Reply To:

Name - Reply Comment

By First Capital Research

The secondary market activity remained subdued, evident through limited volumes and low levels of activity.

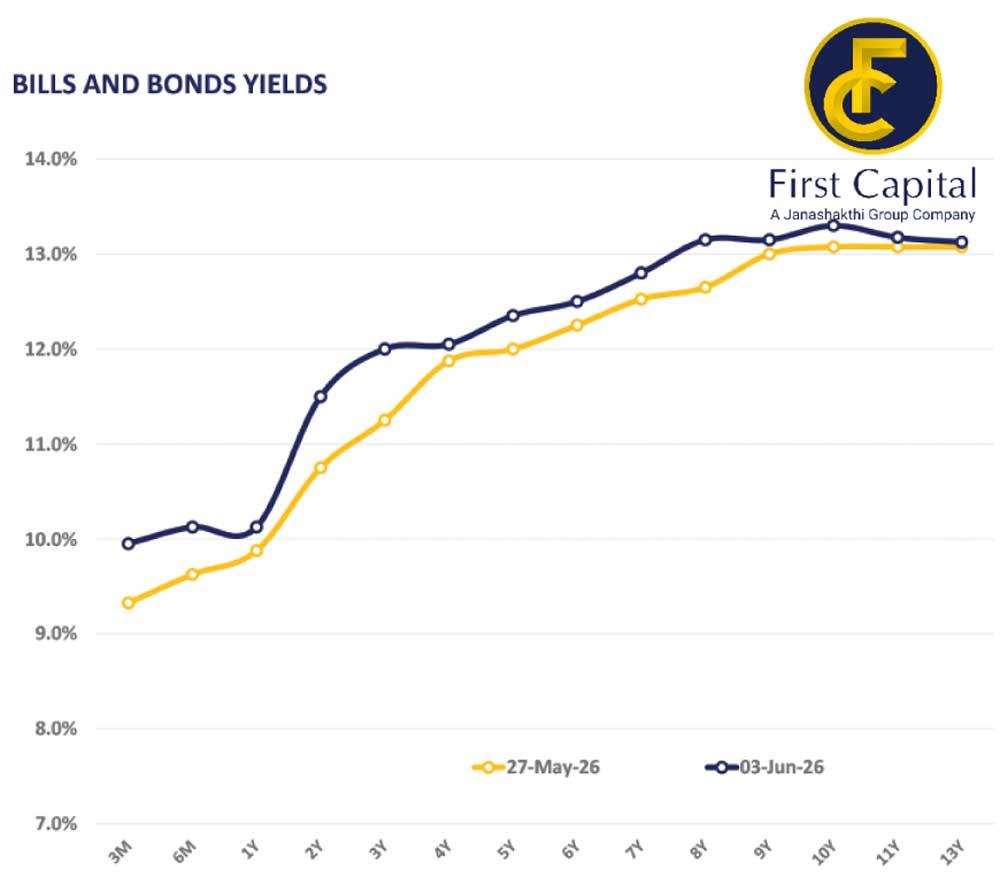

The weighted average yields edged upward across all tenures at yesterday’s T-bill auction, resulting in an upward adjustment across the yield curve.

At the short end of the yield curve, the 01.05.2028 and 01.07.2028 maturities traded from 11.60 percent to 11.75 percent. Moving on to the 2029 bonds, the 15.10.2029 and 15.12.2029 maturities traded between 12.05 percent to 12.10 percent.

At the belly end, the 01.07.2030 and 01.08.2030 maturities attracted some activity, trading at 12.15 percent. Moving further along, the 01.06.2034 and 15.03.2035, both traded at 13.15 percent.

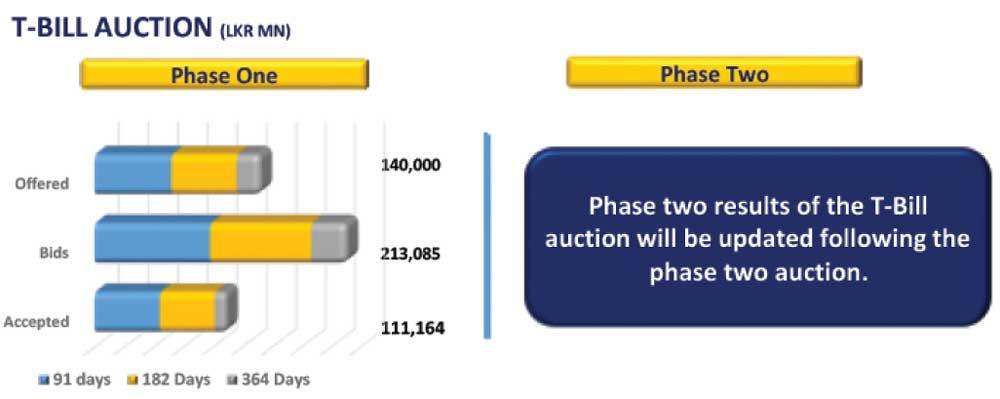

At yesterday’s T-bill auction, the PDMO raised only a portion, totalling to Rs.111.2 billion, compared to the initial offer of Rs.140.0 billion. The three-month bill raised Rs.55.2 billion, falling short of its offer of Rs.65.0 billion, while the six-month and 12-month maturities raised Rs.46.3 billion and Rs.9.6 billion, compared to the offered amounts of Rs.55.0 billion and Rs.20.0 billion, respectively.

The weighted average yields edged up across the board, with the three-month yield edging up 48bps to settle at 9.84 percent, the six-month yield edging up 33bps to 10.01 percent and the 12-month bill edging up 19bps to 10.02 percent.

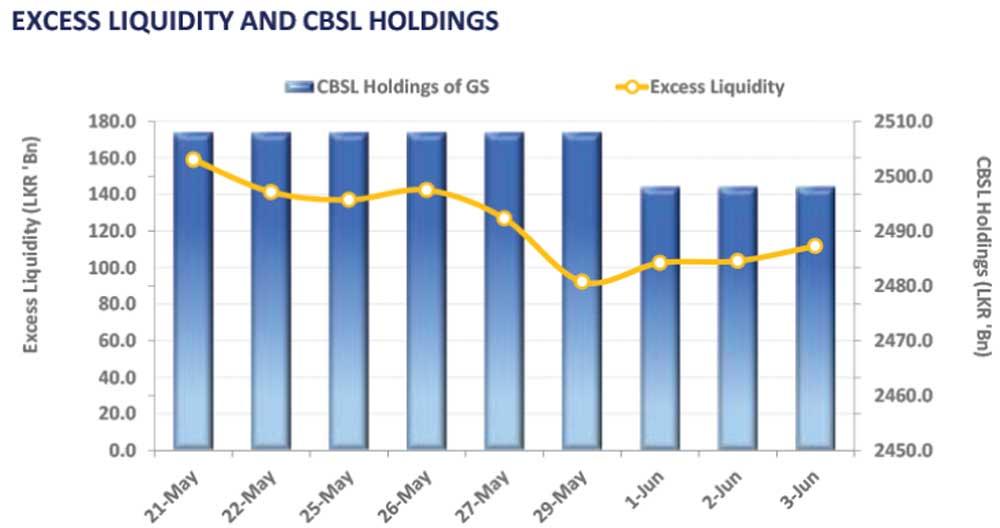

On the external front, the Sri Lankan rupee depreciated against the US dollar, standing at Rs.332.16/US dollar, compared to Rs.331.58/US dollar seen earlier. Liquidity in the banking system expanded to Rs.111.71 billion, from Rs.103.56 billion recorded previously.