Reply To:

Name - Reply Comment

Sri Lanka is approaching a notable shift in its fiscal landscape, with an Ernst & Young Tax Alert highlights that the amendments aim to broaden the tax base by lowering registration thresholds and bringing a wider range of participants—including foreign digital service providers—into the VAT system. As the Bill moves through Parliament, professional circles have also noted areas that may benefit from further clarification, including the treatment of digital services and the valuation of non-cash employee benefits. For many businesses, the transition toward more structured electronic compliance systems signals an important operational shift, bringing both opportunities and added compliance responsibilities.

Sri Lanka is preparing for one of its more extensive tax reforms in recent years as the proposed amendments to the Value Added Tax Act advance toward a possible July 1, 2026 implementation. The changes, outlined in a detailed update by Ernst & Young, are expected to affect a broad cross-section of the economy, including banks, retailers, investors, digital service providers, and consumers.

The amendments remain at the Bill stage and are not yet law. Published in a government gazette on April 24, 2026, they must undergo the full parliamentary process—including three readings and the Speaker’s endorsement—before taking effect. A 14-day window for constitutional challenges will also apply once the Bill is placed in Parliament’s Order Paper.

Even so, many businesses have already begun preparing in anticipation.

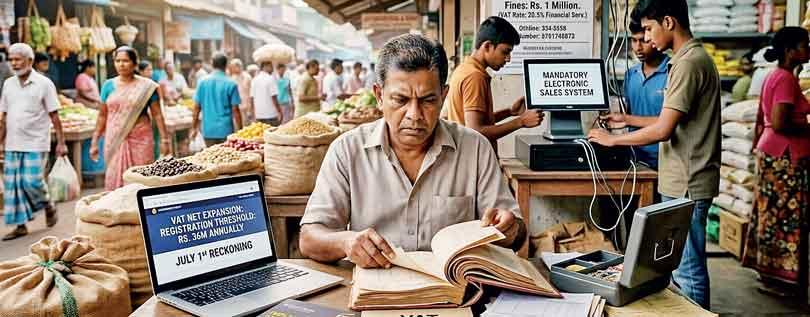

One of the largest changes is the reduction of the mandatory VAT registration threshold.

As per the Bill, businesses with turnover exceeding Rs. 9 million per quarter or Rs. 36 million annually would need to register for VAT.

That move is expected to bring a much larger group of small and medium sized businesses into the tax system. However, newly registered businesses would gain the ability to claim input VAT credits on purchases, which may partly offset the impact.

The proposed threshold also aligns with the registration limit already used under the Social Security Contribution Levy framework, a step authorities believe will simplify monitoring and administration.

The Bill also introduces a special deemed input tax credit for businesses in wholesale and retail trade that register for VAT on or after April 1, 2026.

Under that provision, businesses can claim credits for VAT paid on unsold stock held at the time of registration, provided proper records are maintained and submitted with VAT returns.

The credit would apply only to goods that are not specifically exempt under the VAT Act.

Another major proposal requires VAT registered businesses to use government approved electronic point of sale systems.

These systems must be capable of recording transactions, issuing invoices and transmitting transaction data electronically.

Authorities say the goal is to improve tax compliance and reduce the underreporting of sales.

The Commissioner General of Inland Revenue would approve the systems used by businesses.

Companies would be required to adopt the approved systems within three months from the date specified by authorities.

This requirement may create additional compliance costs for smaller businesses that still rely on manual bookkeeping systems.

However, authorities believe real-time electronic reporting will strengthen tax collection and reduce leakages.

The proposed Bill also introduces an entirely new section targeting foreign digital service providers.

The rules would apply to nonresident companies offering digital services to Sri Lankan users through websites, applications and online platforms.

Foreign companies would need to register for VAT if annual sales to Sri Lankan customers exceed Rs 36 million or quarterly sales exceed Rs 9 million.

The proposal defines an electronic platform broadly as any internet-based system enabling the supply of services.

This could potentially affect streaming services, cloud computing providers, software firms, online marketplaces, subscription platforms and application stores.

The Bill says a digital service would be considered supplied to a person in Sri Lanka if at least two indicators are met.

Those indicators include a Sri Lankan billing address, business address or residential address, payment through a Sri Lankan bank, use of a Sri Lankan issued payment card or a Sri Lankan IP address.

The proposal also requires foreign providers to apply electronically for VAT registration within three months of becoming liable.

VAT returns and communications would be handled electronically through the Inland Revenue Department’s systems.

Payments could be made either in Sri Lankan rupees or approved foreign currencies.

Despite the broad framework, tax specialists say several parts of the digital services proposal remain unclear.

Ernst & Young noted that the Bill does not contain a highly detailed definition of “digital services,” unlike laws used in some other countries.

Ernst and Young further highlighted that there are at two possible interpretations on the application of VAT on Digital Services under the Bill

Under one interpretation, VAT would apply only when three separate parties are involved: a foreign digital platform, a service provider and a Sri Lankan recipient.

Under a broader interpretation, the foreign company itself could be treated as the service provider, expanding the tax reach substantially.

Tax specialists say the second interpretation could increase costs for Sri Lankan businesses because foreign companies are likely to pass VAT charges directly to customers.

Businesses may also face additional withholding tax obligations on top of VAT payments.

The report added that software providers and technology firms could face a major administrative burden under the proposed framework.

The bill also contains exemptions for selected digital services.

Educational services, including online courses, training platforms, and webinars, would be exempt from VAT under the proposal.

Healthcare related services such as telemedicine and AI assisted diagnostics would also remain exempt.

Services supplied to diplomatic missions and certain government organisations would also qualify for exemptions.

Still, Ernst and Young say there remains uncertainty regarding how the value of digital services should be calculated for VAT purposes because earlier gazette notifications and the new Bill use different legal sections.

Banks and financial institutions are among the sectors expected to experience some of the largest financial impacts under the proposed amendments.

The VAT rate on financial services is expected to increase from 18% to 20.5% beginning July 1, 2026. At the same time, the Social Security Contribution Levy on financial services would be removed.

While authorities describe the move as a simplification measure, tax specialists say banks may still face higher effective tax costs.

Previously, the Social Security Contribution Levy was deductible when calculating income tax liabilities.

The revised VAT structure may therefore increase the final tax burden unless additional adjustments are introduced.

The Bill also changes how “emoluments payable” are calculated for VAT on financial services.

That term refers to employee-related compensation and benefits used in calculating VAT liabilities for banks and financial institutions.

For periods after April 1, 2018, the proposal links the definition to employment income provisions under the Inland Revenue Act of 2017.

Importantly, the amendments introduce a “fair market value” basis for valuing noncash employee benefits.

Ernst & Young is of the view that the fair market value should be defined to bring in more to preempt disputes with the Inland Revenue Department.

Items such as transport facilities, refreshments, uniforms and vehicle benefits could potentially be treated as taxable employee benefits.

Businesses and tax authorities may disagree on the correct market value of those benefits.

Ernst & Young warned that the broader definition could expand the range of items included in VAT calculations, increasing tax liabilities for financial institutions.

The Ernst & Young tax alert suggested that Sri Lanka may eventually need official valuation guidelines similar to those already issued for income tax purposes under the Inland Revenue Act.

The amendments also specify that VAT returns filed before January 1, 2026, using the earlier gross remuneration method would still be treated as valid.

The Bill also attempts to clarify how dividend income should be treated for VAT on financial services for non-banking and non-financial institutions.

Under the current practice, companies that are not banks or financial institutions may exclude dividend income from VAT calculations if the income is not treated as business profits.

The proposal attempts to reinforce that exclusion by stating that dividend income received by nonfinancial businesses should not automatically be treated as business profits for VAT purposes.

However, Ernst & Young said the wording may still create confusion in some situations.

For example, a holding company that occasionally provides financing to related parties may face uncertainty over whether its dividend income still qualifies for exclusion.

The Ernst & Young Tax Alert highlighted that some holding companies and investors could continue facing VAT exposure on realised and unrealised investment gains. It is also said that VAT traditionally applies to goods and services rather than passive investment income.

They say additional clarification would help create a more stable environment for capital investment and corporate structuring.

The Bill also affects Sri Lankan companies purchasing services from overseas providers.

Businesses that are VAT exempt may still become exposed to VAT on imported digital services.

There is also uncertainty regarding companies registered only for VAT on financial services.

The proposal refers broadly to “registered persons” under the VAT Act without clearly stating whether VAT on financial services registrations qualify for exemption from digital services VAT.

Tax advisers say this ambiguity could create disputes once implementation begins.

The proposed amendments significantly strengthen compliance provisions and penalties.

Fraudulently attempting to obtain VAT refunds through false information, forged documents or concealment of material facts would become a criminal offence.

Businesses failing to maintain valid tax invoices or customs declarations at the time of filing VAT returns could also face penalties.

For offences linked to tax periods beginning after October 1, 2025, penalties could increase sharply.

The proposed maximum fine rises from Rs. 25,000 Rs. 1 million, alongside possible prison sentences of up to six months.

Tax specialists say the changes signal a tougher enforcement approach by the authorities as Sri Lanka attempts to improve tax collection.

Despite the extensive proposals, businesses and tax professionals continue raising concerns about implementation and enforcement capacity.

The digital services framework may require substantial coordination between tax authorities, banks and international technology firms.

Questions also remain over whether Sri Lanka has sufficient technical systems and staffing to monitor electronic transactions in real time.

Businesses are also watching closely for additional regulations, gazette notifications and implementation guidelines expected before July 2026.

Tax professionals say further clarification is especially needed on digital service definitions, treatment of passive investment income, valuation of employee benefits and exemptions for business-to-business transactions.

Although the Bill is not yet law, businesses are already reviewing contracts, accounting systems and compliance procedures in anticipation of implementation.

Technology firms and multinational digital service providers are also evaluating whether they may fall within the proposed registration thresholds.

The reforms represent one of Sri Lanka’s broadest efforts in recent years to modernize tax administration and expand revenue collection as the country continues rebuilding public finances.

Supporters say the changes could improve transparency, strengthen compliance and align Sri Lanka more closely with global tax trends.

Critics argue that unclear wording and aggressive compliance burdens may create confusion, higher operating costs and legal disputes unless additional guidance is issued before implementation begins.