Reply To:

Name - Reply Comment

|

| Krishan Balendra |

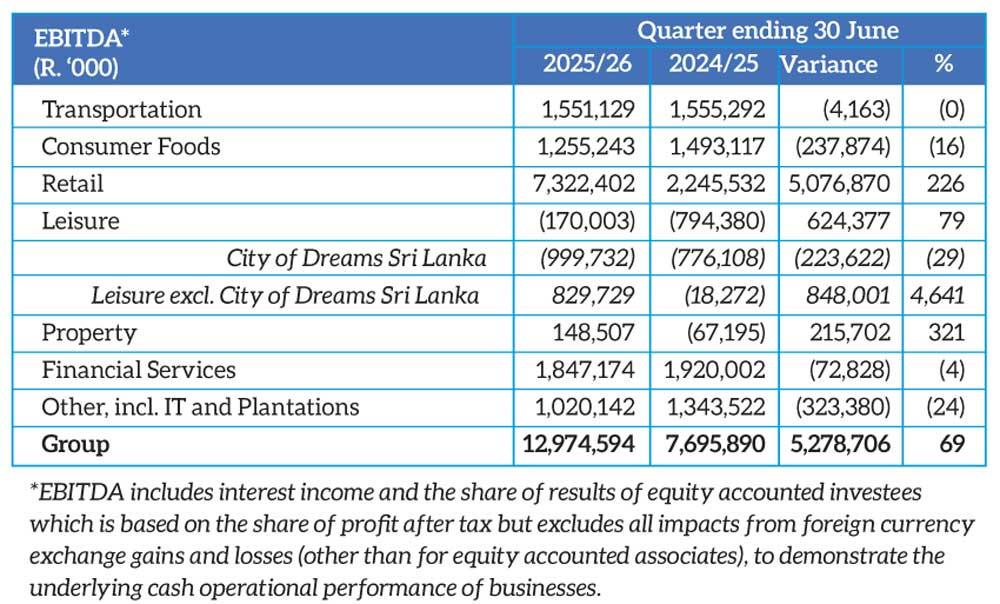

Premier blue-chip John Keells Holdings PLC (JKH) posted a sharp earnings rebound in the first quarter of its current financial year (1Q26), with group revenue expanding 64 percent year-on-year (YoY) to Rs.114.15 billion and group EBITDA rising 69 percent to Rs.12.97 billion.

The improved performance was largely fuelled by the retail segment, particularly supermarkets and new energy vehicles, along with the momentum in transportation, property and banking.

“Group profit before tax (PBT) is an increase over the negative Rs.204 million recorded in the previous financial year,” JKH Chairman Krishan Balendra noted in his quarterly review.

PBT rose to Rs.3.11 billion during the quarter, while profit after tax (PAT) stood at Rs.717 million, reversing a loss of Rs.967 million a year earlier.

Excluding the integrated resort project City of Dreams Sri Lanka, group PBT increased by 306 percent to Rs.7.29 billion and PAT rose 374 percent to Rs.4.91 billion.

However, the group recorded a loss attributable to the equity holders of Rs.804 million, primarily due to the higher losses incurred at WPL, the project company of City of Dreams Sri Lanka, which amounted to Rs.4.19 billion during the quarter, compared to Rs.2 billion in the same period last year. The figure was partially offset by the profit recognition at John Keells CG Auto.

Retail was the standout performer, with EBITDA up 226 percent YoY to Rs.7.32 billion. This was driven by strong contributions from John Keells CG Auto and the supermarket business, which posted a 21 percent increase in EBITDA to Rs.2.45 billion, supported by 13 percent growth in same-store sales and a 17 percent rise in footfall.

Balendra attributed the group’s topline growth to the strength in retail. The group recorded a significant growth in revenue and EBITDA primarily on account of the retail industry group, aided by the performance of the supermarket and new energy vehicle businesses.

The transportation segment recorded a marginal decline in EBITDA to Rs.1.55 billion, reflecting the impact of equity accounting for Colombo West Container Terminal (WCT-1), which commenced commercial operations during the quarter. Excluding WCT-1, transportation EBITDA grew by 11 percent, led by a 13 percent volume increase and improved margins at Lanka Marine Services.

JKH noted that the volume ramp-up at WCT-1 exceeded expectations and operational productivity had scaled significantly. The terminal is expected to reach breakeven earnings within its first year, with the second phase on track for completion in the second half of FY2026/27.

The consumer foods segment posted a 16 percent drop in EBITDA to Rs.1.26 billion, as beverage volumes declined 10 percent amid the unseasonal weather. However, the confectionery volumes rose 3 percent and convenience foods returned to pre-pandemic levels in both volume and profitability.

Financial services EBITDA dipped 4 percent to Rs.1.85 billion. Nations Trust Bank saw improved profitability, supported by credit expansion and lower impairments. Union Assurance delivered premium growth but faced lower investment income, following its bancassurance investment with Sampath Bank.

Meanwhile, property posted stronger earnings through residential sales at Cinnamon Life, TRI-ZEN and VIMAN and from land transactions via Rajawella Holdings.

The group also reported environmental improvements, with an 8.3 percent reduction in carbon footprint and a 9.5 percent drop in water withdrawal per million rupees of revenue, excluding the Cinnamon Life hotel.