Reply To:

Name - Reply Comment

By First Capital Research

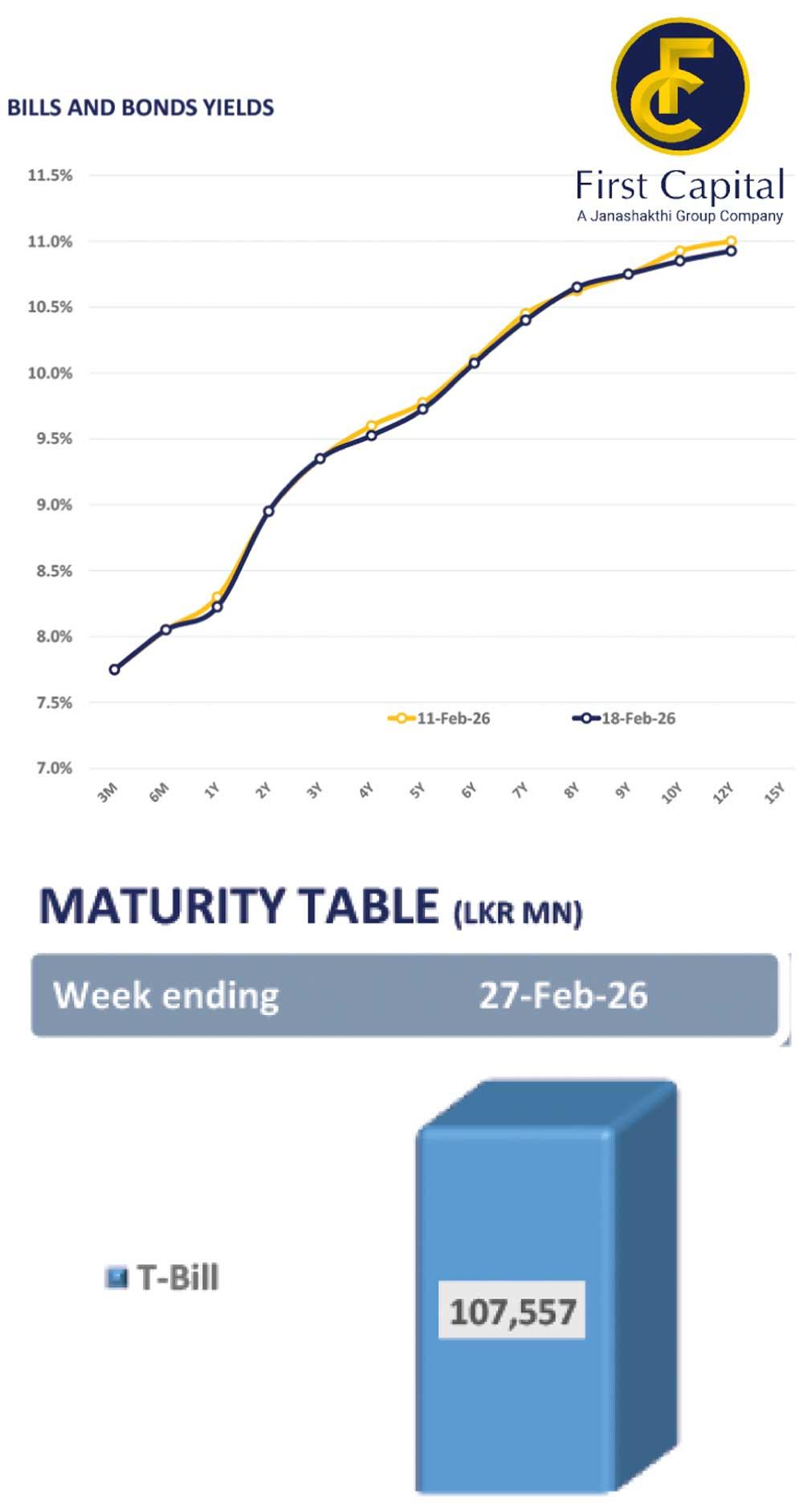

The secondary market yield curve remained largely unchanged, with moderate trading volumes and mixed activity.

Within the 2028 maturities, 15.02.2028, 15.03.2028, 01.07.2028 and 01.09.2028 traded in the range of 8.90 percent to 9.15 percent.

Further along the yield curve, 15.05.2029, 01.06.2029, 15.09.2029 and 15.12.2029 traded between 9.34 percent and 9.50 percent. The 01.03.2030 maturity changed hands at 9.55 percent, while 01.07.2030 and 15.10.2030 were traded at 9.58 percent.

At the longer end of the curve, 15.03.2031, 15.12.2032, 15.06.2032 and 01.07.2037 traded at 9.75 percent, 10.15 percent, 10.75 percent and 10.87 percent, respectively.

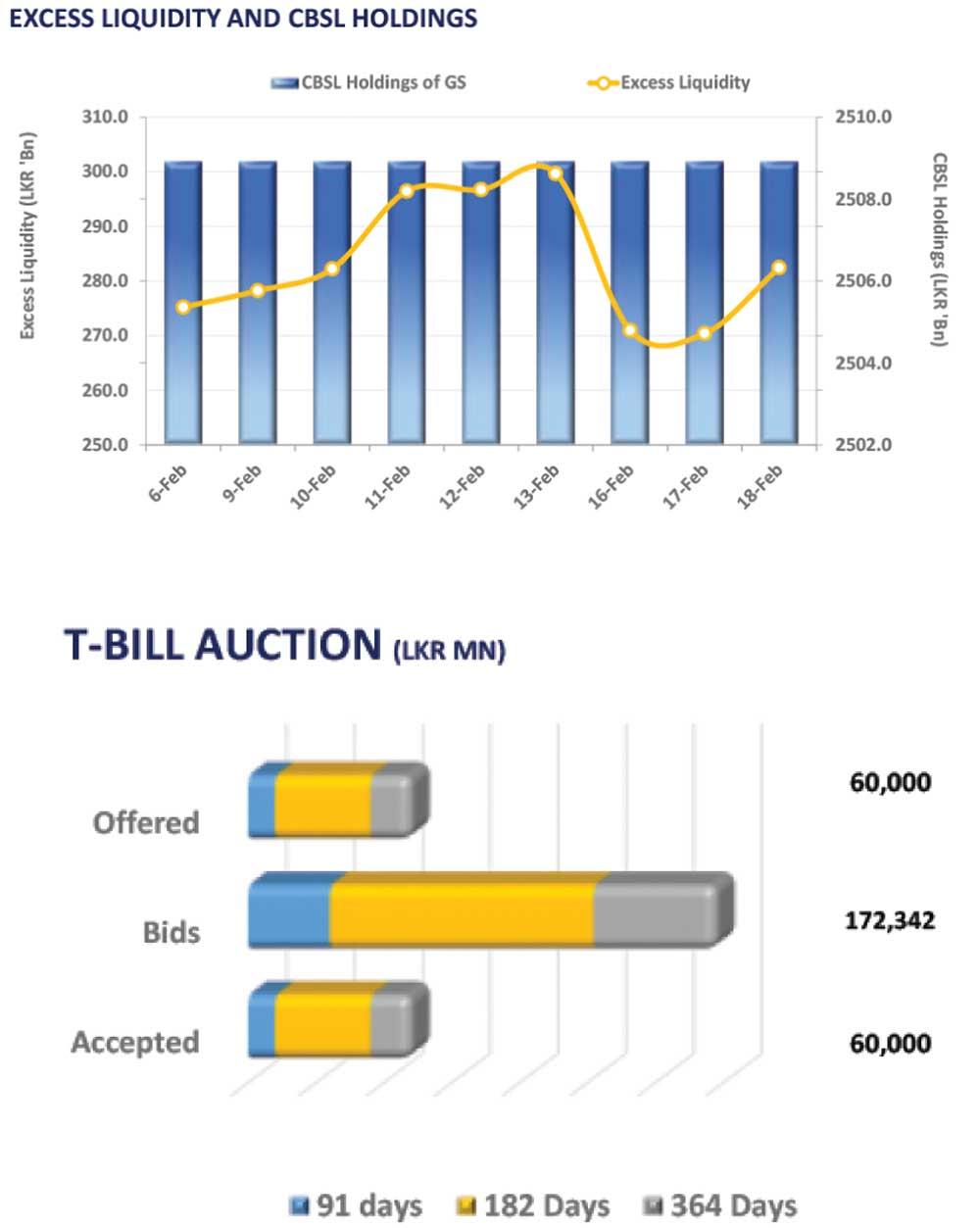

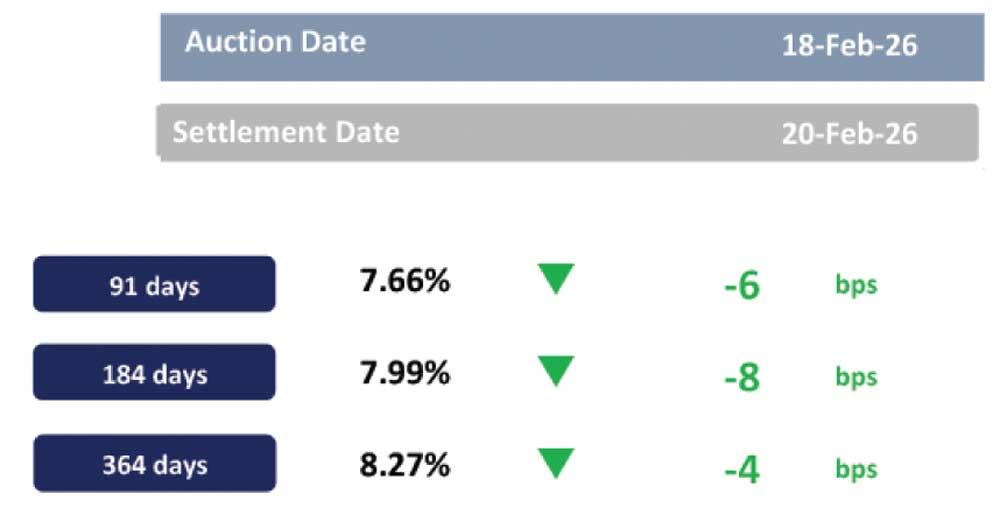

The public debt management office concluded its weekly T-bill auction, where Rs.60.0 billion was raised, accepting the fully offered amount.

The weighted average yields inched down across all tenures with that of the three-month bill inching down by 6bps to settle at 7.66 percent while that of the six-month and 12-month tenures dipped by 8bps and 4bps, settling at 7.99 percent and 8.27 percent, respectively.

On the external front, the Sri Lankan rupee slightly depreciated against the US dollar, closing at Rs.309.32/US dollar, compared to Rs.309.22/US dollar recorded the previous day.

Overnight liquidity in the banking system expanded to Rs.282.43 billion, from Rs.270.41 billion recorded previously.