Reply To:

Name - Reply Comment

Authorities uncovered 60 alleged Ponzi schemes last year with a total US $ 3.25 billion in investor funds — the highest amount since around the time of the Great Recession, according to new data (CNBC, 2020)

Sahara Group Chairman Subrata Roy was arrested in 2014 on allegations of financial fraud for operating a business model, which closely reflects the features of a Ponzi scheme

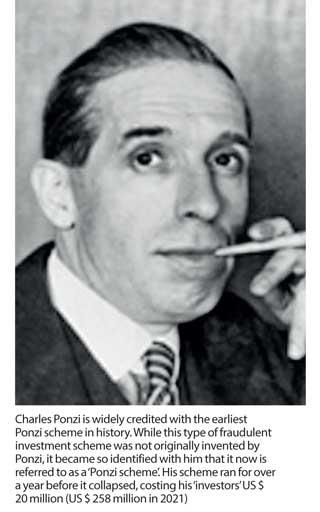

Carlo Charles Ponzi was an Italian immigrant whose stay in the United States is memorialised in relation to his swindling of US $ 20 million from investors in the 1920s. The amount would be equivalent to cool US $ 258 million in today’s terms and stands to reason why a specific type of financial fraud is now known as ‘Ponzi schemes’, with reference to Charles.

Carlo Charles Ponzi was an Italian immigrant whose stay in the United States is memorialised in relation to his swindling of US $ 20 million from investors in the 1920s. The amount would be equivalent to cool US $ 258 million in today’s terms and stands to reason why a specific type of financial fraud is now known as ‘Ponzi schemes’, with reference to Charles.

The investors who entrusted Charles with their hard-earned money were under the impression that there was an opportunity to capitalise on foreign currency fluctuations by purchasing discounted postal reply coupons from other countries and selling them at full value in the United States. While the ploy sounds clever enough and arbitrage is a very real source of income for many investors in financial markets even today, Charles was unable to follow through on the returns he promised his investors.

In fact, the promised return is a good place to start understanding what a Ponzi Scheme is. Charles, in 1920, promised his investors up to 100 percent profits on their capital invested within a 90-day time window. What the investors didn’t quite understand till much later presumably is that the returns they were getting were generated from new investors, who were entering the scheme and whose profits in turn will depend on future investors that Charles was in the process of convincing to join in.

“History repeats itself but in such cunning disguise that we never detect the resemblance until the damage is done.”

- Sydney J. Harris

History is ripe with examples in the vein of Charles. In actual fact, Charles, although the owner of the moniker is not even the first known swindler to employ a Ponzi Scheme. Twenty one-year old William Miller defrauded over 13,000 investors for a total of US $ 1 million in 1899. Miller’s business the ‘Franklin Syndicate’, promised investors 520 percent annualised returns on their investments, by virtue of which Miller himself came to be known as “520 percent Miller”.

As you may imagine, Miller’s promises, much like those made by Charles, met with tragic endings and while there is no recorded insight on the damage caused, it isn’t beyond imagination to think that some part of the investors may have lost more than they could afford to.

“There are some frauds so well conducted that it would be stupidity not to be deceived by them.”

- Charles Caleb Colton

The story so far clearly explains every feature of a Ponzi Scheme. These types of schemes promise unrealistic returns, have no tangible means to generate promised returns and actively recruit new investors continuously. Additionally, most such schemes will also present investors with the opportunity to add to their earnings by introducing other investors to the scheme.

To any reasonable reader and even more so, to someone with exposure to managing investments, it may seem a laughable prospect to fall prey to such a thinly disguised scam. After all, that’s all it really is, Ponzi schemes are elaborate scams and they are guaranteed to collapse in time. Right?

I may in the past have agreed with the notion that only a fool would fall for this type of scam. However, having seen close friends, colleagues and family invest in and lose money to Ponzi schemes, I’ve come to realise that it really isn’t a case of foolery. There is an underlying psychological aspect as well as an economic vulnerability that is priming Sri Lankans to be the ideal prey for this type of racket.

Psychologically, it must be recognised that Ponzi schemes mimic financial institutions in a somewhat abstract way. In that, they recruit new investors actively, promise returns and are intrinsically unsustainable business models in the event that new capital flow halts. Further, financial literacy is not a hallmark outcome of the Sri Lankan educational system. We are not taught how money works in the real world, in practical terms till much later in life and most Sri Lankans never really acquire an understanding of complex financial instruments.

Our collective psyche as a nation is a highly vulnerable breeding ground for swindlers, who come armed with elaborate investment opportunities and foggy details of how profit is generated. In fact, the oldest trick in the book that Charles devised itself may successfully fool a number of Sri Lankans had it been run today.

Economically, Sri Lanka is in dire straits, with the government declaring the economy is in its most challenged state since gaining independence. The mounting pressure to maintain quality of life against the rapidly rising rate of inflation and the high-yield promises made by Ponzi schemes in short-term windows is a recipe for disaster.

It stands to reason in this context that there is an outbreak of Ponzi schemes rampant in the country. While the Banking Act recognises Pyramid and Ponzi schemes as being illegal activities, these schemes operate with a level of anonymity that is difficult to be traced.

Wood to the fire is the advent of cryptocurrencies to the local market. Given their intrinsically decentralised transfer protocol, cryptocurrencies make it impossible for perpetrators to be tracked and also allow for foreign Ponzi schemes to enter the country with relative ease.

“We do not live in an economy, we live in a Ponzi scheme.”

- Douglas Rushkoff

Part of why even savvy investors fall prey to these schemes, especially ones that are based on virtual currencies, is the method of elaboration used by scammers when designing these schemes.

At their very core, Ponzi schemes bear a remarkable resemblance to Pyramid schemes and are self-sustaining financial models so long as cash outflows can be matched by inflows. The distinctive separation between a Pyramid or Ponzi scheme and a legitimate investment opportunity is their inherent lack of ability to generate value outside of the cash inflows that they generate from onboarding new investors.

Bonds, stock, commercial papers, bank deposits and other financial instruments generate profits from the pools of liquidity that they raise from investors, thereby securing their ability to repay investors at the close of the investment tenure. Investments made towards assets such as precious metals and real estate sustain and appreciate their value based on the price discovery of the underlying asset class. In stark contrast, Ponzi and Pyramid schemes have no intrinsic method for value generation and depend exclusively on new investments to build liquidity, which is in turn used to pay off early investors who exit the scheme.

To their credit however, the complexities with which Ponzi schemes are designed, differ dramatically to the extent that some large and notable ones closely resemble legitimate investment opportunities.

If you recall the ‘Sahara’ branding, which appeared on the Indian National Cricket team’s playing kit from years 2001 to 2013, you will no doubt be surprised to know that ‘Sahara India Pariwar’ was controversially accused of operating a complex Ponzi-type scam, which involved the swindling of US $ 3.2 billion from nearly three million, many of whom were rural-dwelling poor Indians.

While it’s inaccurate to call Sahara a classic case of Ponzi, there are undebatable similarities between the microfinancing scheme they operated and the modus operandi of a Charles or Miller. The inability to diagnose this type of large scam as a Ponzi scheme without argument and the fact that legal implications for those who operated the Sahara organisation including its flamboyant chief - Subrata Roy, who served only two years in jail and is now released on parole are all the reasons why a Ponzi scheme is a lot more likely to catch you off-guard than you would initially imagine.

“We do not live in an economy, we “Curiosity pulls people into the scam.”

- Frank Stallone

Spotting a Ponzi scheme is the simplest thing for many people who have a firm belief in things that are too good, always being unlikely to be true. For the rest of us, who find our curiosity and imaginative optimism harder to suppress, all hope is yet not lost. A Ponzi scheme regardless of its elaborate design and complex operating protocol depends on a number of features that are essential for its sustenance.

The first feature of a Ponzi scheme is unrealistically lucrative promises of profit. Consider for a moment that the effective interest rate of a fixed deposit instrument offered by any accredited financial institution in Sri Lanka hovers around 6 percent to 8 percent at the time of my writing. Most Ponzi schemes will promise to outperform standard investment options by large margins. Some schemes I have been introduced to promise returns as high as 100 percent on capital employed within a matter of weeks. While high returns themselves are not a definite indicator, it should clue you in on the fact that the risk factor involved must certainly be considerably higher.

The second feature of a Ponzi scheme is the promise of guaranteed returns. Aside from a financial institution whose capital adequacy is regulated by a central authority, the possibility of returns being guaranteed is questionable. Almost all high-yield investment options, including the trade of stocks and cryptocurrency, come with high intrinsic risks. A highly lucrative return on investment, combined with a guarantee on returns without a caveat is almost always a tell-tale sign that the scheme operator is disclosing less than complete information.

Thirdly, Ponzi schemes notoriously struggle to explain how returns are generated. In the case of a stock or a fund, the underlying asset is clearly defined and the process by which profit is generated is easily identifiable. For example, a company stock fundamentally depends on the value of the entity that issued the stock appreciating in an exchange in which the liquidity of said stock can be exercised. In the case of an asset such as a precious metal or a motor vehicle, the commodity market in which the asset can be sold should recognise the asset to be of appreciating value. Ponzi schemes often present elaborate explanations of how the returns are generated but some quick research on how these markets operate will clue you in on the unlikeliness of the explanation holding true.

Fourthly, Ponzi schemes and scheme operators will maintain high levels of anonymity. This is achieved primarily by having no proof of legitimate incorporation, no directly attributable presence of a management team and no banking infrastructure. It’s not uncommon for scammers to request cash or cryptocurrency payments from investors, exempting them from having to disclose any documented form of accountability such as a bank account.

Ponzi schemes will also detail elaborate roadmaps of events that are scheduled to occur in the not-so-distant future, such as office openings, listings on exchanges and the launch of media campaigns. These efforts are focused on building confidence and sometimes include frequent updates of investor meetings and events hosted in other countries and cities with the participation of large groups of investors.

Finally and most definitely, Ponzi schemes will always provide a mechanism for investors to invite and onboard other investors to the scheme. These invitation/referral mechanisms will be incentivised through elaborate payment structures by which sign-up bonuses and recurring commissions can be earned. As a rule of thumb, any scheme, which generates more lucrative returns for investors through the process of referral as opposed to the market performance or value appreciation of an asset, is almost always a Ponzi scheme. The one rare exception to the rule is multi-level marketing (MLM) schemes such as Oriflame that have the makings of a Ponzi scheme but have succeeded in creating a sustainable model of value generation to extend the lifecycle of the business.

“I don’t invest in anything I don’t understand.”

- Warren Buffet

Generating returns on investments is an essential piece to the puzzle of creating wealth and is largely what separates the rich from the poor in a capitalist economy. The scalability and profoundly exponential nature of a well-managed investment portfolio is the key to achieving financial independence and securing assets against macroeconomic risk factors such as inflation and currency debasement. However, the need for understanding the fundamentals of assessing an investment is unsurmountable in the modern financial landscape.

The tumultuous economic condition that the Sri Lankan and at large the global economy is undergoing at present and the rising popularity of the stock market, cryptocurrencies and other investment avenues is the perfect storm for Ponzi and Pyramid schemes to mushroom.

With the prevalence of the internet, the exposure of retail investors to investment opportunities both legitimate and illegitimate has increased profoundly. However, the savviness of the average investor when compared with an institutional investor and the tools available to the average individual to carry out due diligence are limited and hence should be the reason for double the caution.

While nothing can replace the value of thorough research and education on the basic concepts of how investments generate value and what the risks associated with such investments are, a watchful eye on the parallels between how a Ponzi scheme works and any suspicious investment options presented to you should be a reasonable guardrail. Be sure to educate anyone who might be pitching such an investment to you, while also refraining from letting curiosity get the better of you.

As a final thought, consider these words from Warren Buffet, the Oracle of Omaha: “The first rule of investing is not to lose money. The second rule is to remember the first rule.”

(Dilshan Senaratne, MBA (UK), GDM-Mgt (UK), Dip (US), leads communication for APAC and EME for a US $ 1 billion global technology blue chip headquartered in the US. He is also Founder and former CEO of Cyaniq Global LLC, a specialised consulting and advisory service firm based in Colombo)