Reply To:

Name - Reply Comment

The short answer is that the withdrawal was not a well-considered, revenue-driven -policy decision.

This decision, widely perceived as motivated by narrow interests rather than sound economic principles, appeared designed to target a specific major trading chain under the guise of expanding the

This move represents a bureaucratic and fiscal error that contradicts sound tax principles and imposes an undue burden on the economy.

A point of rare consensus among fiscal policymakers and legislators across the political spectrum was the deliberate exclusion of trading activities from both the GST and VAT frameworks.

Retired Deputy Commissioner General of IRD. Can be reached at [email protected]

This article examines the original legislative intent to exclude trading activity from the scope of Value Added Tax (VAT) and its predecessor, the Goods and Services Tax (GST). It critiques the subsequent policy shift that brought trading into the VAT net, arguing that this move represents a bureaucratic and fiscal error that contradicts sound tax principles and imposes an undue burden on the economy.

Value Added Tax (VAT) is presently charged on imports and on the following activities done as a business with some stipulations:

Value Added Tax (VAT) is presently charged on imports and on the following activities done as a business with some stipulations:

Manufacturing and production,

Provision of service, and

Trading. (Defined as the local buying and selling of goods in the wholesale or retail market).

Even though VAT was nominally introduced effective from 01st August 2002, it was virtually effective from 1998 in the name of GST which was introduced by then People’s Alliance (PA) government abolishing the Turnover Tax (TT). The name change from GST to VAT in 2002 was largely political, following an election promise by the incoming UNP government to abolish the GST.

A comparative analysis of the two Acts reveals near-identical structures and mechanisms, making the change one of branding rather than substantive fiscal reform.

Prudent Fiscal Policy Decision: Exclusion of Trading Activity from the Scopes of both GST and VAT

A point of rare consensus among fiscal policymakers and legislators across the political spectrum was the deliberate exclusion of trading activities from both the GST and VAT frameworks. This was a considered decision rooted in the anticipation of serious practical complications and economic distortions should such a tax be applied on the trading.

The wordings and Section 3 of both acts that excluded the trading activity from the scope of GST and VAT were identical and verbatim.

Section 3 of the respective GST Act, No. 34 of 1996 and VAT Act, No. 14 of 2002:

“Notwithstanding the provisions of section 2, the tax shall not be charged on the wholesale or retail supply of goods, other than on the wholesale or retail supply of goods, by-

(a) manufacturer of such goods; or

(b) an importer of such goods; or

(c) a supplier who is unable to satisfy the Commissioner-General, as to the source from which the goods supplied by him, were acquired : or”

This clear statutory language ensured that VAT liability on the sale of goods rested solely with the manufacturer or the importer—the points of origin in the supply chain. A trader purchasing from these sources was explicitly excluded, protecting a vast segment of the distribution network from direct VAT liability.

Rationality of Exemption of Trading Activity from VAT Liability.

Prior to introduction of GST in 1998, Turnover Tax (TT) was in place at relatively lower rates and it was charged on all four main branches of a business, namely manufacturing, importing, provision of services, and trading. The TT mechanism had two primary defects in its self.

Cascading (tax on tax) effect: It occurs when a sales tax is applied at every stage of the production and distribution chain, without any mechanism to credit the tax paid on previous purchases, and

Administrative Inefficiency: Applying the tax to the entire trading sector, often involving numerous small-scale transactions, wasted the tax administration’s limited resources. The cost of compliance and enforcement was disproportionately high compared to the revenue yielded, violating the acknowledged principles of taxation—namely fairness, convenience, and economic efficiency.

The introduction of GST/VAT solved the first problem by implementing a credit-invoice system that eliminated cascading. It solved the second by strategically limiting the VAT liability to manufacturers, importers, and service providers thereby focusing administrative efforts on fewer, larger taxpayers.

Resultant Revenue Shortfall and the Way Out.

Once the cascading (tax on tax) effect and the trading activity were removed from the TT, it would definitely create negative impact on the state coffer, of which the political and economic aftershocks were obvious.

GST/VAT effectively and efficiently addressed these two main concerns as follow:

I. Taxation at the Source: By concentrating the tax point at the source of the supply chain (manufacture or import), the tax is embedded in the cost of the goods. It is then passed down through the distribution chain to the final consumer. The trader acts as a passive collector rather than a primary taxpayer, ensuring revenue is captured without the administrative cost of taxing every transaction.

II. Enhanced Tax Rates: Turnover Tax rates were relatively low (ranging from 1% to 10%, with trading often at 1%). The introduction of GST/VAT came with proportionately higher standard rates (initially 10%-20%), designed to compensate for the revenue foregone by exempting trading, while simultaneously benefiting from a more efficient and broader base at the point of origin.

Thus, the introduction of GST/VAT not only mitigated the negative effects of excluding trading activity but also strengthened tax revenue in subsequent years by enhancing the efficiency of tax administration.

If excluding trading activity had indeed been a prudent and timely decision, it is reasonable to ask why that exclusion was later withdrawn and trading brought within the scope of VAT.

The short answer is that the withdrawal was not a well-considered, revenue-driven policy decision. This decision, widely perceived as motivated by narrow interests rather than sound economic principles, appeared designed to target a specific major trading chain under the guise of expanding the tax base.

In pursuit of this agenda, an amendment was introduced to Section 3 of the VAT Act, making enterprises engaged in trading liable to VAT if their quarterly trading turnover exceeded Rs. 500 million. This amendment took effect from 01.01.2013.

The targeted trading giant, however, effectively sidestepped the impact by restructuring its operations—splitting its entity into two. This maneuver ensured that each entity’s turnover remained below the Rs. 500 million threshold, thereby avoiding liability for VAT on trading turnover.

The bureaucrat did not relent. A subsequent amendment, effective from 01.01.2014, reduced the threshold to Rs. 250 million and introduced aggregation rules.

Under this revision, the sales of all associated or subsidiary companies within a group were combined to determine VAT liability. This amendment was specifically aimed at neutralizing the trading group’s previous restructuring strategy.

Despite the might of bureaucracy—fortified by legislative backing—the trading giant, supported by skilled tax consultants, managed to resist the challenge. Even after becoming liable to pay VAT at 12% on its trading turnover, the enterprise did not collapse as anticipated.

One reason for its resilience was that the additional VAT burden did not significantly erode its competitiveness. Prices remained on par with those of other traders who were not VAT-registered. The real secret, however, lay in the company’s considerable bargaining power, which enabled it to shift or share the VAT burden with its suppliers.

Reconsidering the VAT Exclusion

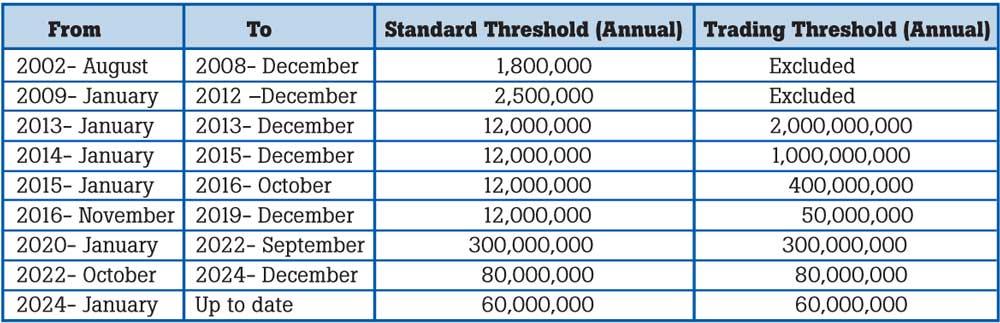

The initial decision to exclude trading activities from the Value-Added Tax (VAT) framework was a prudent and well-considered policy. After the withdrawal of exclusion and bringing large –scale traders into the VAT net, a semblance of prudence was temporarily (from 2013 to 2019) maintained through a significant gap in the registration thresholds for standard businesses as opposed to traders, acknowledging the unique nature of high-volume, low-margin trading activities.

This residual prudence as well eroded significantly following the political anarchy and instability of 2019. Post-chaos, policy-making abandoned its earlier cautious approach, leading to a haphazard alignment of thresholds that ignores the fundamental differences between trading and other sectors. The current policy no longer reflects the original principles of fairness and efficiency that supported the VAT system.

The following chronology of VAT registration thresholds illustrates this policy inconsistency and its increasing lack of discernment: (Table)

Charging VAT on Trading Vs. MRP and Lower Margin

Subjecting traders to the same VAT burden as manufacturers and importers is inequitable and unjustified. Unlike these primary suppliers, traders operate at the end of the distribution chain with significantly lower margins. Furthermore, they are legally bound to sell goods at the mandated Maximum Retail Price (MRP), non-compliance with which is a punishable offence.

In most cases, traders purchase their merchandise from suppliers who are not VAT-registered, which prevents them from claiming input tax credits. Even in situations where input credits are available, the payment of output VAT on trading activity becomes impractical when considered against the narrow trading margin and the statutory restriction imposed by the MRP.

Recommendations.

1. Restoration of status quo of trading activity in VAT: A return to the original GST/VAT structure – excluding trading activity from VAT net while maintaining robust and efficient taxation at these primary suppliers of manufacturer and importer level- is not a radical recommendation.

The original decision to exclude trading activity from GST and VAT was not accidental—it was a deliberate and prudent policy decision, aimed at avoiding inefficiencies and protecting both traders and consumers from undue hardship. The later inclusion of trading into the VAT net was a fundamental misstep, ignoring the original intent of lawmakers and undermining the very logic of VAT. Rectifying this error is essential, not only to restore fairness and efficiency in taxation but also to recognize the sound fiscal principles on which VAT was first built.

2. Compensatory VAT Rate Increase: The potential VAT revenue loss resulting from the exclusion of traders would be nominal, as traders occupy the final stage of the distribution chain due to lower markup and to credits claimed on earlier purchases. Consequently, their net VAT contribution is not a significant component of overall revenue.

To offset this marginal loss, it is recommended that the VAT rate be increased by four percentage points (from 18% to 22%), applicable only to primary suppliers—manufacturers, importers, and service providers. Any revenue foregone by excluding traders could thus be effectively recovered from this adjustment.

A scientific data-driven analysis of the VAT actually contributed by trading sectors in recent years, compared with the additional revenue anticipated from the proposed rate increase, would further substantiate the viability of this recommendation.

This two-pronged strategy offers a sophisticated and fiscally responsible path forward. By restoring the VAT system to its logical design—exempting the trading sector—the policy would eliminate significant administrative burdens and boost economic activity at the retail level. Concurrently, a modest, targeted increase in the VAT rate at the primary supplier level would safeguard government revenues, ensuring the change is budget-neutral. Even if the VAT rate were not increased, the revenue loss – if any – could be recovered through the enhanced efficiency of the tax administration.

Beyond the direct fiscal and economic advantages, this approach offers considerable political and social dividends.

For a government elected on a platform of eradicating corruption and restoring fairness, this policy delivers a clear victory: it reduces opportunities for bureaucratic harassment while providing tangible relief to the trading community.

The resulting goodwill, extending to thousands if not millions of individuals, would significantly strengthen the credibility of governance, build trust in public institutions, and reinforce the overall legitimacy of the tax system itself.

The writer is a retired Deputy Commissioner General of IRD. The writer can be reached at [email protected]