SHABIYA ALI AHLAM

SHABIYA ALI AHLAM

Reply To:

Name - Reply Comment

|

Krishan Balendra |

John Keells Holdings (JKH) delivered one of its strongest operational quarters in recent years in the March quarter, as the conglomerate’s large-scale investments in its integrated resort, port and electric vehicle businesses began making a materially stronger contribution to earnings.

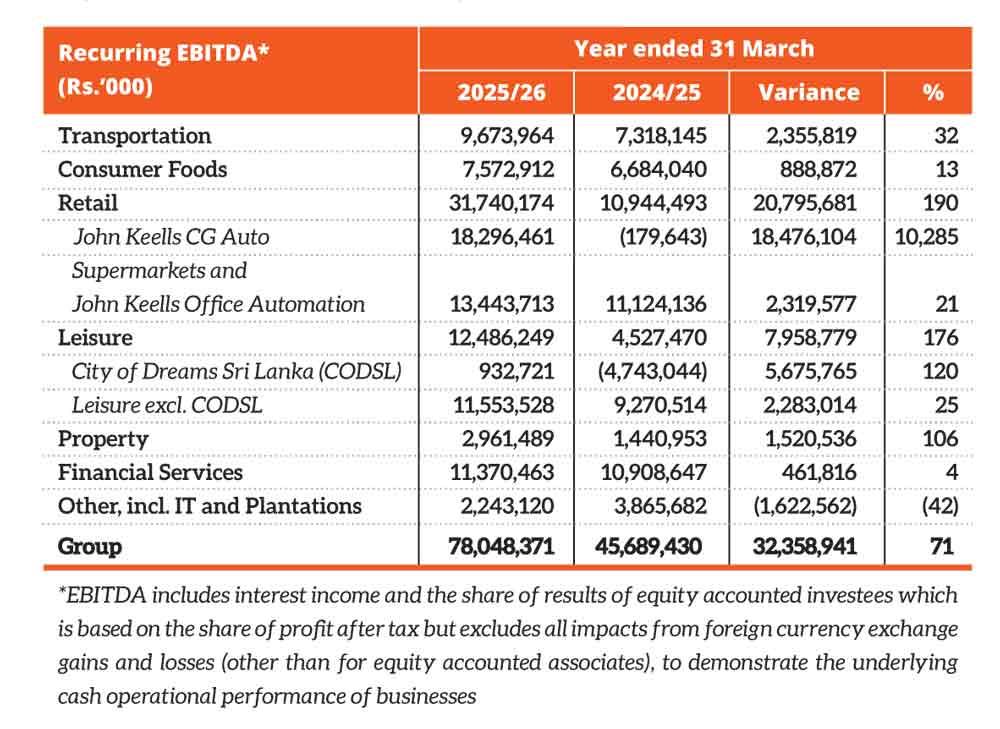

The premier blue-chip conglomerate reported a 51 percent year-on-year (YoY) jump in 4Q recurring EBITDA to Rs.24 billion, as momentum accelerated across its integrated resort, port terminal, bunkering and electric vehicle businesses.

The quarter was particularly significant because it marked the first sustained earnings contribution from City of Dreams Sri Lanka (CODSL), which turned EBITDA positive after years of development-stage losses. CODSL recorded fourth-quarter EBITDA of Rs.1.17 billion, compared with a loss of Rs.1.22 billion a year earlier, as casino operations ramped up and occupancy improved at Cinnamon Life and Nuwa.

JKH said casino operations saw “an encouraging pick-up” from the fourth quarter onwards, with the group currently recognising fixed rental income while variable rental income is expected to scale alongside activity levels.

“The Group is confident that revenue and profitability from the Cinnamon Life hotel and the other components of CODSL will continue to ramp up over the next few quarters. With all elements now operational and booking momentum continuing to build, we expect this positive earnings trajectory to be sustained,” Chairperson Krishan Balendra said.

The transportation segment emerged as another major driver of quarterly earnings, with EBITDA surging 94 percent to Rs.4.15 billion.

That performance was fuelled by record bunkering volumes at Lanka Marine Services (LMS), which benefited from shipping dislocations linked to the Middle East conflict, and the rapid scaling of the Colombo West International Terminal (CWIT).

JKH said CWIT had already reached full annualised utilisation of its phase one capacity within its first year of operations, underscoring both the strength of regional transshipment demand and the speed at which the Port of Colombo absorbed new capacity.

“CWIT recorded strong throughput growth during the year, supported by an improving volume mix, translating into profitability ahead of expectations. I am pleased to state that CWIT handled over one million TEUs for the year, and the terminal has already reached full utilisation of phase 1 capacity based on its latest monthly run-rate, despite being within its first year of operations,” Balendra said.

The results also suggest JKH’s earnings base is becoming increasingly diversified after several years during which heavy capital expenditure diluted returns.

Retail EBITDA rose 93 percent in the March quarter to Rs.6.6 billion, supported by strong supermarket performance and continued momentum at John Keells CG Auto (JKCG), the BYD vehicle distribution business.

JKCG generated Rs.18.3 billion in recurring EBITDA for the full year after handing over more than 10,000 vehicles, making it one of the group’s single largest earnings contributors during the year.

While vehicle demand moderated after the initial post-import reopening surge, JKH said order activity strengthened again during the fourth quarter amid fuel-related disruptions and rising interest in hybrid and electric vehicles.

For the full year ended March 2026, recurring EBITDA rose 71 percent to Rs.78.05 billion, while recurring profit before tax climbed 143 percent to Rs.35.72 billion. Recurring profit attributable to equity holders increased 155 percent to Rs.13.24 billion.

Yet beneath the headline growth, the results also reflected the lingering weight of JKH’s investment-heavy balance sheet.

The leisure segment remained loss-making at the pre-tax level, recording a recurring pre-tax loss of Rs.10.3 billion, largely due to depreciation, amortisation and interest charges linked to CODSL, including exchange losses on the group’s dollar-denominated debt.

The group recognised Rs.10.96 billion in depreciation, amortisation and finance costs related to CODSL during the year, more than double the previous year’s charge, reflecting the commencement of full operations across the integrated resort.

Still, the latest results indicate that JKH may have crossed a broader inflection point after nearly a decade of heavy capital deployment.

Group return on capital employed improved to 9 percent from 5.1 percent a year earlier, while the group said net debt-to-EBITDA stood at around two times.

The earnings trajectory now increasingly hinges on whether CODSL can sustain its operational ramp-up, whether CWIT continues scaling ahead of schedule and whether BYD demand remains resilient after the initial reopening cycle fades.