Reply To:

Name - Reply Comment

Financial frauds and scams are no longer isolated challenges; they are a systemic threat to public trust on financial system, economic resilience and national development.

Financial frauds and scams are no longer isolated challenges; they are a systemic threat to public trust on financial system, economic resilience and national development.

Financial frauds and scams have intensified sharply in recent years, exacerbated by the rapid expansion of digital banking and the increasing reliance of financial consumers on online financial services. While technological innovation has made transactions faster, cheaper and more accessible, it has simultaneously created new avenues of exploitation for sophisticated fraudsters.

Today, financial consumers are exposed to a growing array of threats: phishing attacks, fraudulent investment schemes, identity theft involving the misuse of stolen personal or financial information, unauthorised transactions and unlicensed financial operators. These are not isolated incidents.

They form a part of a deliberate and evolving criminal landscape that preys on trust, exploits the gap in digital literacy and operates with increasing speed and scale.

Many consumers fall victim to financial fraud through a combination of limited awareness, misplaced trust and the allure of quick financial gains. Fraudsters exploit these vulnerabilities with calculated precision, deploying fear, urgency and attractive promises to manipulate their targets.

A failure to observe safe banking practices, verify information or guard confidential details only deepens this exposure, making informed and vigilant behaviour the most effective defence a consumer can hold.

In today’s interconnected financial ecosystem, the effects of financial frauds and scams extend far beyond the individual victim. They have emerged as a widespread threat capable of undermining public confidence, weakening financial stability and hindering national development. This is why protecting financial consumers from financial frauds and scams must be elevated from a consumer protection issue to a matter of strategic national importance.

Financial frauds and scams, at their core, are unlawful and deceptive acts carried out by individuals or organised groups with the intent of causing financial harm.

Through manipulation and misinformation, consumers are misled or pressured into authorizing transactions, disclosing confidential information or transferring funds from their own accounts.

The methods employed, such as impersonation, fabricated promises, misuse of digital platforms and exploitation of trust, typically bypass the formal controls of banking systems by manipulating the consumer directly.

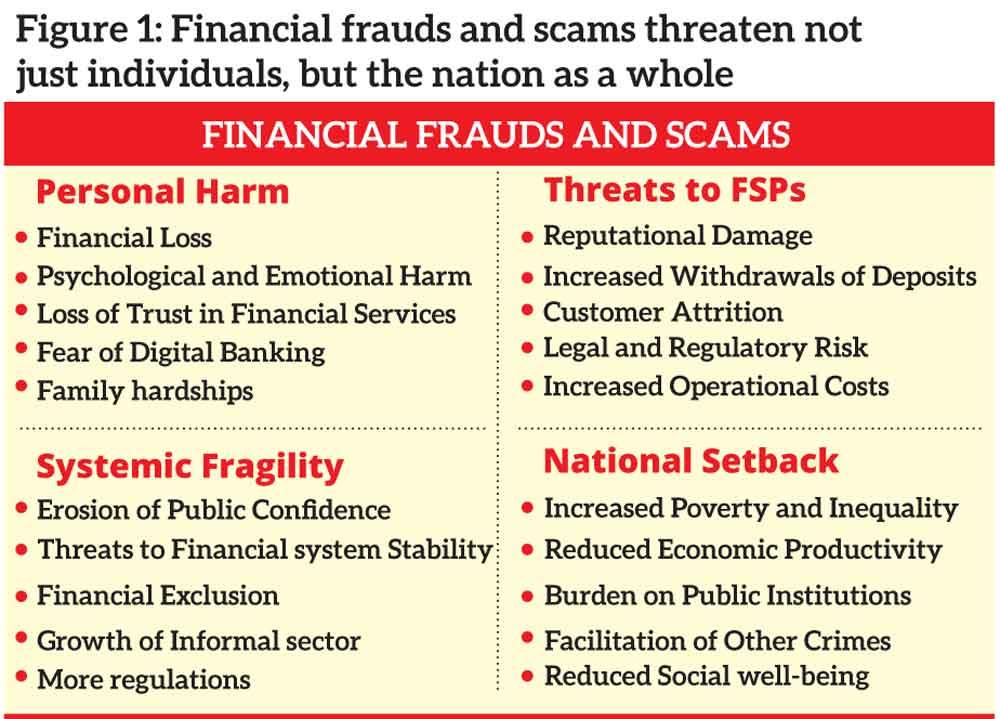

The consequences of financial frauds and scams extend far beyond the theft of money or data, causing serious and wide-ranging harm to individual consumers, financial service providers (FSPs), the financial system and society at large. The true cost of financial fraud is measured across four dimensions.

Financial frauds and scams inflict harm far greater than monetary loss alone. When consumers fall victim to financial frauds and scams, confidence in formal financial institutions diminishes and participation in the broader financial system weakens alongside it. The consequences reach well beyond the individual, weakening institutional credibility, threatening systemic stability and quietly undermining the social trust upon which a healthy economy depends. Preventing financial frauds and scams is, therefore, not simply an act of financial protection. It is an act of national preservation, one that safeguards public confidence over the financial system, sustains economic stability and secures the foundations of long-term social well-being.

When a nation chooses to treat fraud prevention as a strategic priority rather than a reactive obligation, it reaps dividends that extend well beyond the containment of financial losses.

Strategic prevention builds public confidence, protects household savings and reinforces the credibility of FSPs. More significantly, it transforms the national response to fraud from a purely defensive response into a forward-looking investment in stability, inclusion and sustainable growth.

By anticipating risks, enhancing safeguards and coordinating national efforts, a country both protects its citizens and fosters a secure financial environment where trust is preserved and economic resilience is sustained. The national gains of such an approach are both tangible and far-reaching.

Strengthening Public Trust in the Financial System: Trust is the invisible foundation of any financial system.

People deposit their savings, transact digitally and participate in the formal economy based on one fundamental belief, that their money is safe and that FSPs will protect them.

Every successful fraud and scam quietly erodes that belief and it is strategic prevention that preserves it, reinforcing the credibility of financial institutions and sustaining the willingness of the public to engage with the formal financial system.

Promoting Financial Inclusion and Digital Transformation: Sri Lanka, like many nations, is striving to build a digital economy where electronic payments, mobile banking and cashless transactions are the norm. Yet, digital transformation can only succeed if consumers feel secure. Unmitigated fraud risk may discourage vulnerable groups, such as the elderly, those with low financial literacy and first-time digital users, from engaging with formal financial services. Effective fraud prevention, therefore, does more than protect individuals. It sustains the momentum of financial inclusion and ensures that the benefits of technological progress are shared by all.

Reducing Poverty and Social Vulnerability: Financial frauds and scams often disproportionately affect those with limited financial literacy. When low-income households lose their savings, the consequences extend well beyond financial hardship, pushing families towards debt, diminishing their access to food, education and healthcare and deepening existing social inequalities. Protecting financial consumers is ultimately not solely a regulatory obligation. It is a matter of social justice, one that reflects a national commitment to shielding the most vulnerable from exploitation and upholding the principles of equality and shared social welfare.

Disrupting Organised Crime and Reinforcing National Security: Many large-scale financial fraud schemes are not the work of lone criminals. These are operations embedded within broader networks of money laundering, cybercrime and transnational organised crime.

Effective fraud prevention contributes directly to dismantling these networks and strengthening the overall architecture of national security.

Safeguarding Financial System Stability: Financial security drives active participation in the economy. Households that trust the financial system are more likely to save, invest and consume, which are critical drivers of growth.

Conversely, large-scale fraud incidents can trigger withdrawal from formal financial channels, reduce economic activity and in severe cases, destabilise financial markets.

Such disruptions highlight how financial fraud and scams can extend beyond individual losses to pose broader risks to the stability of the financial system.

Addressing these threats by strengthening fraud prevention and consumer protection measures is therefore essential to safeguarding financial system stability.

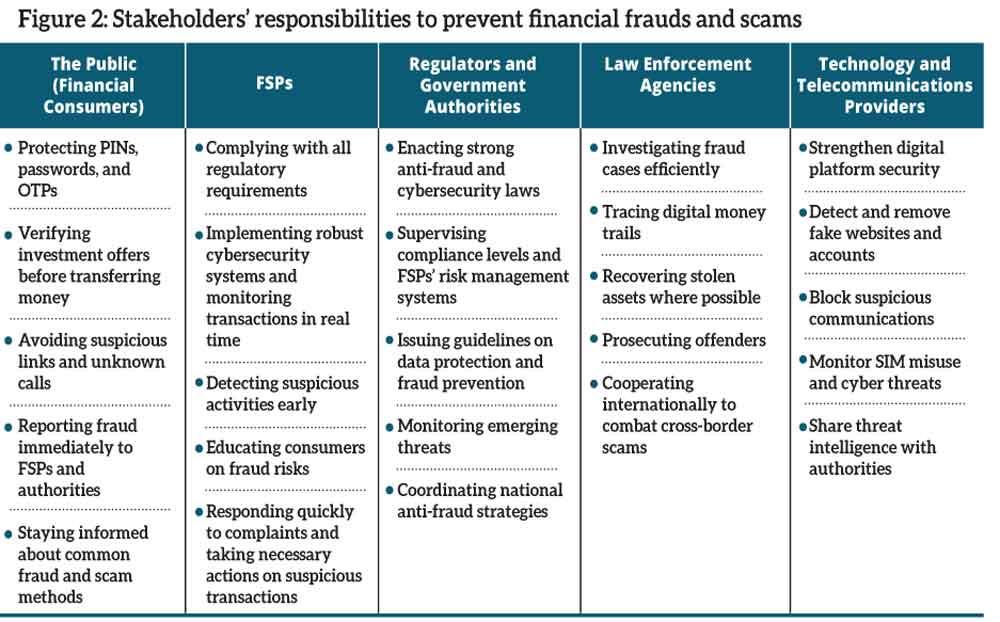

Preventing financial fraud is a shared national responsibility, one that demands coordinated action across regulators, FSPs, law enforcement agencies, technology providers and the public. Each stakeholder plays a distinct yet interconnected role and it is only through the deliberate alignment of these efforts that a truly resilient financial ecosystem can be built. A coordinated national response does not merely react to fraud; it anticipates, prevents and systematically minimizes harm, protecting not only individual savings but also public trust, economic stability and the broader foundations of national development.

Financial frauds and scams have emerged as one of the defining threats to Sri Lanka’s financial sector and to the well-being of its citizens. As demonstrated in this article, the evidence is unambiguous: the harms caused by financial frauds and scams are not confined to individual losses. They cascade across institutions, undermine systemic confidence and impede the nation’s economic well-being. Rising digitalization and interconnectedness make consumer protection against sophisticated financial frauds and scams more urgent than ever.

Combating this threat requires more than reactive enforcement. It requires the recognition, at the highest levels of policy, that protecting financial consumers is a strategic national priority. This means strengthening legal frameworks and supervisory capacity, enhancing institutional safeguards, deepening public financial literacy and fostering genuine collaboration among all relevant stakeholders. It is also essential to understand that fraud prevention is not a static exercise. Criminal actors are adaptive. They evolve with technology, exploit new social trends and continuously refine their methods. The national response must therefore be equally dynamic, characterised by continuous investment, regulatory agility and sustained public engagement.

Most importantly, fraud prevention should be understood as an investment, not a cost. The resources committed to protecting financial consumers are a fraction of the economic and social losses that widespread financial frauds and scams inflict.

A secure financial environment enables citizens to save with confidence, invest with purpose and engage with the formal economy without fear. It is precisely this connection between fraud prevention, economic resilience and financial system stability that elevates financial consumer protection beyond regulatory routine and establishes it, unequivocally, as a strategic national priority.

The writers: Yanaka Yamithra Ranaweera is a Deputy Director of Financial Consumer Relations Department, CBSL. Steffi Fernando is a Senior Assistant Director, Communications Department