Reply To:

Name - Reply Comment

|

Krishan Balendra |

Premier blue-chip John Keells Holdings PLC (JKH) reported a strong fourth quarter (4Q) performance for the financial year ended 31 March 2025, driven by a rebound in consumer demand and the first earnings contributions from new investments, including the West Container Terminal (WCT-1).

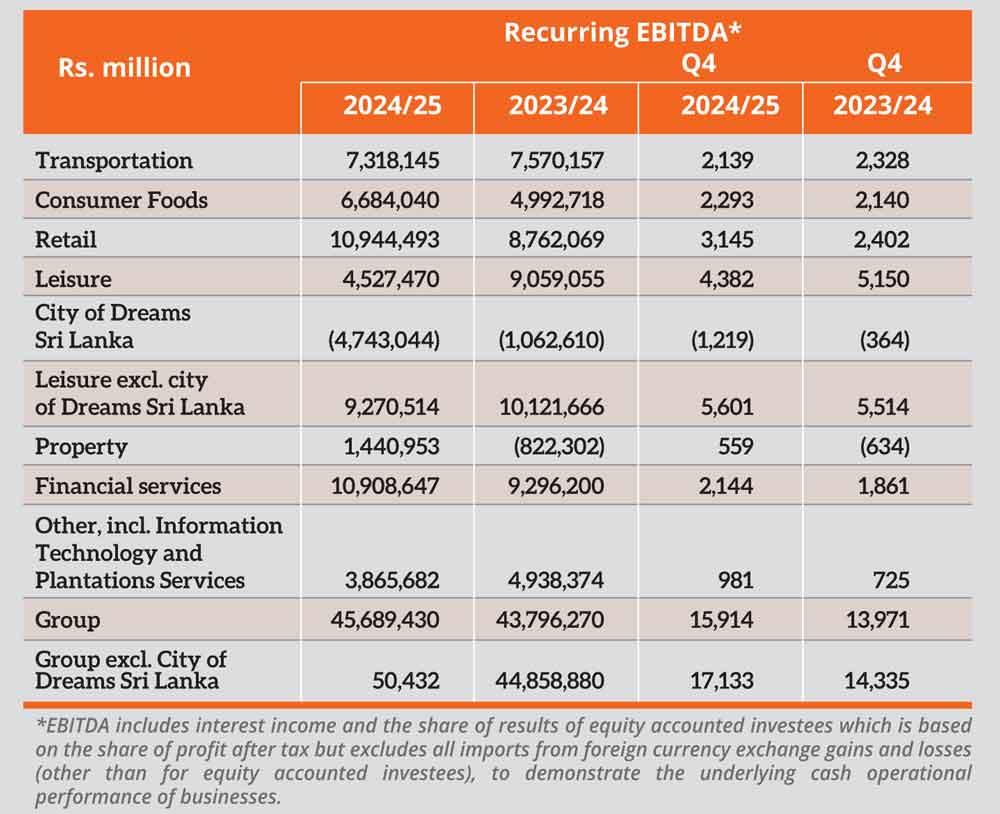

Group profit before tax (PBT), excluding the City of Dreams Sri Lanka (CODSL) project, soared 71 percent year-on-year (YoY) to Rs.10.85 billion in 4Q. Earnings before interest, tax, depreciation, and amortisation (EBITDA) also rose significantly during the quarter, supported by its consumer, supermarket, and financial services businesses.

For the full FY2024/25, recurring Group EBITDA (excluding Cinnamon Life) rose 12 percent to Rs.50.43 billion, while recurring PBT (excluding CODSL) increased 60 percent to Rs.22.93 billion.

The quarter included Rs.1.14 billion depreciation charge and Rs.1.09 billion in interest expenses tied to Cinnamon Life, the Group’s luxury integrated resort that soft-opened in January.

“The Group’s financial performance remained in line with expectations, driven by the strength of our consumer-focused businesses which gained momentum quarter-after-quarter,” JKH Chairman Krishan Balendra said in a commentary that followed the release of the financial results.

“As anticipated, overall Group EBITDA was affected by the substantial pre-opening, ramp-up, and operating expenses at the City of Dreams Sri Lanka integrated resort,” he added.

Profitability surged on the back of double-digit volume growth in Beverages and Confectionery, pushed by seasonal demand and a broader uptick in consumer activity. Margins, however, came under pressure from higher excise duties, softer performance in impulse product lines, and increased promotional costs.

Same-store sales rose 16.2 percent year-on-year in 4Q, with footfall up 19.1 percent, which offset a 2.4 percent dip in average basket size. The performance underscores the continued recovery in retail consumer sentiment.

JKCG Auto launched its New Energy Vehicles (NEV) business with the BYD range, attracting stronger-than-expected demand. The Group expects a “material earnings contribution” from this segment in the upcoming quarter.

The Leisure industry was weighed down by pre-opening and ramp-up expenses from CODSL. Excluding Cinnamon Life, EBITDA remained steady at Rs.5.60 billion. Sri Lankan Resorts delivered improved profits with higher occupancy and room rates, while Colombo and Maldivian operations saw pressure from currency losses and one-off expenses.

Profitability improved on the back of continued apartment sales at Cinnamon Life and revenue from the VIMAN project. Rajawella Holdings also contributed gains from real estate sales in Digana.

However, 4Q results included a Rs.639 million asset write-off related to the demolition of the K-Zone Ja-Ela mall to make way for VIMAN residential development.

Transportation saw a dip in EBITDA, primarily due to a 17 percent decline in volumes at Lanka Marine Services (LMS). The strong base effect from last year’s Red Sea crisis–induced spike also weighed on comparisons. SAGT volumes improved but profitability was flat due to currency appreciation.

Nations Trust Bank delivered robust profit growth with improved lending volumes. Union Assurance reported double-digit growth in gross written premiums, helped by renewal and regular new business premiums.

Other sectors benefited from foreign exchange gains at the Holding Company. Despite an uptick in borrowings, PBT rose due to lower interest costs following the January 2025 conversion of convertible debentures issued to HWIC Asia Fund.