Reply To:

Name - Reply Comment

Governments use fiscal policy to promote strong and sustainable economy

Whilst tax avoidance is legal, tax evasion is not

Whilst tax avoidance is legal, tax evasion is not

Tax evaders have been developing increasingly sophisticated methods of concealing income

Tax evasion and Tax crime are major problems when generating revenue in the world

Any government in the world, whether developed or not needs sufficient Revenue for government activities. To achieve the people’s aspiration from bottom to top, government uses fiscal policy and other methods. Governments use fiscal policy to promote strong and sustainable economy. The basic tools used by government for fiscal policy are spending and taxation. A sound fiscal policy of any government helps to achieve macro-economic stability allocation of resources, increasing of production and distribution of income. The developing counties basically consider in reducing income inequality and poverty by providing social safety nets and ensure greater equity of opportunities (Eg. through public education, health) or outcome (Eg. through taxing the rich).

While governments are planning to collect maximum revenue through its agencies, some individuals, organizations, entities also struggle to evade Taxation and conceal their income and tax liabilities.

While governments are planning to collect maximum revenue through its agencies, some individuals, organizations, entities also struggle to evade Taxation and conceal their income and tax liabilities.

Tax evasion and Tax crime are major problems when generating revenue in the world. They are main barriers in Development in the world also.

Tax crime has caused not only loss of revenue to the country but also it cripples the function of some of government activities. The ultimate effect of this crime is destruction of the people’s right and Government achievements too. Therefore, many international organizations have identified the effect of Tax crime and evasion and made some possible solutions to minimize them.

Having identified and analysed this worldwide issue, many International organizations have taken several steps to have a dialog to combat this issue. The followings are extracted from the reports issued and the end of international conferences.

“Vast amount of money are kept offshore and go untaxed to the extent that taxpayers fail to comply with tax obligations in their home jurisdiction. Offshore tax evasion is a serious problem for jurisdictions all over the world, OECD and non-OECD, small and large, developing and developed. Cooperation between tax administration is critical in the fight against tax evasion and key aspect of that co-operation in exchange of information.” Angel Gurria, OECD Secretary-General, Report to the 2013 G20 Leaders’ Summit, Saint-Petersburg

“More than USD 1 in every USD 6 in the world does not subject to tax precisely because those earning it deliberately ensure that it would be hidden from the world’s tax authorities. Tax evasion is always a crime. Tax evasion on this scale is not just a personal crime though; it then become a crime against society and a crime against democracy.” Tax justice Network (2011), The Cost of Tax Abuse

Tax Avoidance – This includes activities which reduce taxpayer’s tax liabilities in ways that were not intended when law was enacted. Tax avoidance always see the loopholes in the tax law. In avoidance, taxpayer minimises his tax liability by taking such ways and means which do not violate the law.

Tax Evasion – This is an illegal practice committed by a person or entity by deliberately distorting of facts in relation to the true tax liability, with the intention of non – payment of tax even after liability has been incurred. In Tax evasion, taxpayer deliberately misrepresents of true position of his affairs with the view of the tax authorities to reduce the tax liability. Tax evasion includes not only an act of evasion itself, but also an attempt to evade with the intention of non-payment of tax.

Murphy (2011) calculated that the tax gap in 145 countries (covering 98 per cent of the global GDP) amounted to 18 per cent of global GDP (i.e. $ 1 in every $6 is not subject to taxation) and total amount of tax evaded was US$ 3.1 trillion

Murphy (2011) calculated that the tax gap in 145 countries (covering 98 per cent of the global GDP) amounted to 18 per cent of global GDP (i.e. $ 1 in every $6 is not subject to taxation) and total amount of tax evaded was US$ 3.1 trillion

The basic tools used by government for fiscal policy are spending and taxation. A sound fiscal policy of any government helps to achieve macro-economic stability allocation of resources, increasing of production and distribution of income

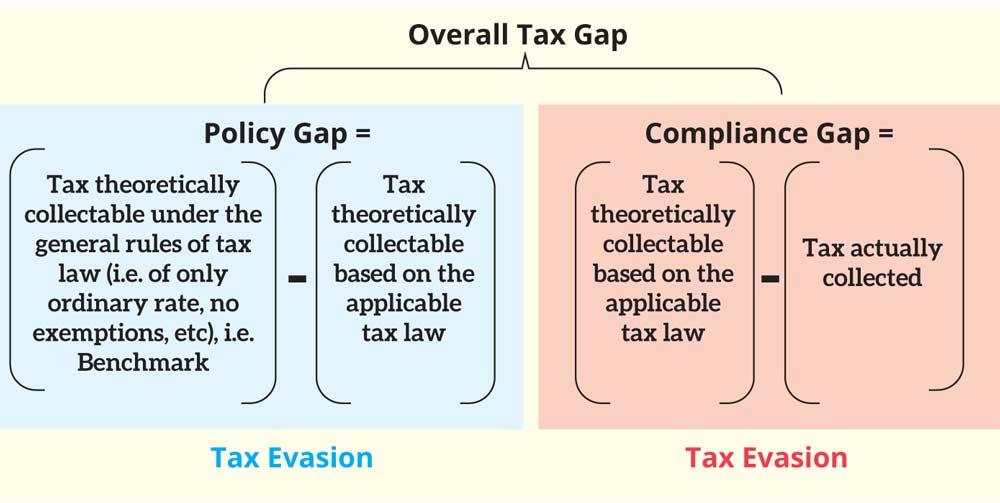

Tax gap

Broadly defined, the tax gap is the difference between the taxes that would be paid if all obligations were fully met in all instances, and taxes that are actually paid and collected.

Broadly defined, the tax gap is the difference between the taxes that would be paid if all obligations were fully met in all instances, and taxes that are actually paid and collected.

Although it is sometimes seen as a measure of tax evasion or fraud, the tax gap is the result of both intentional and unintentional actions. For instance, non-compliance can be due to:

Deliberate choices (such as hiding income or over-claiming deductions/credits)

Deliberate choices (such as hiding income or over-claiming deductions/credits)

Mistakes sometimes due to not knowing the Law.

Ignorance on Registration, filing, reporting, and payment obligations

Inability to comply (such as when a taxpayer declares bankruptcy and cannot pay their tax debt)

Changes to tax rules, procedure, interfusing system, and economic events continually

Understanding the elements of the tax gap enables policymakers and tax administrators to make better decisions regarding how to allocate resources.

Outcome of Tax Gap

It results in higher taxes. Honest taxpayers pay nearly 20 percent more in tax due to tax cheating. Collecting the underpaid taxes takes time and costs money. Tax rates must be set more higher initially in order to cover the shortfall that results from the tax gap.

It results in higher taxes. Honest taxpayers pay nearly 20 percent more in tax due to tax cheating. Collecting the underpaid taxes takes time and costs money. Tax rates must be set more higher initially in order to cover the shortfall that results from the tax gap.

It increases the national deficit, which further increase taxes;

It is undermining trust in society;

It reduces the level and quality of government service that can be offered

Tax Evasion – A world Problem

Whilst tax avoidance is legal, tax evasion is not. Like other frauds it is difficult to evaluate how much tax evasion takes place.

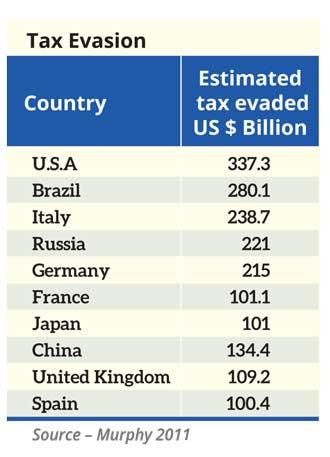

One measure is the ‘tax gap’ being the difference between the amount of income that should be reported to the tax authorities and the amount that actually is reported. Murphy (2011) calculated that the tax gap in 145 countries (covering 98 per cent of the global GDP) amounted to 18 per cent of global GDP (i.e. $ 1 in every $6 is not subject to taxation) and total amount of tax evaded was US$ 3.1 trillion. The top ten countries by value of tax evaded are shown in Table 3.5 and in each of those countries the value of tax evaded exceeded US$ 100 billion.

A well-functioning programme with specific features was outlined in the OECD in 2017. It also emphasized both legal mechanism and institutional frame work and consists of the following 10 principles/ good practices.

1. Ensuring tax offenses are criminalized

2. Devising an effective strategy for addressing tax crimes (and knowing the major threats and risks)

3. Having adequate investigative powers – within the tax agency directly or powers available indirectly (across other law enforcement organization)

4. Having effective powers to freeze, seize and confiscate assets (e.g. to collect tax)

5. Having a clear organizational structure with defined responsibilities

6. Having adequate resources for tax crime investigation

7. Making tax crimes a predicate offence for money laundering

8. Having an effective framework for domestic inter-agency co-operation

9. Ensuring international co-operation mechanisms are available

10. Protecting suspects right (ensure procedural fairness and rights are observed e.g. presumption of innocence).

Source: OCED (2017), Fighting Tax Crime: The Ten Global Principles, OECD Publishing, Paris

Tax criminal proceeding in Sri Lanka

Section from 186 to 193 in chapter xviii of the Inland Revenue Act No. 24 of 2017, clearly mention the criminal proceeding for Tax crime. Act No. 10 of 2006 also stated some part of criminal Investigation on Tax crime. The Tax evasion and other proceedings are specifically stated in it. But in 2017 Act clearly identify major issues of Tax evasion and interpret it and some activities against criminal charges also.

The following sections denote the fines on conviction on guilty of an offence.

On Tax Evasion

Tax evasion – Sec. 189

A person who willfully evades or attempts to evade the assessment, payment or collection of tax or who willfully and fraudulently claims a refund of tax to which the person is not entitled, shall be guilty of an offence and shall be liable on conviction to a fine not exceeding ten million rupees or to imprisonment for a term not exceeding two years or to both such fine and imprisonment.

Impeding Tax Administration - Sec. 190

(1) A person who willfully impedes or attempts to impede the Department in the administration of this Act shall be guilty of an offence and shall be liable on conviction to a fine not exceeding one million rupees or to imprisonment for a term not exceeding one year or to both such fine and imprisonment.

(2) For the purposes of this section, a person impedes the administration of this Act if the person;

(a) fails to comply with lawful request by the official to examine documents, records, or data within the control of the person.

(b) fails to comply with a lawful request by a tax official to have the person appear before officials of the Department.

(c) interferes with the lawful right of a tax officials to enter into premises;

(d) fails to file a return.

(e) uses a false taxpayer identification member or a taxpayer identification number that does not apply to the person.

(f) refuses to allow the Commissioner General or authorized officer to inspect or measure land or refuses to deliver for inspection any map, plan, title deed, instrument of title or other document.

(g) makes a statement to a tax official that is false or misleading in a material particular.

(h) fails to comply with a notice issued under section 170.

(i) fails to maintain required records or

(j) otherwise impedes the determination, assessment or collection of tax.

Failure to preserve secrecy- Sec.191

A person who contravenes subsection (2) or (3) of section 100 shall be guilty of an offence and shall be liable on conviction to a fine not exceeding one million rupees or imprisonment for a term not exceeding one year or to both such fine and imprisonment.

Amendment Act No. 10 of 2021 introduced the following new section as Sec. 190A

Any person who fraudulently;

(a) prepares, any document or information,

or

(b) certifies a document to be furnished to the commissioner- General, commits an offence under this Act, and on conviction after summary trial before a Magistrate, be liable to a fine not exceeding one million rupees or imprisonment of either description for a term not exceeding six months.

Conclusion

Tax evaders have been developing increasingly sophisticated methods of concealing income. Tax crime is a violation of tax law and in order to combat these issues, every government must take action to investigations, proceeds and implement legal proceeding under criminal procedures.

In the modern world with techniques used for crimes and much legal activities occurred, it will be a severe problem in combatting tax evasion also but the following recommendations made to tackle those issues.

1. Establish as effective legal mechanism with institutional framework for domestic inter agency cooperation. For this purpose, financial intelligent unit, criminal Investigation high legal entities can function together.

2. Exchange of information for tax purpose. This should be included setting standards for sending and receiving information and revealing the names and value of Bank Accounts, property and other assets or owners of anonymous legal stretches.

3. Introducing and implementing new framework for this purpose we will have to seek help from international organization also.

In the past, some instrumental frame work designed by OECD also inspected. Such as base erosion and profit shifting BEPS, Financial Action Task Force (FATF), and OECD Academy for tax and financial criminal investigation are some of them.

4. Making Strong tax trailing among the countries. International Agreements are useful to make a forum of good legal mechanism and close the loopholes. The agreements are also useful to enable tax Authorities and relevant parties to obtain information and some impotent data in tax evasion.

Sources –

Effective Inter-Agency Co-Operation in Fighting Tax Crimes and Other Financial Crimes - OECD

Fighting Tax Crime: THE TEN GLOBAL PRINCIPLES - OECD

Inland Revenue Act No. 24 of 2017