Reply To:

Name - Reply Comment

|

Ashish Chandra |

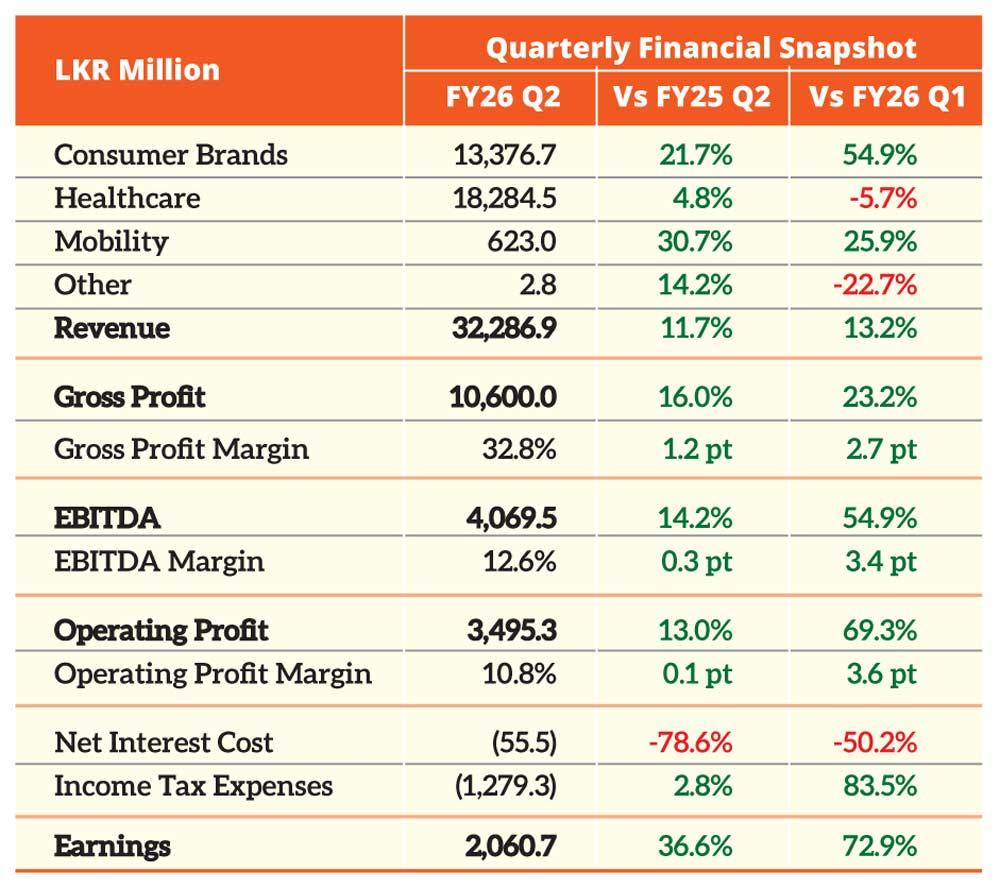

Hemas Holdings PLC delivered another quarter of resilient performance in the three months ended September 2025, posting a 36.6 percent year-on-year (YoY) surge in earnings to Rs.2.1 billion.

The performance was powered by revenue growth across all core business segments and disciplined cost management.

The group’s operating profit rose 13.0 percent to Rs.3.5 billion, while the net interest costs dropped sharply by 78.9 percent, reflecting lower borrowing levels and easing interest rates that helped strengthen the bottom line.

The second quarter also marked a period of strategic acceleration for the group, with two major investments underscoring Hemas’ long-term growth vision and diversification strategy. The company entered into a conditional agreement to acquire a leading consumer products firm in Kenya, marking its first move into East Africa in line with its international expansion roadmap. Simultaneously, Hemas Hospitals commenced the expansion of its Thalawathugoda facility, a step toward transforming into a tertiary care provider by introducing specialised services in cardiology, neurology and nephrology.

Investor confidence in the group’s trajectory has mirrored its operational strength. The Hemas share has appreciated 110.6 percent YoY, far outpacing the CSE All Share Index’s 83.6 percent and S&P SL20’s 77.1 percent gains during the same period.

For the first half of FY2026, Hemas’ revenue rose 11.8 percent to Rs.60.8 billion, while the operating profit climbed 10.7 percent to Rs.5.6 billion. The cumulative earnings reached Rs.3.3 billion, an increase of 32.5 percent YoY, signalling the sustained momentum despite a still-fragile macroeconomic recovery.

The group’s strong showing came against a backdrop of improving domestic economic conditions. The rupee remained broadly stable, Average Weighted Prime Lending Rate eased to 8.05 percent and headline inflation turned positive, reflecting a mild uptick in demand after a year of contraction. Sri Lanka’s debt restructuring efforts, progress on the International Monetary Fund programme and the sovereign credit rating upgrade to ‘CCC+/C’ collectively strengthened the macro stability, conditions that Hemas appears to have leveraged effectively.

Across its business verticals, the consumer brands sector continued to be the group’s growth engine. Revenue for the quarter climbed 21.7 percent to Rs.13.4 billion, while the operating profit rose to Rs.2.1 billion and earnings to Rs.1.6 billion. The uptick was driven by higher sales volumes in the beauty and personal care categories, supported by intensified marketing and brand-building efforts.

New product innovation, including a charcoal-infused toothbrush under the Clogard brand, strengthened its domestic portfolio, while the Bangladesh business recorded revenue growth, despite the inflationary and political headwinds, buoyed by a favourable sales mix in the value-added hair oil category.

For the first half, the sector’s cumulative earnings grew 25.7 percent to Rs.2.3 billion, with revenue up 10.9 percent to Rs.22.0 billion and the operating profit increasing 15.1 percent to Rs.2.9 billion.

Hemas’ learning arm Atlas maintained its leadership position in the stationery market, posting notable volume-led growth and diversifying into lifestyle products with the ‘Active Fit’ school bag range. Its push into the digital learning space through strategic partnerships underscored its commitment to innovation in education.

The healthcare sector reported a 12.2 percent rise in cumulative revenue to Rs.37.7 billion and a 15.3 percent increase in earnings to Rs.2.1 billion, with growth seen across pharmaceuticals and hospitals. Morison’s new product launches, including ChlorMor for paediatric respiratory care and CeeMor Vitamin C Tablets, expanded its wellness portfolio, while Hemas Hospitals benefited from higher admissions, channel consultations and growing demand for outpatient services. The SLIIT-Hemas Allied Health Institute further broadened its course offerings, adding biomedical sciences to meet the demand for skilled healthcare professionals.

The mobility sector too maintained steady growth, with revenue up 18.7 percent to Rs.1.12 billion and earnings at Rs.396.3 million. Maritime operations were buoyed by higher volumes, following the launch of the China-India Express service, while the aviation segment benefited from the increased passenger and cargo traffic, despite the global trade uncertainties and tariff-related challenges.

Looking ahead, Hemas said it expects to complete the Kenyan acquisition by end-FY2026, subject to the regulatory approvals, positioning the group to unlock new regional growth opportunities. At the same time, it is conducting a strategic review of its Long Range Plan to align with the evolving market dynamics and focus on cost optimisation, operational excellence and innovation-led value creation.

Group CEO Ashish Chandra said Hemas remains focused on “driving operational excellence, enhancing resilience and exploring investment opportunities in related and adjacent spaces to deliver long-term shareholder value”.