Reply To:

Name - Reply Comment

By Rauff Reffai

Attracting FDI, a key enabler of export performance, has been a challenge for Sri Lanka. As exports and FDI are a platform for productivity growth, Sri Lanka has missed out on new technologies and know-how typically associated with FDI.

Prof. Razeen Sally (a Sri Lankan Resident Singaporean at NUS) in an interview to Daily Mirror In June this year set the alarm bells when he observed:

(1)If the pace of growth is not sustained (i.e. 5 percent GDP) the economy will slide into recession and default (mercifully that had not happened) or in the alternative

(2)The economy needs to sustain a growth path beyond the IMF programme, and make FDI Flows possible by integrating into the Global Value Chains (GVC).

Garments have not made us rich , nor has Sri Lanka succeeded in climbing the manufacturing Ladder. The work Force is still stuck in semi skilled and unskilled labour. Low end manufacturing and Inefficient Agriculture .Then the next hurdle to clear is to create a work force that supports a Niche base of Critical Industries, the Think Tank Centre for Poverty Analysis Identifies in its latest Report (CEPA 2024) that : Tourism, Agriculture (Value added) ,Manufacturing and ICT as these Niche Sectors.

Our ambitious target for Merchandise Exports for Sri Lanka is projected to be US$ 25.0 billion by 2030, while we are presently confined to US$3.0 to 5.0 million on average (US Trade Stats 2025). The size of the FDI pie is US$ 860.0 billion (2023) of which US$ 31.0 billion have flown (2024) into structurally weak economies, including small developing island countries (UNCTAD 2024).

What is shocking is that we have registered a steady slide in the very measures which Investors find it attractive for drawing in FDI into the targeted sectors/sub sectors.

Our Governance effectiveness Index according to World Bank had slid from 112 (2010) to 127 (2023) while India (70) and Vietnam (95) are well ahead of us. In terms of corruption perception Index our rankings have slid from 91 (2010) to 121 (in 2024).

The above is a revelation of what is retarding our efforts to draw FDI , when in actual fact 2.4 percent of the global flows (US$ 31.0 billion) are still available to tap into Then why not ?

Most readers would realize that our Central pillar (FIG 1) a Coherent Institutional Framework is not at its strongest. While the BOI is talking of investment accruals ( US$ 507 million) in first half of 2025, US Investment sources attribute a mere 10 % of that as inward flows (in real time). While the BOI is talking of the Investor Facilitation Centre (IFC) The Global Investor Competiveness Report decries the lack of a National Single Window (NSW) approval system . These are contradictory signals. Reeks of lack of coherence. It’s also a persistent query why we don’t share a National Development plan, which constantly evades the public gaze.

Unfortunately for the country the story which prospective investors tell is not aligned with a strong service delivery either , be it the Sri Lanka Customs or the Environment service or for that matter the much hyped Sri Lanka Tourism Development Authority (SLTDA ) which recently emptied its drawers on a listing of 14 eamarked land for tourism development on 30 year lease . Which EOI closed even before the SLTDA promotion campaign had started.

The Port City Project (once boasted as the biggest effort to integrate ourselves to the Global Value Chains has so far only 130 Companies and 70 fresh entrants to boast (over a ten year period) while their biggest investment is US$ 5.0 million inflow. We appear to pull the wool over own eyes in this valiant effort to show off attracting FDI.

However not all is lost. Sri Lanka has an opportunity to capitalize on shifts in GVCs precipitated by ongoing geopolitical shifts, supply chain disruptions, and geopolitical instability(due to the Trump Tariffs) . Global trade is rebounding, with a projected 2.6 percent growth in 2024 and expected growth of 3.3 percent in 2025.

To make the most of these new opportunities, however, our trade policy should: (i) reduce and sustain low tariffs to incentivize exports, thereby reducing input costs for exporters; (ii) implement a NSW to reduce the time and costs of engaging in international trade; (iii) adopt a modern FDI regime focused on attracting export-oriented investments (JVs in particular) and (iv) establish complementary labor market policies such as STEM skills upgrades, and (v) address governance challenges (Example Governance effectiveness and stopping the Internal bleeding through loss making SOEs) facing our economy.

REALITY CHECKS

The purpose of this follow up feature is basically to address (iii) and (iv) above.

Enhancing competitiveness is critical to return to a sustainable growth path. Further implementation of SOE reforms is needed to address the fiscal, financial stability and governance-related risks posed by SOEs, as well as to improve the country’s competitiveness of its Exports. This includes measures to restructure the balance sheets of selected key SOEs (CPC, CEB and the National Airline) and explore opportunities to increase private participation in SOEs engaged in commercial activities. Measures to develop the financial sector and strengthen the digital economy will help enhance productivity and competitiveness, and improve service delivery.

. Years of low export growth and limited diversification, due to inward-oriented policies, have also contributed to this. The declining growth rate of the working age population has lowered employment growth, and with depleted national savings and ongoing fiscal consolidation had limited public investment, nor had it improved private investment . Certainly export and productivity growth are critical. Higher FDI inflows if garnered can help revive private investment and diversify and expand exports.

Lack of openness limits vulnerabilities but on the other hand it limits the country’s ’ ability to take advantage of the reshaping of GVCs that is underway.

Further, since 2016, India, Pakistan, Sri Lanka, and Bhutan have widened the geopolitical spectrum of their export markets and FDI sources. With above-average export concentration towards the US and Europe, and above-average concentration of FDI from China, Sri Lanka shares characteristics of ‘connector countries’ that are able to navigate and benefit from relationships across different geopolitical blocs.

Removing obstacles to trade and foreign investment, improving infrastructure and logistics, and increasing institutional effectiveness can help Sri Lanka integrate further into the desired global supply chains.

Growth of Industrial exports have been slow and had diversified little. On average, during 2010–2023, slow growth in industrial exports accounted for the weak performance of exports overall, as it comprised three quarters of goods exports. Apparel– the most successful manufactured export – grew at only 3.7 percent a year during 2010–2023, and lost world market share in 2010–2019.

Further, the share of sophisticated manufactured products in the export basket remained low, as indicated by Sri Lanka’s ranking of around 80 (in recent years) among 133 countries based on the Economic Complexity Index. (Sri Lanka Development Update World Bank 2024).

Sophisticated goods on the manufacturing ladder permits upgrade vertically within a sub-sector (e.g., machinery versus clothing) and generate more inter-industry spillovers and faster export and productivity growth.

The growth and diversification of Sri Lanka’s exports, particularly in manufactured goods, is restricted by protection. High import tariffs made import substitutes relatively more profitable than exports, creating an anti-export bias. Protection was mostly driven by the imposition of para-tariffs on top of the existing custom duties. The manufacturing sector was the most protected, (170 of these) did not represent strategic developments or scope for high employment.

While holding back these ST oriented protectionist para tariffs, we need to pursue trade agreements most beneficial to Sri Lanka. Building negotiating capacity in these free trade agreements too needs to be prioritized.

Support businesses in the use of preferences in existing FTAs (e.g. Thailand) and restart FTA negotiations via a properly resourced Sri Lanka Trade Representative Office. Undertake a feasibility study for a Sri Lanka trade representative office and implement capacity-building programmes on FTA negotiations.

Address supply side constraints to enhance work force skills (eg STEM) , build Export Zones access , improve agricultural productivity besides transitioning land limitations obstructing realization of the economies of scale (particularly in Coconut cultivation ). See Accelerating Growth below for more details.

TARGETED SECTORS /SUB SECTORS

Manufacturing , is pivotal in accelerating growth to higher levels in the medium term and sustaining it over the long term, ultimately transitioning the country to a high-income status.

integration within the global economy, enables industries to expand and capitalise on economies of scale. while attracting FDI, targeting international markets and global supply chains. FDI brings not just capital but also technology, management expertise, professionalism and access to input and output markets – fostering spillover benefits for the host country.

Essentially they are of two types:

(1) Global Production Networks Producer Driven (PD)

(2) Global Production Networks which are Buyer Driven (BD)

.High end Apparel /designer wear /value added garments, food processing (yet BD) and niche manufacturing such as auto parts, boat-building and electronic components (PD) The PD category needing large labour deployment / vis-a-vis if less automated accommodates transition of excess labour from domestic agriculture .It can also enhance innovation and productivity growth in the agriculture sector itself.

It bolsters the service sector growth too, generating value additions during the manufacturing process and preventing the ‘non-tradable bias’ in economic growth.

To support manufacturing effectively, the following (if absent) , will become a barrier:

(1)Simple and rational regulations, Single Window (NSW) arrangements in institutions and procedures.

(2)Ensure the availability, affordability and quality of manufacturing inputs – both primary and secondary – to maintain an uninterrupted industrialization process and international competitiveness of industries.

(3)Reform cross-border policies and regulations while adopting digitalised processes and a ‘single window’ system to streamline trade and investment flows.

(4)Align industrialisation with 21st century requirements by embracing sustainability standards such ESG into EU markets for example(effective from 2023).

It would be a good FDI bench mark if Sri Lanka could use Vietnam as a comparator (but on a lower scale)

VIETNAM MANUFACTURING INDUSTRY

Vietnam’s manufacturing market is shaped by its strong export orientation and sectoral specialization. Domestic enterprises hold competitive positions in industries such as steel, chemicals, agribusiness, and consumer goods, while high-tech segments, including electronics, mobile phones, textiles, footwear, and machinery, are primarily driven by large-scale production for export. (mostly PD Global Production Networks).

FDI-DRIVEN GROWTH

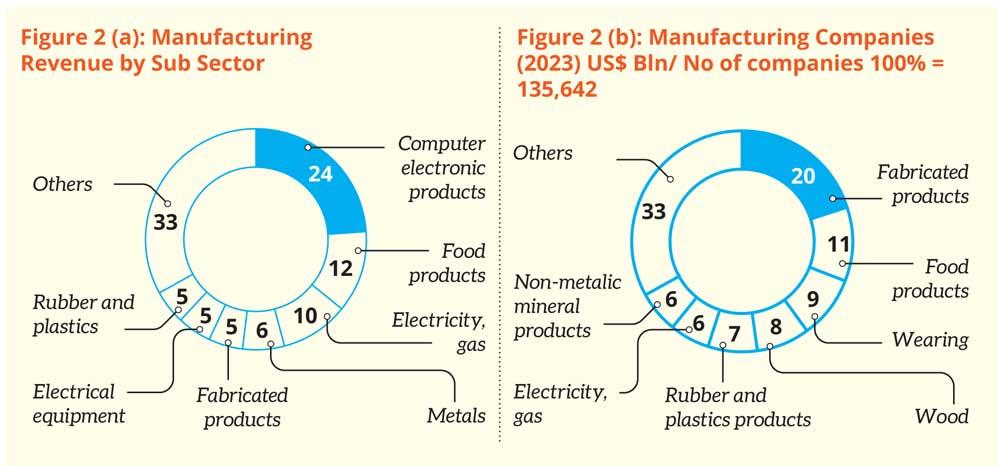

Vietnam’s manufacturing industry is strongly fueled by foreign investment. From 2015 to 2024, annual registered FDI into processing and manufacturing ranged between US$ 7–10 billion, before surging to over US$ 20 billion in both 2023 and 2024. In 2024, manufacturing accounted for the largest share of disbursed FDI at about US$ 20.6 billion. The momentum has carried into 2025, with the first seven months attracting US$ 24.1 billion in registered FDI, of which 61 percent (US$ 12.1 billion) went to manufacturing.

It can be seen (FIG 3) that even in a relatively volatile period (2023 and 2024) while GVCs were shifting, Vietnam attracted its highest ever Capital inflows (in US$ billions).

These inflows were into projects including new electronics plants, renewable energy equipment factories, and automotive assembly facilities. Major investors continue to come from South Korea, Singapore, China, Japan, and Taiwan, reflecting both high-tech expansion and regional supply chain shifts.

Investors are drawn by Vietnam’s competitive wages, stable investment policies, and extensive trade agreements, which make it an attractive alternative production base. This shift has reinforced Vietnam’s position in global supply chains,

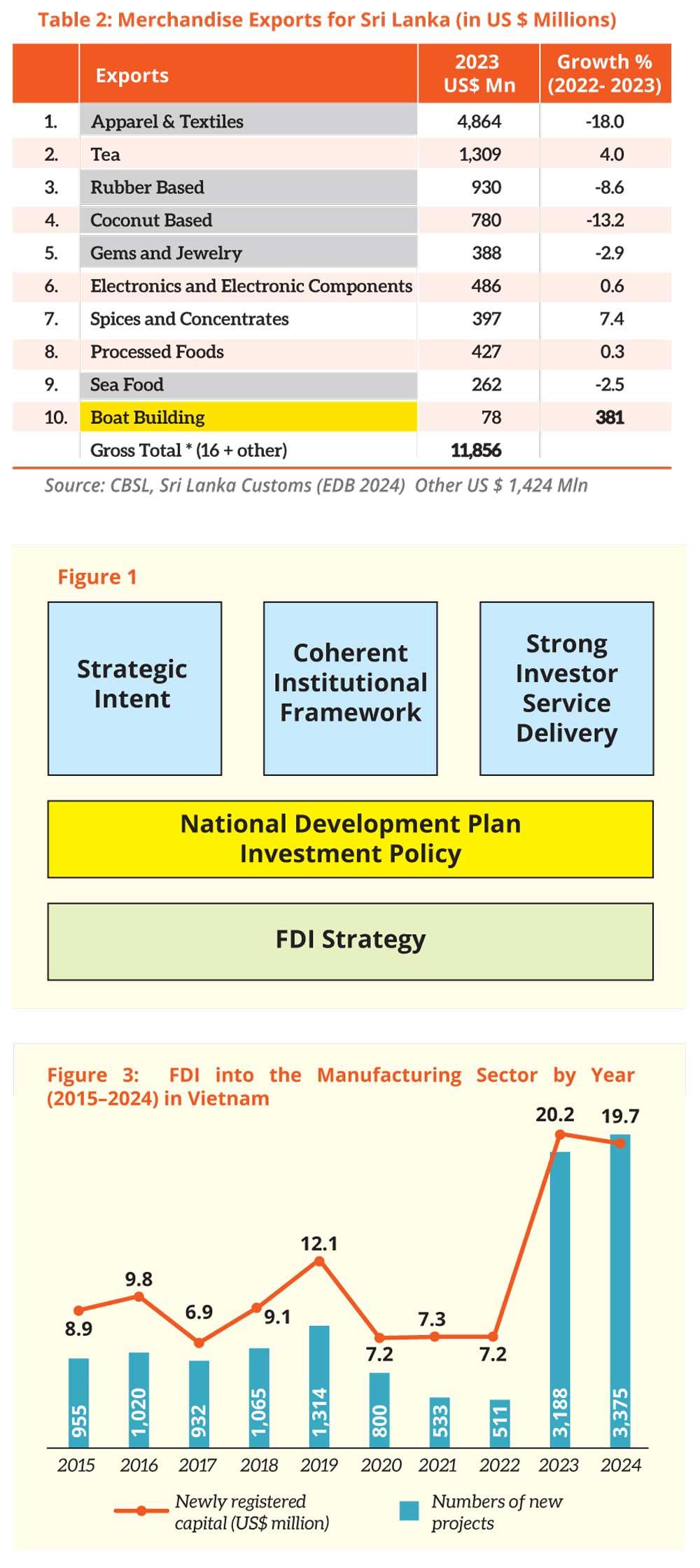

When we examine the latest Merchandise Exports for Sri Lanka, we see significant decline in some of our key Exports (Table 2).

Though we averaged US$ 1.0 billion ( every month during the above period , we see significant drops in Apparel, Rubber and Coconut based products. Though valiantly shouted out, our Gems and Jewellery too dropped by 3 percent. Boat Building shows some promise with a 300 percent increase over the previous year. Our FDI inflows (according to BOI) still trail US$ 500.0 million to the US$ 20.0 billion for Vietnam in 2023.

RATE OF CLIMB ON THE MANUFACTURING LADDER

Vietnam’s manufacturing spans several key industries, from high-tech electronics to traditional labor-intensive sectors. Electronics, phones, and machinery together account for40 percent of Vietnam’s total export turnover, driven largely by multinational firms like Samsung, LG, and Intel. Meanwhile, textiles, garments, and footwear remain strong traditional pillars, supported by skilled labor and extensive trade agreements.

Emerging segments such as semiconductor, transport equipment, and high-value wood products also show steady growth, reflecting the country’s ongoing shift toward a more diversified industrial base. Notably, semiconductor assembly and testing have begun to attract significant foreign investment, positioning Vietnam as a potential hub in the global semiconductor supply chain.

In 2024, manufacturing exports dominated Vietnam’s trade performance, reaching US$ 356.74 billion and accounting for 88 percent of the country’s total exports. (While ours roughly remains at 65 percent of total exports at US$ 11.8 billion in 2023).

Within this, Vietnam registered electronics, computers, and components which led the sector with US$ 72.6 billion, representing over 20 percent of all manufacturing exports. This underscores the dual importance of manufacturing as the backbone of an export economy and electronics as its single largest and most competitive driver. That’s producer- driven where as our ratio (37 percent total exports of Apparel) is buyer-driven.

SHIFT IN WORKFORCE SKILLS

Human Capital re skilling can make a difference while attracting FDI towards higher end manufacturing Industries.

If (and should ) Producer driven GPNs demand skills complementary to semiconductor assembly and testing , then Sri Lanka too should introduce school based / TVT based preparedness to become part of the global semiconductor supply chain.

Then it will be a combined state and private sector response to investment in mid career reskilling and upskilling of labour along with fair wage and merit-based management practices. These behaviour by firms can signal to workers who are exploring both short-cycle and fundamental training that their efforts will not be wasted,

A revival in the development of human capital and the functioning of labour markets within the economy requires focused efforts to renew training systems for various age and experience cohorts, with an emphasis on the skills needed for emerging jobs. This update is urgently needed in secondary education to ensure that future generations of young people enter the labour market with job-ready skills.

Since the Government is currently incorporating these changes it’s a good signal for investors. However, talent shortages will remain until there is substantial escalation in mid-career re skilling and upskilling programmes as many of the individuals who need further reskilling and upskilling are beyond school age

investment in the skills needed for the jobs and “markets of tomorrow” viz reskilling, upskilling and education curricula updates are central to prepare workers and to achieve inclusive prosperity.

There is urgent need to upgrade education systems to provide digital skills and critical thinking skills through schools and universities . Supplemented by ongoing learning and skilling through public and private (life-long) learning programmes.

The Netherlands, Denmark, Switzerland and Finland are among the better-prepared countries in this respect. Any of these countries can be approached by Sri Lankan planners to assimilate their experience into our own curriculum upgrades. (without re inventing the wheel ).

ACCELERATING GROWTH

From the above, it can be concluded that the following five (5) success factors are critical for accelerating FDI growth:

Support from the higher levels of Government (President/Prime Minister) championing them would positively influence inward investments.

Strong Strategic alignment after consultation with public and private stakeholders cascading them into a well formulated National Development Plan, favors FDI decisions.

A High degree of Institutional and Financial Autonomy with flexib8ility to act according to the strategic plans, is certainly seen as a positively buy investors. Particularly form countries like Japan (who weigh planning before committing resources). Inducting Key staff of the promotion agency (BOI) from Private Sector with corporate experience would enhance investor experience.

A strong investor centric service orientation to design and provide relevant high quality services to investors through their investment cycle too, favors positive decisions. In view of this the Investor Facilitation Centre (IFC) /NSW must be located independent of the BOI.

While in this budgetary year, its timely to remind that sufficient and sustained financial resources over 3- 5 years be allocated , to ensure continuity of strategic efforts over the long haul. Such efforts are not abandoned pre maturely.

HOW HAVE WE DONE SO FAR?

FDI serves as a crucial mechanism to boost investment, do bring with them new technologies and production processes that enhance productivity, generate positive spillover effects by improving skills and management practices. They improve access to global production networks and GVCs . Sri Lanka’s FDI as a share of GDP on average amounted to 1.1 percent over the 2011–21 period, which is lower than the average (4.8 percent) among comparator countries . Only 36 percent of greenfield FDI announcements classified as export-oriented efficiency-seeking FDI.

Sri Lanka’s FDI inflows are also predominantly comprised of intra-company loans, representing short-term capital. Only about 10 percent of FDI inflows in the past decade constituted new investments (ADB 2012- 2022)

WHAT MUST BE DONE NOW

The first transition is particularly relevant to Sri Lanka today. It involves gradually increasing private domestic and foreign investment (especially in strategic industries), and the infusion (or diffusion) of technological and operational expertise from abroad into local production.

Human capital upskilling through vocational training and promoting science-tech-engineering-medicine (STEM) fields in secondary education, will create a pool of specialized workers connected to global knowledge flows. Increased competition, driven by openness and appropriate regulation, will boost local firms’ productivity as well. Both established firms, which can scale and enhance capabilities, and new entrants, which drive innovation and equitable growth, are essential for this transition.

The transformation is, as pointed out, on the long haul. There is no certainty that our Target of Merchandise exports of US$ 25.0 billion will be achieved five years from now.

(The writer is a retired Senior Consultant of the IDA, World Bank. An institutional Specialist by practice, with over twenty years in consulting and an equal number of years in Private Sector in senior management positions. He is a double Masters holder : MBA (USJ), M.Sc (Lon). He can be reached at [email protected])