Reply To:

Name - Reply Comment

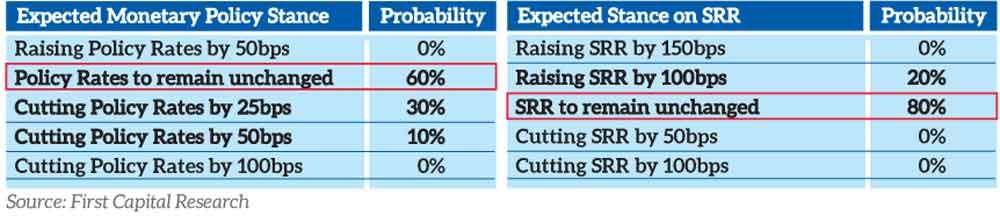

The Central Bank is expected to maintain its key policy rates at today’s final monetary policy review of 2025, as a strong private credit growth and a fragile external position outweigh the arguments for further easing.

A pre-policy note published yesterday by First Capital Research (FCR) indicated a 60 percent probability of rates staying unchanged, while assigning a 40 percent probability for a rate cut, 25 basis points most likely, with a smaller chance of a 50-basis-point reduction.

The Statutory Reserve Ratio is also expected to remain steady, although analysts see a small possibility of a 100-basis-point hike amid the improving liquidity.

Private sector lending has surged, following the February 2025 relaxation of the vehicle import ban, with September alone recording a record Rs.236.3 billion in new loans. The cumulative credit expansion from January to September exceeded Rs.9.5 trillion, while the Central Bank’s Willingness to Lend Index continued to improve into the third quarter.

This momentum, combined with the rising domestic demand and the ongoing recovery in construction, reduces the case for a rate cut, which could overheat credit growth and widen the current account deficit.

Sri Lanka’s foreign reserves, while marginally supported by tourism inflows and expected International Monetary Policy-Extended Fund Facility disbursements, remain tight at US $ 6.21 billion in October, covering roughly three months of imports. The near-term outflows are projected at US $ 2.04 billion over the next three months, largely due to the currency swap settlements. Against this backdrop, further monetary easing could exacerbate exchange rate pressures, increase import costs and complicate external debt servicing.

The Average Weighted Call Money Rate, the Central Bank’s operational target, has remained slightly above the policy rate amid the tightening liquidity. The banking system liquidity dropped to Rs.87.6 billion in mid-November, constraining the transmission of monetary easing. Analysts said a rate cut at this stage is unlikely to significantly influence the interbank rates.

Despite the strong credit expansion, some indicators suggest the economy may require support. GDP grew 4.8 percent in the first half of 2025 but the momentum is expected to ease, due to the subdued government capital expenditure and slowing household consumption. Inflation turned positive in August, rising 1.2 percent year-on-year and remained below the Central Bank’s 5 percent target, signalling some room for policy stimulus.

The small and medium enterprises (SMEs), which contribute over half of Sri Lanka’s GDP, continue to face high borrowing costs, with the average weighted SME rate at 10.5 percent, above the overall weighted prime rate of 8.4 percent. Analysts said a rate reduction could improve credit access for the SMEs and support domestic demand.

The global headwinds, including the emerging stagflation risks in the United States and slowing international growth, have prompted major central banks to ease policy in recent months. Fitch Ratings forecasts global growth at 2.4 percent for 2025, the slowest pace outside crisis years since 2008. Analysts said the Central Bank may consider aligning with the global easing cycles if the domestic conditions deteriorate.

The government’s proposal to remove the 2.5 percent Social Security Contribution Levy on financial services, effective January 2026 pending parliamentary approval, is expected to lower the borrowing costs and support economic activity. FCR analysts said the Central Bank may adopt a “wait-and-see” approach, avoiding immediate rate changes if the levy is abolished.

At its September 2025 review, the Central Bank maintained the Overnight Policy Rate at 7.75 percent, citing stable inflation trends, robust private sector credit expansion and resilient external inflows.

Analysts noted that these factors, alongside the improved sovereign credit ratings and easing global financial conditions, underpinned the bank’s cautious stance.