Reply To:

Name - Reply Comment

By First Capital Research

Pivoting from the previous day’s sentiment ahead of the bond auction, the secondary market witnessed a mixed sentiment with moderate volumes and low activity.

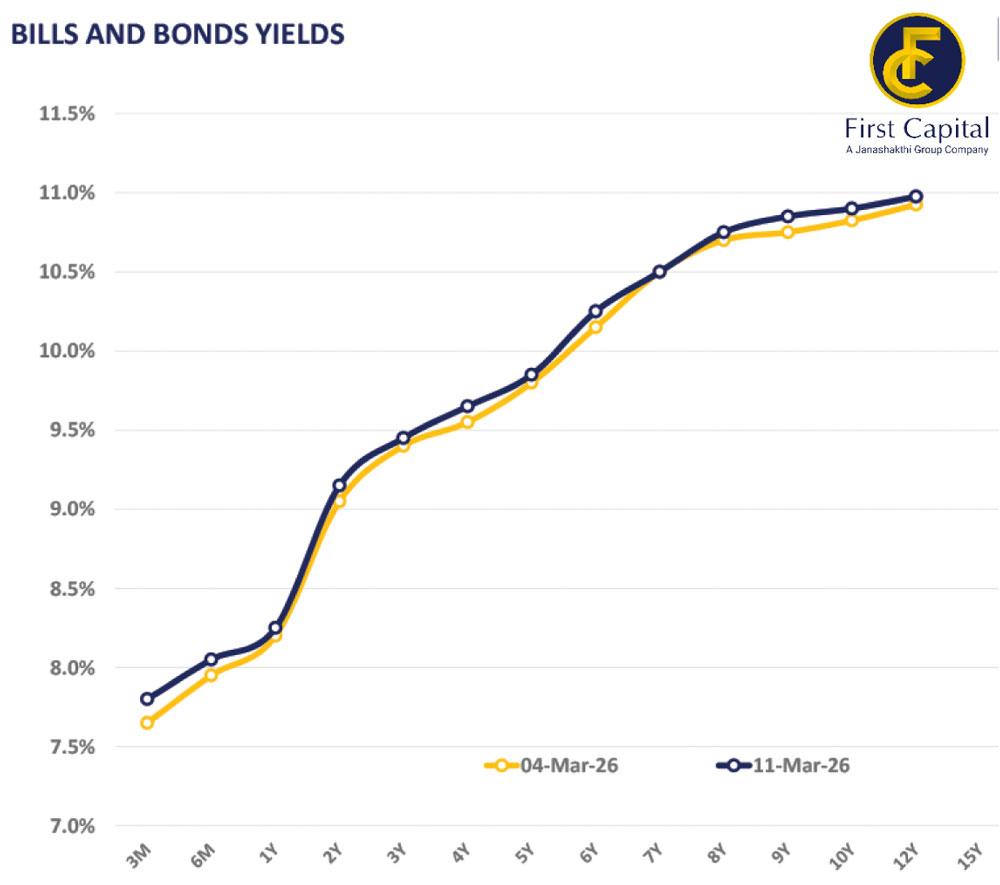

At the short end of the curve, 15.02.2028 and 15.03.2028 were seen trading in the range of 9.12 percent to 9.15 percent.

Moving along the curve, 15.09.2029, 15.12.2029, 01.03.2030 and 01.06.2033 changed hands at 9.50 percent, 9.55 percent, 9.65 percent and 10.50 percent, respectively.

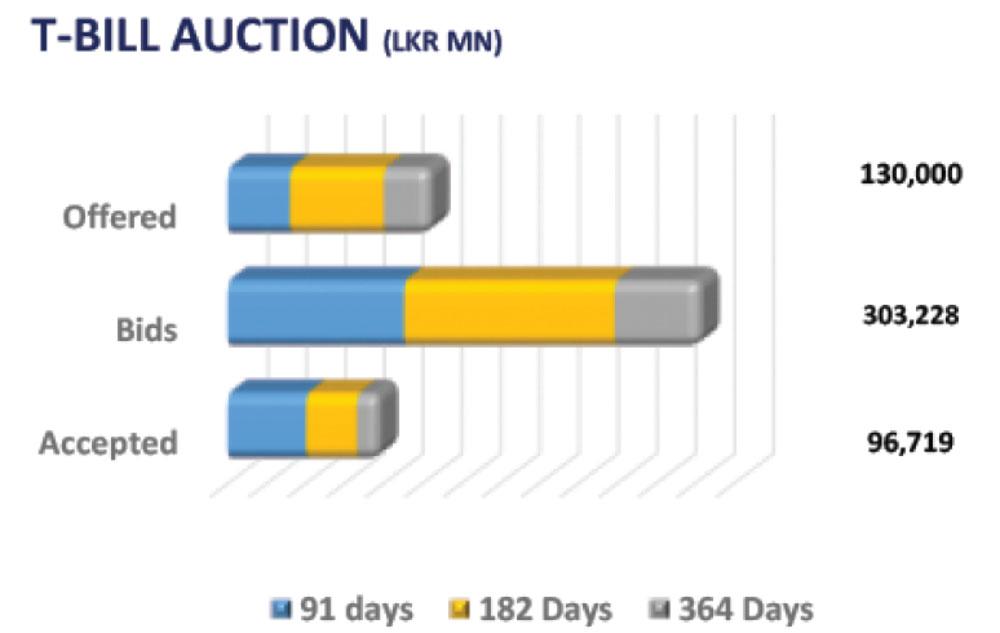

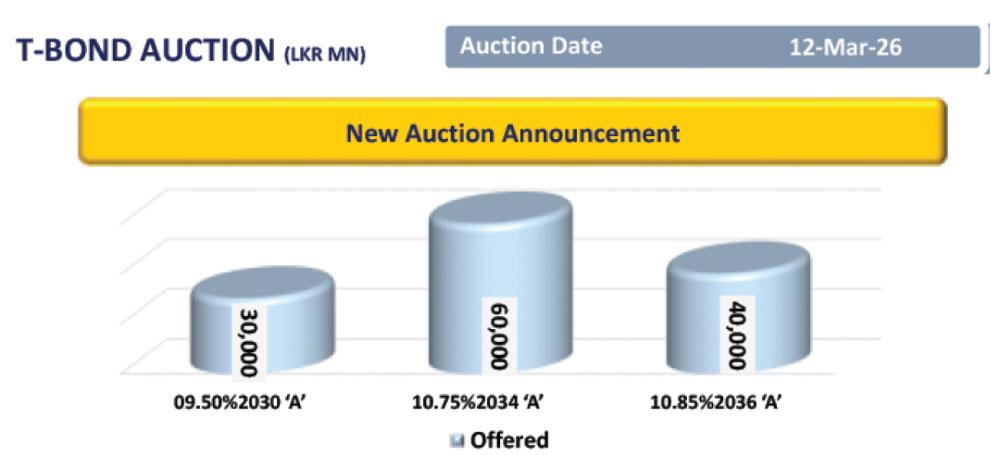

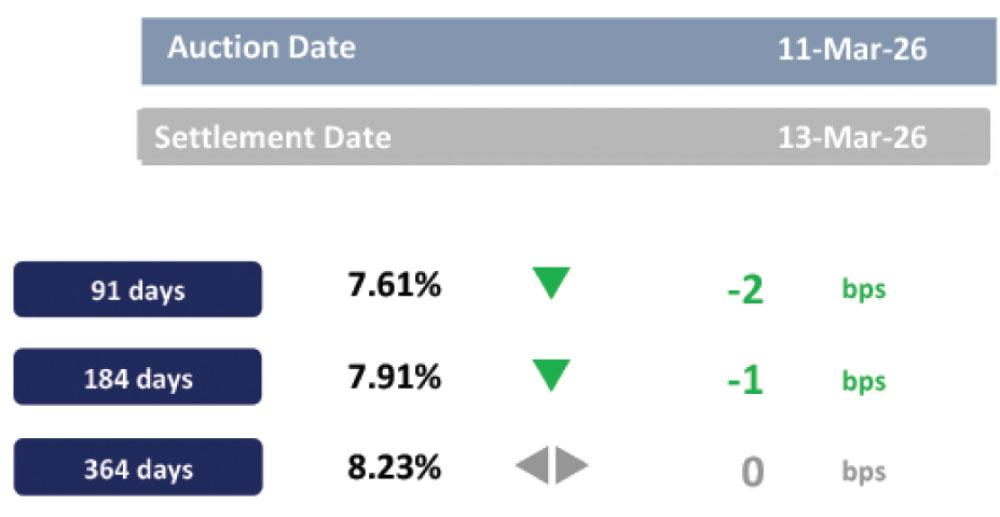

Further ahead on the curve, the 15.06.2034 maturity traded in the range of 10.75 percent to 10.76 percent. At the T-bill auction, the PDMO raised only a portion, totalling to Rs.96.7 billion, compared to the initial offer of Rs.130.0 billion.

However, the three-month raised Rs.50.5 billion, surpassing its offer of Rs.40.0 billion, while the six-month and 12-month maturities raised Rs.32.3 billion and Rs.13.9 billion, compared to the offered amounts of Rs.60.0 billion and Rs.35.0 billion, respectively.

Weighted average yields of the three-month and six-month maturities decreased by 2bps and 1bps, respectively to 7.61 percent and 7.91 percent, while the 12-month remained unchanged at 8.23 percent.

On the external front, the Sri Lankan rupee appreciated against the US dollar, closing at Rs.311.12/US dollar, compared to Rs.311.73/US dollar recorded the previous day.

Overnight liquidity in the banking system contracted to Rs.394.53 billion, from Rs.410.36 billion recorded previously.