Reply To:

Name - Reply Comment

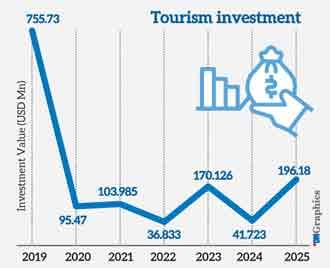

Sri Lanka’s tourism sector recorded a massive resurgence in investor confidence in 2025, with realised investments reaching their highest level since 2019.

Sri Lanka’s tourism sector recorded a massive resurgence in investor confidence in 2025, with realised investments reaching their highest level since 2019.

Driven by a record-breaking influx of tourists, the sector saw approved investment projects surge to USD 196.18 million, representing a nearly fourfold increase from the US$ 41.72 million recorded in the previous year. A deeper analysis of the investment data reveals a robust pipeline of future developments. The Sri Lanka Tourism Development Authority (SLTDA) received 126 investment project proposals in 2025, encompassing 3,413 rooms with a total proposed investment value of US$ 339.28 million. From this pipeline, 42 projects consisting of 1,205 rooms were officially approved and realised during the year, highlighting a strong conversion rate and renewed capital deployment in the hospitality space.

The regional distribution of these investments paints a fascinating picture of shifting investor focus, albeit with stark disparities. The Badulla district emerged as the undisputed top destination for fresh capital, attracting a massive US$ 70.6 million across 13 projects. This influx points to large-scale developments capitalising on the booming backpacker and boutique tourism corridor spanning Ella and Bandarawela.

Other significant capital magnets included Ampara with US$ 36.31 million, Galle with US$ 35.14 million, and the Gampaha and Kalutara districts securing roughly US$ 25 million each. Interestingly, while the Matara district attracted the highest volume of individual projects at 29, the total investment value stood at a moderate US$ 24.72 million, indicating a vibrant ecosystem of smaller-scale, localised enterprises. In stark contrast, five districts, including Mannar, Mullaitivu, Vavuniya, Kilinochchi, and Polonnaruwa, recorded absolutely zero new tourism investment projects in 2025, exposing a critical lack of development in the Northern and historical regions.

This wave of investment coincided with a substantial expansion in the country’s accommodation infrastructure. The total number of registered tourism establishments grew by approximately 12 per cent, rising from 4,390 in 2024 to 4,927 in 2025. Consequently, the national room inventory expanded by 6,200 rooms, pushing the total capacity from 53,378 to 59,578 rooms. The classified tourist hotel segment saw moderate but steady growth, adding 1,500 rooms to reach a total of 18,308. The most aggressive expansion within this premium tier was witnessed in the five-star category, which ballooned from 6,283 to 7,733 rooms, a trend likely driven by existing properties upgrading their classifications. Meanwhile, the one-star and two-star categories experienced slight contractions in both establishments and room counts.

The alternative and unclassified accommodation segments demonstrated even more dynamic growth, proving essential to absorbing the record tourist numbers. Guest houses across the island added over 3,000 rooms, expanding their capacity from 18,445 to 21,463 rooms.

The bungalow category also recorded a sharp increase, adding over 1,000 rooms to reach a total of 5,432, signalling a surging demand for private, nature-oriented family accommodations. Homestay units similarly reflected the continued strength of community-based tourism, growing to 3,416 rooms.

Despite the overall capacity growth, the geographic distribution of Sri Lanka’s room stock remains heavily skewed toward the traditional coastal belts. The Western Province, functioning as the primary business and transit hub, commands the lion’s share with 20,433 rooms, representing 34.3 per cent of the national total. The Southern Province follows closely with 15,722 rooms, holding a 26.4 per cent share driven almost entirely by the sun-and-sand leisure market. Together, these two coastal regions control over 60 per cent of the country’s formal accommodation infrastructure.

The Central Province acts as the vital third pillar with 9,917 rooms, supporting the cultural and hill country circuits.

However, vast stretches of the country remain acutely underdeveloped, with the entire Northern Province holding just 1,169 rooms and the Sabaragamuwa Province offering a mere 1,528 rooms, leaving significant untapped potential for future geographic diversification and investment. (NF)