Reply To:

Name - Reply Comment

Vice President – Research Charith Gamage brings over 16 years of experience in research, capital markets and financial institutions. He holds a PhD in Finance from Monash University, Australia, and a Master’s degree from the University of California, Berkeley, USA

Senior Research Analyst Akna Tennakoon specialising in macroeconomic research, econometric analysis, and sector research. She holds an Honours Degree in Economics from the University of Colombo and is currently pursuing a Master’s Degree in Economics at the same in addition to actively contributing to economic research

Q Why did First Capital Research choose Greece and Jamaica as comparators for Sri Lanka’s post-crisis recovery?

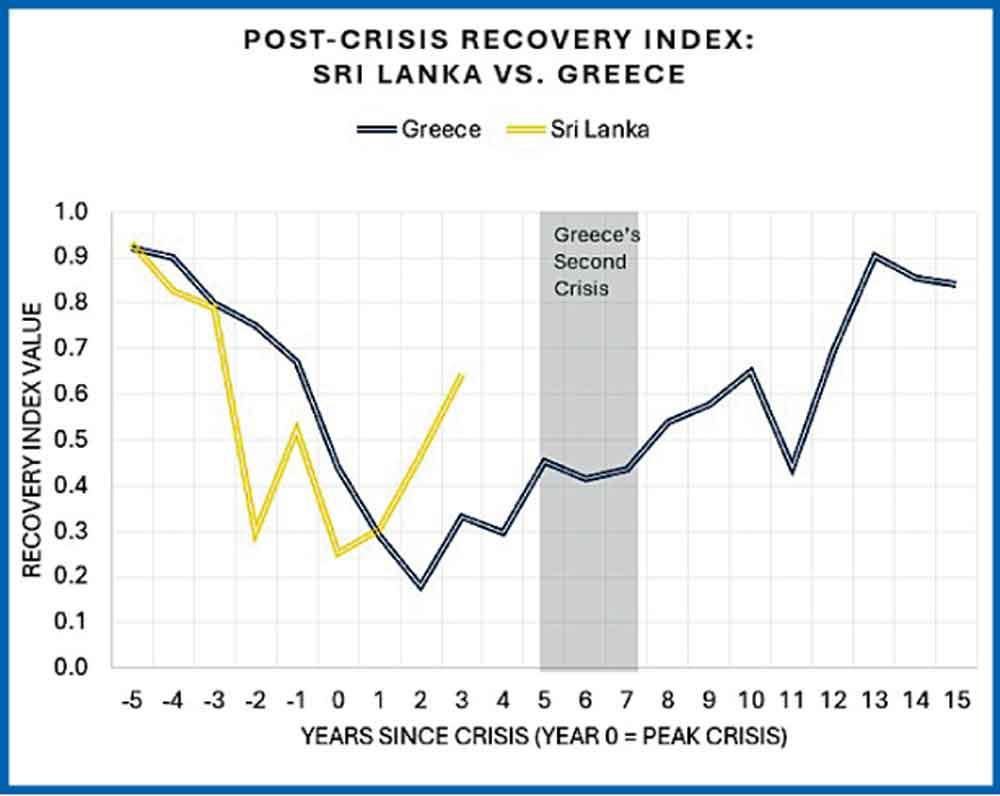

Charith: Sri Lanka is not the first country to face a debt crisis. Several economies have gone through similar hardships, and their recovery paths offer useful lessons on what supports stability, what delays it, and what can go wrong after the initial adjustment phase.We chose Greece because it shares a number of similarities with Sri Lanka. Greece’s crisis emerged in 2009–2010, after years of structural weaknesses had accumulated, fiscal imbalances, weak revenue mobilisation, external vulnerabilities, and low competitiveness. These problems did not emerge overnight, they built up over time and eventually became difficult to absorb when financial stress struck.

Greece is also relevant because its recovery was shaped not just by economics, but by politics. Austerity created resistance, policy continuity weakened, and confidence took longer to rebuild. These are useful lessons for Sri Lanka as the country moves through its recovery phase.

Jamaica, meanwhile, presents a different risk. It restored debt sustainability through strong fiscal discipline, but growth stayed weak for a prolonged period. Together, Greece and Jamaica illustrate the two traps Sri Lanka must avoid, reform fatigue and policy inconsistency on one side, and stability without growth on the other.

Q What was the most important takeaway from Greece’s crisis?

Charith: The key lesson from Greece is that stabilisation is not the same as recovery.

Greece’s early adjustment helped restore some macroeconomic stability, but the economy remained fragile for years because reforms were not always sequenced or sustained properly. Early IMF-led stabilisation was necessary, but it also came with a sharp drag on growth.

Recovery only became more durable when Greece moved through a clearer reform sequence, first macro stabilisation, then domestic fiscal and institutional reforms, and finally a growth-oriented agenda focused on competitiveness, investment, and private-sector activity.

This sequencing matters. If a country focuses only on repairing the balance sheet, it may create stability, but not necessarily durable growth. For Sri Lanka, the message is that the current phase should not be treated as the end of the adjustment story. It is only the beginning of a longer process.

Q How important were political cycles in Greece’s recovery path?

Charith: Very important. In Greece, politics and economics reinforced each other throughout the crisis period. As recession deepened and austerity continued, public dissatisfaction rose. This created political instability, repeated leadership changes, and policy uncertainty.

This matters because every time the political direction shifted, market confidence weakened. Investors need clarity and consistency. When these factors are missing, recovery becomes slower and more fragile.

The 2015 episode was especially important. Negotiations broke down, bank closures and capital controls were imposed, and confidence deteriorated again. That second crisis episode delayed recovery further and showed how political disruption can reverse progress even after initial stabilisation.

For Sri Lanka, the lesson is straightforward, that policy consistency, reform credibility, and political consensus matter just as much as fiscal repair. Without a stable direction, the country’s recovery can easily lose momentum.

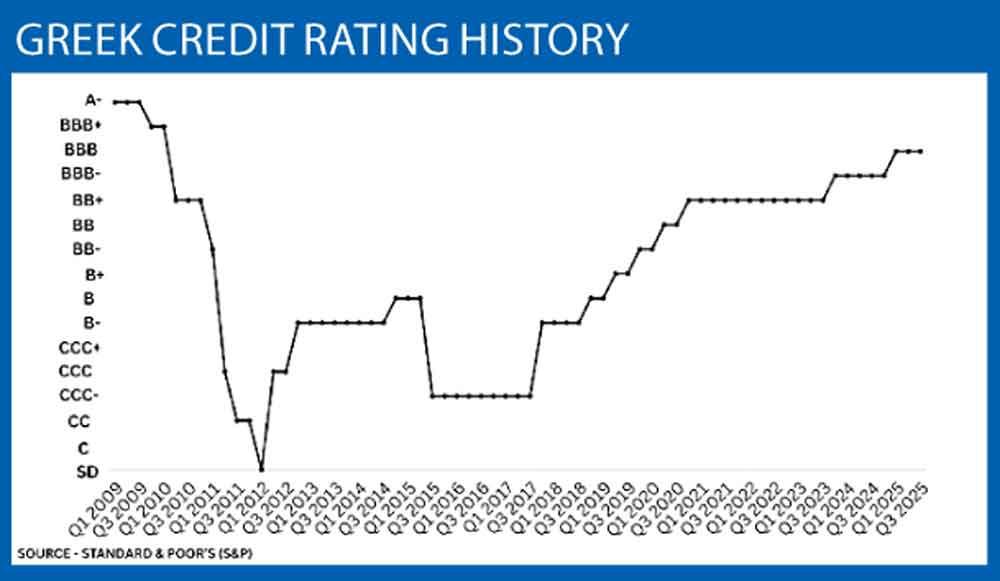

Q What did Greece’s credit rating trajectory tell you about crisis recovery?

Charith: Credit ratings are a useful signal of how credibility is rebuilt. In Greece, ratings improved at first after the initial adjustment, but those gains were fragile. When the second crisis hit in 2015, progress stalled again.

The broader lesson is that credit recovery follows credibility, and credibility takes time. It does not happen immediately after a debt restructuring or an IMF programme. It improves when reforms are delivered consistently, fiscal discipline is maintained, and policy stability becomes visible over time.

For Sri Lanka, this means rating improvements will depend on more than the first phase of stabilisation. They will depend on reform delivery, successful debt-deal execution, and a sustained return to market access. Early upgrades are encouraging, but they must be backed by consistent policy action.

Q Why is Jamaica relevant to this post-crisis discussion?

Akna: Jamaica is relevant because it shows what happens when a country restores debt sustainability, but growth remains weak for too long.

Its crisis was the result of a long build-up of domestic imbalances, weak fiscal discipline, low investment in productive areas, structural inefficiencies, and an unsustainable debt burden. Over time, debt became increasingly difficult to service, and growth was not strong enough to support the economy.

This makes Jamaica an important cautionary tale for Sri Lanka. Jamaica’s case shows that fiscal consolidation can restore stability, but if growth does not revive alongside it, the economy can remain stuck in a low-growth equilibrium.

For Sri Lanka, the challenge is not only to repair public finances, but to ensure that repair translates into private sector activity, investment, and long-term growth.

Q How did Jamaica’s first debt restructuring fall short?

Akna: Jamaica’s first restructuring in 2010, the Jamaica Debt Exchange, did deliver immediate relief. It was a voluntary, par-neutral exchange that lowered interest costs and extended debt maturities, which eased short-term pressure.

But it did not solve the underlying sustainability problem. The principal debt stock was not reduced, so the burden remained very high. Fiscal slippage also weakened the adjustment effort, while growth stayed subdued because investment remained weak. In addition, debt linked to state-owned entities complicated the situation further.

So the gains from the first restructuring proved temporary. This is why Jamaica had to go back into restructuring again in 2013.

The lesson for Sri Lanka is that temporary relief is not enough if the reform base is incomplete. A restructuring can buy time, but that time has to be used to strengthen the fiscal and growth foundations of the economy.

Q What changed in Jamaica’s second restructuring, and what was the trade-off?

Akna: Jamaica’s second restructuring was much more comprehensive and disciplined.

It introduced legally binding fiscal rules, tighter control of public sector wages through multi-year agreements, improved tax administration, greater debt transparency, expanded reporting of liabilities, and stronger oversight of state-owned enterprises. These reforms helped create a more credible fiscal framework and put public debt on a sustained downward path. But the trade-off was clear. Growth remained weak for a long time, public investment stayed low, and private sector expansion was limited. So, while Jamaica achieved stability, it came at the cost of subdued economic momentum.

This is the important lesson for Sri Lanka. Fiscal discipline is essential, but it should not come at the expense of long-term growth. Stability must be supported by policies that keep the economy moving forward.

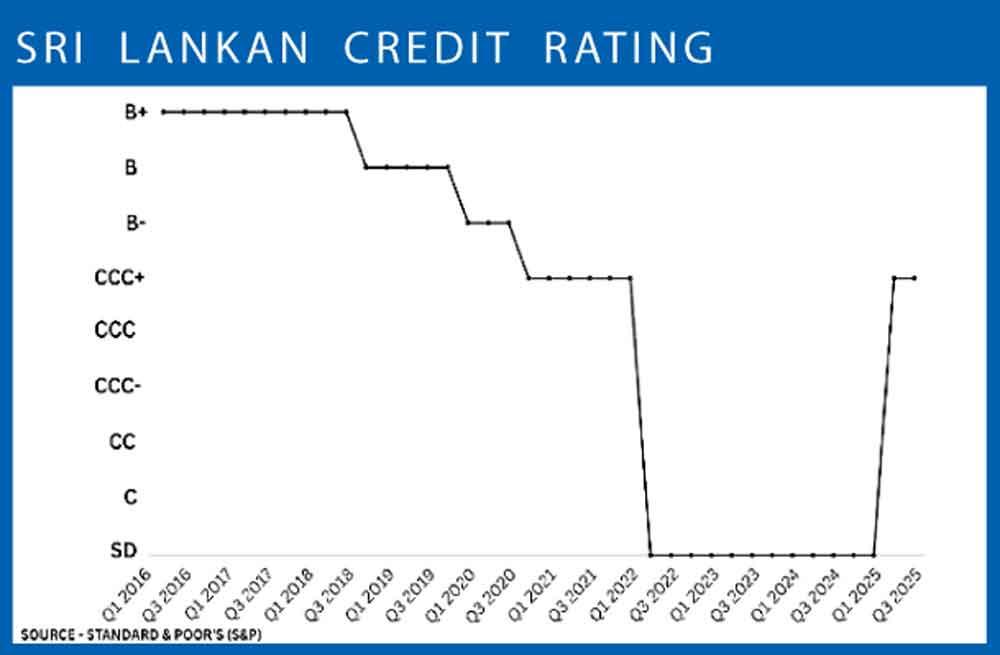

Q Sri Lanka appears to have stabilised faster than both Greece and Jamaica. Is that fair to say?

Charith: Broadly, yes. Sri Lanka’s early stabilisation has been relatively sharp. Fiscal balances have improved, sovereign risk has started to normalise, and external conditions have recovered faster than in many comparable cases.

In that sense, Sri Lanka’s starting point after crisis looks better than what Greece had at similar stages.

But early stabilisation is only the beginning. The real test is what happens next. The economy now has to move from balance sheet repair to durable growth. This means reform delivery must continue, private investment must pick up, and productivity has to improve.

So yes, Sri Lanka has stabilised relatively quickly. And more importantly, it is currently in a better position than both Greece and Jamaica were at similar points in their recovery paths. But the durability of the country’s recovery will depend on whether that stabilisation is converted into a stronger growth path.

Q Can Sri Lanka’s current account improvement be misleading?

Charith: Yes, it can be.

A better current account number does not automatically mean the economy has become stronger. We need to look at what is driving the improvement. If the current account is improving mainly because domestic demand is weak and imports have been compressed, then that is not the same as a healthy external recovery. In Sri Lanka’s case, capital goods imports have remained subdued, which suggests investment demand is still weak. Tourism and remittances may also remain vulnerable. So the improvement needs to be interpreted carefully.

This is similar to what happened in Greece. There, the current account improved largely because imports collapsed as demand contracted. It was a recession-driven adjustment, not a competitiveness driven one. When growth returned, the deficit reappeared because the underlying external weaknesses had not been fully fixed.

Sri Lanka should avoid that outcome. Real external strength must come from export growth, better competitiveness, stronger investment, and higher productive capacity.

Q What is the most important policy takeaway from this comparative study?

Akna: The main takeaway is that recovery is a process, not a single event.

Greece shows the cost of delayed reforms, policy reversals, and austerity fatigue. Jamaica demonstrates the risk of restoring stability but failing to generate enough growth. Sri Lanka now has the opportunity to avoid both of these traps. For recovery to be durable, stabilisation has to be followed by deeper reforms that restore confidence, support investment, and build growth capacity. This means Sri Lanka must move through three stages. Firstly through macro stabilisation, second through institutional and fiscal reform, and then thirdly through growth-oriented transformation.

Charith: Exactly. Sri Lanka’s opportunity is to turn early stabilisation into durable economic momentum. The challenge is not just to fix the balance sheet, but to ensure the adjustment translates into real economic activity, private sector expansion, and productivity-led growth.

If Sri Lanka can do that, it can avoid the mistakes seen in both Greece and Jamaica and build a recovery path that is both stable and sustainable.