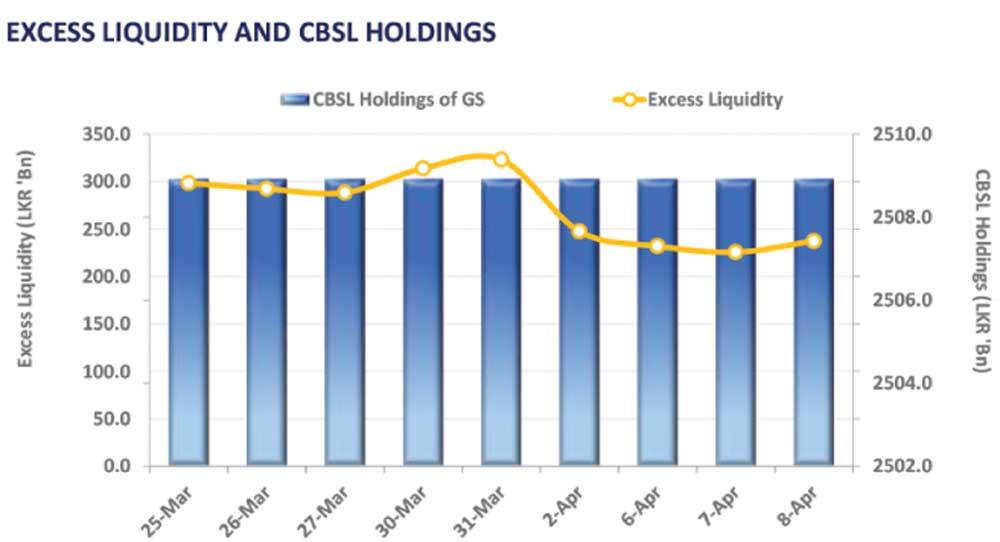

On the external front, the Sri Lankan rupee stayed steady at Rs.315.45/US dollar compared to the previous day. Liquidity in the banking system expanded to Rs.237.26 billion, from Rs.225.43 billion recorded previously.