Reply To:

Name - Reply Comment

Sri Lanka’s corporate income tax (CIT) collection remains far below the regional peers, raising concerns over the sustainability of government revenue and its post-crisis fiscal recovery, the World Bank (WB) highlighted.

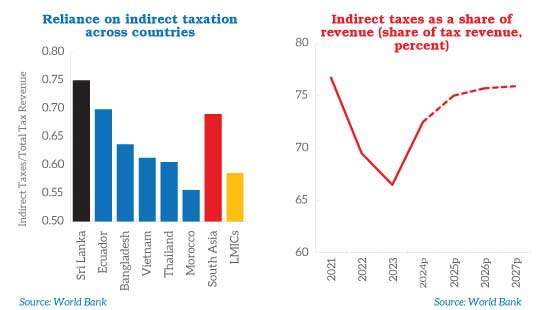

Despite an increase in the statutory CIT rate to 30 percent in October 2022 and the discontinuation of exemptions and concessionary rates, corporate tax collection as a share of GDP in 2023 remained at just 2 percent, compared with 3.5 percent in South Asia and 3 percent in other lower-middle-income countries.

“One of the key reasons for the dependence on indirect taxes is low direct tax take, driven by the weaknesses in CIT collection,” the WB said in the latest Public Finance Review themed ‘Towards a Balanced Fiscal Adjustment’.

It noted that policy choices have created tax-avoidance opportunities and tax expenditures that erode the tax base.

The WB asserted that Sri Lanka’s participation in the OECD’s Inclusive Framework on Base Erosion and Profit Shifting (BEPS) has not yet translated into effective compliance.

Preferential tax regimes such as Strategic Development Projects (SDP), Board of Investment incentives and special economic zones such as Port City Colombo pose significant BEPS risks. The extent to which the multinationals have eroded the tax base through transfer pricing avoidance and shifting profits offshore to low-tax jurisdictions remains unclear, the WB noted.

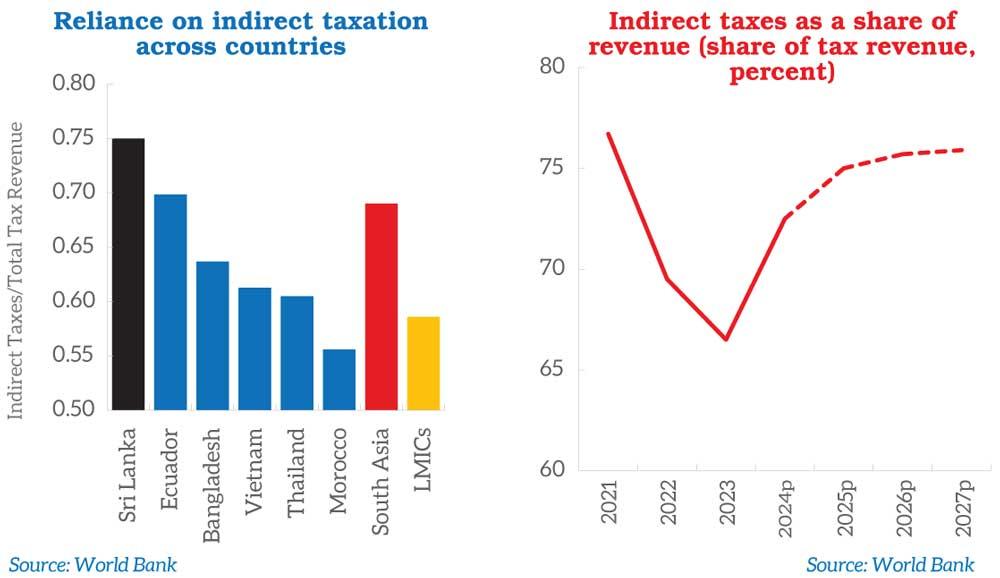

Weak corporate tax productivity is also linked to the country’s heavy reliance on indirect taxes such as VAT and excise duties, it said, which now constitute close to 75 percent of total tax revenue and are projected to remain at that level through 2025. The report cautioned that excessive dependence on indirect taxation reduces progressivity, lowers tax morale and constrains compliance, particularly during a fragile economic recovery.

“The government has committed to reducing tax expenditures but the framework for provision still poses significant challenges,” the international lender cautioned.

It acknowledged that efforts are made to refrain from implementing new tax exemptions and incentives and from approving new projects under the SDP.

However, despite this progress, tax expenditures, particularly for CIT, are likely to increase, given multiple authorising bodies, limited cost-benefit analysis and the lack of sunset clauses.

To address these structural weaknesses, the WB recommends improving the predictability of tax policies, reducing policy and administrative complexity, enhancing coordination across tax policy and administration, engaging in clear and targeted external communications and reporting on tangible benefits from tax revenue and government spending.