08 Aug 2025 - {{hitsCtrl.values.hits}}

Customer deposits in the licensed commercial banking sector continued to grow at a faster rate from 2024 through the second quarter of 2025 despite the interest rates on deposits slumping in line with the decline in market interest rates.

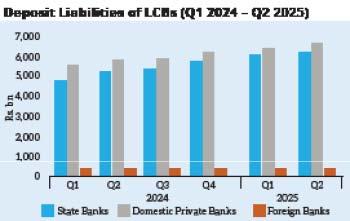

Customer deposits in the licensed commercial banking sector continued to grow at a faster rate from 2024 through the second quarter of 2025 despite the interest rates on deposits slumping in line with the decline in market interest rates.

According to the Central Bank, the growth was driven by State commercial banks followed by private sector commercial banks with foreign commercial banks failing to make much traction during the period.

“The rise in deposits was mainly driven by state banks as well as domestic private banks, aligned with increasing private sector credit flows, supported by a low interest rate environment,” the Central Bank said in their recently released Market Operations Report.

The data showed that the rupee deposit liabilities had risen by as much as Rs.559.2 billion in the three months through March 2025 to Rs.12,883.0 billion followed by another Rs.351.3 billion in the second quarter of 2025 to Rs.13,234.3 billion.

Though slowing somewhat in the second quarter from the growth in the first quarter, it was quite surprising the inclination for bank deposits as an investment or savings by the people even amidst declining deposit rates.

For instance the average weighted deposit rate fell by 411 basis points to 4.11 percent during 2024 to 7.53 percent to end the year while the average weighted fixed deposit rate slumped 561 basis points to settle at 9.27 percent at the end of the year.

Between December 2024 and March 2025, the average weighted deposit rate fell further by 38 basis points to 7.15 percent while the average weighted fixed deposit rate fell 48 basis points to 8.79 percent.

Based on the latest data available up to May, the two rates fell further to 6.98 percent and 8.56 percent following the 25 basis points cut in the Overnight Policy Rate (OPR) by the Central Bank.

At their third monetary policy meeting held in May, the Central Bank lowered the OPR to 7.75 percent to quicken the return of prices to positive territory from the months-long deflation and also to further push market interest rates down to support the economy’s recovery by way of channeling more funding into the real economy from the banks.

At the meeting however the Central Bank left the banks’ Statutory Reserve Ratio (SRR) at 2.0 percent – the proportion of rupee deposit liabilities the commercial banks are required to maintain as cash deposit in their settlement accounts with the Central Bank.

Due to the increase in the rupee deposit liability, the total required reserves went up to Rs.202.9 billion by the end of June 2025 from Rs.187.3 billion at the end of December 2024.

Given the pace and the quantum of growth in the bank deposits in the system shows that still bulk of the savings of the people are drawn into the banking sector considering its perceived safety compared to other alternative investment options such as stocks which have gone up in value a lot.

07 Jun 2026 37 minute ago

06 Jun 2026 06 Jun 2026

06 Jun 2026 06 Jun 2026

06 Jun 2026 06 Jun 2026

06 Jun 2026 06 Jun 2026