Reply To:

Name - Reply Comment

By First Capital Research

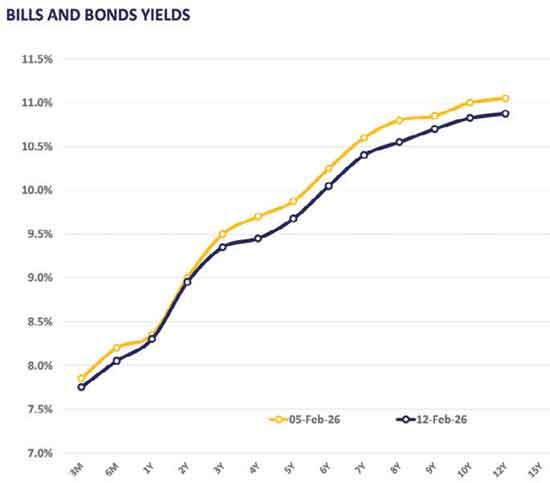

The secondary market yields declined across the curve yesterday, while buying interest persisted amidst large trading volumes.

The secondary market yields declined across the curve yesterday, while buying interest persisted amidst large trading volumes.

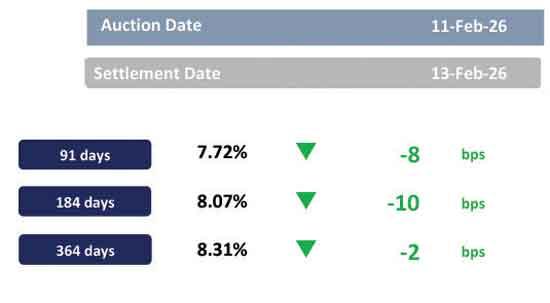

The PDMO concluded the T-bond auction, with theoffersfully subscribed. Over 2029 segment, 15.06.2029, 15.09.2029, 15.10.2029 and 15.12.2029 maturities traded in the range of 9.34%-9.45%.

Moving ahead, 01.03.2030, 15.05.2030 and 01.07.2030 traded within the band of 9.55%-9.50%. Further towardsmid-term maturities, 15.03.2031, 01.10.2032, 01.06.2033 and 15.09.2034 changed hands at 9.70%, 10.10%, 10.38% and 10.60% respectively.

Around the long tenor, 15.06.2035, 01.07.2037 and 15.08.2039 traded at 10.73%, 10.85% and 10.90% respectively.At the T-bond auction, PDMO acceptedits initial offer in full, totaling to Rs. 51.0bn.

Acceptances on 01.03.2030 and 15.08.2036 maturities were Rs. 21.0bn and Rs. 30.0bn while the weighted average yields stood at 9.52% and 10.73% respectively.

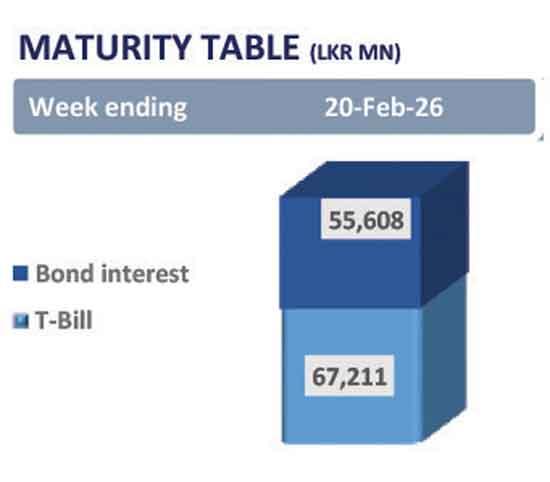

On the external front, the LKR appreciated against the USD, closing at Rs. 309.39/USD compared to Rs. 309.46/USD recorded the previous day. Overnight liquidity in the banking system marginally expanded to Rs. 296.71bn from Rs. 296.45bn recorded previously.