Reply To:

Name - Reply Comment

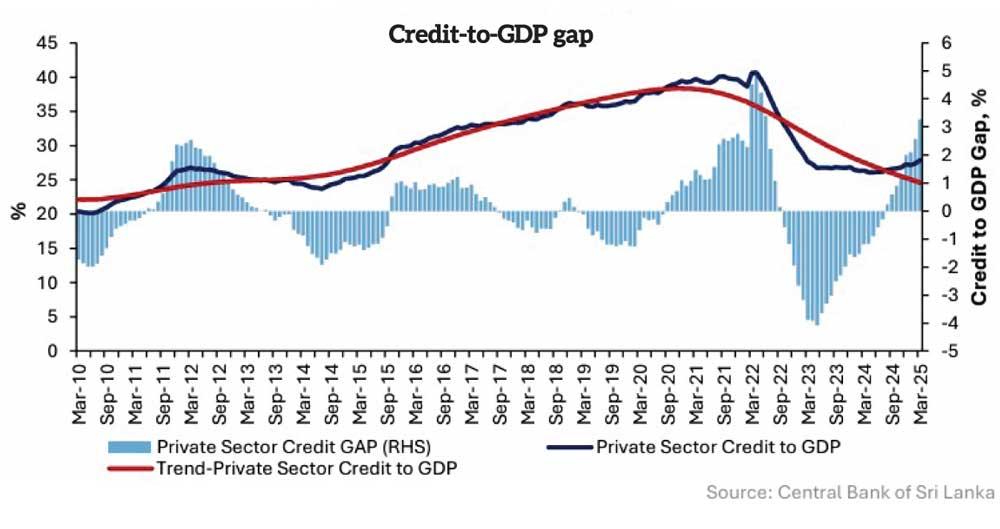

Sri Lanka’s private sector credit-to-GDP ratio has been rising from around the middle of 2024, with the credit-to-GDP gap or the credit gap widening, reflecting the expansionary credit cycle.

Credit-to-GDP or the gross domestic product is a measure of total outstanding credit to the private sector as a share of the size of the economy and is a key indicator of the overall economic health and a bellwether of risks building up in the banking sector through excessive lending.

Based on the latest data available through March 2025, Sri Lanka’s credit-to-GDP stands at slightly below 30 percent, with the credit gap standing at tad higher than 3.0 percent, after gradually rising from the middle of last year when a more meaningful growth in credit to the private sector began.

This gap was negative during the economic crisis between around the second half of 2022 through the first half of 2024, when Sri Lanka was slowly emerging out of the worst of the economic crisis. This was because the overall private sector credit growth was only nominal or negative during most of this period. The credit-to-GDP gap is measured as the difference between the credit-to-GDP and its long-running trend. This is also an indicator for assessing the banking sector risks and overall health of the financial system.

A negative credit-to-GDP gap suggests that the current credit-to-GDP ratio is lower than the long-term trend and thus, indicates a potential over-leveraging or credit stagnation. Meanwhile, a positive gap suggests a risk of financial instability.

Despite a positive gap at present, it remains modest and Sri Lanka is still in its early stage of its credit cycle and thus does not imply a risk.

“The resilience of the financial sector gradually improved during 1H-2025, amidst the improving macroeconomic conditions. The total assets of the banking sector expanded during the period under review, mainly due to the increased investments as well as loans and receivables,” the Central Bank stated. “Accordingly, total assets recorded a year-on-year (YoY) growth of 14.9 percent at end-June 2025 and stood at Rs.23.8 trillion. Furthermore, the growth of gross loans and receivables notably accelerated to 11.4 percent, YoY, at end-June 2025, amidst the eased monetary conditions,” it added.

However, this positive gap reached as high as 5.0 percent in 2022, signalling the financial crisis, which unravelled in March that year.

The private sector credit data available through the first six months showed that the banks have ramped up their lending drive as of late, as they expanded their total outstanding private sector credit by a mammoth Rs.221.6 billion, taking the first six months’ growth to a gargantuan Rs.716.1 billion, which translated to a faster 17.9 percent growth from a year ago.

The Central Bank in July brushed aside concerns of an overheating of the economy – higher credit-to-GDP with higher inflation – from the current spell of rapid growth in credit.

This is because the current spell of credit is taking place after a period of degrowth in credit and at present, the government and public sector institutions rely less on the banking sector borrowings, as their financials have improved after their prices were tied to the true costs.

Hence, the Central Bank said it currently witnesses what it calls a crowding-in effect of credit from a crowding out of credit, due to the government absorbing a large amount of debt in the run up to the economic crisis.