18 Sep 2025 - {{hitsCtrl.values.hits}}

In a 1996 speech to the Singapore Press Club, Lee Kuan Yew addressed the challenge of ensuring Singapore’s survival beyond his leadership and laid out the core principle of its success. He explained that Singapore prospered by “creating first-world conditions in a third-world region” and becoming “a base camp from which entrepreneurs forayed into the less developed areas around it”.

In a 1996 speech to the Singapore Press Club, Lee Kuan Yew addressed the challenge of ensuring Singapore’s survival beyond his leadership and laid out the core principle of its success. He explained that Singapore prospered by “creating first-world conditions in a third-world region” and becoming “a base camp from which entrepreneurs forayed into the less developed areas around it”.

It did this by offering speed, certainty and clean governance at a time when larger neighbours could not. The lesson for Sri Lanka is obvious. On scale, we are outmatched. A single Indian state surpasses our market size, while Vietnam’s labour force is seven times larger. While Vietnam operates around 400 export parks and is heading towards 500, we have just 15. We will never surpass our neighbours on land, labour, or market size; these are key investor attractions we lack. Therefore, Sri Lanka must compete differently.

Governance and the Cost of Doing Business Matter More for Small States

Sri Lanka must learn from other smaller economies that have excelled in exports and FDI. Nations like the Netherlands, Hong Kong, Switzerland, and Singapore consistently rank among the world’s top exporters despite their size. They win by delivering what larger administrations struggle to sustain: ruthless efficiency, reliable rules, and clean government.

Global rankings provide clear evidence of this, quantifying the very conditions that attract capital. High placings for small nations in the World Bank’s Doing Business report, for instance, signal an environment where contracts are enforced and bureaucracy is minimal. Strong scores on Transparency International’s Corruption Perception index, where countries like Denmark and Singapore top the rankings, are a direct measure of low corruption risk.

Similarly, consistent leadership in the World Intellectual Property Organisation (WIPO)’s Global Innovation Index, a position held by Switzerland for 14 years, points to a highly skilled workforce and world-class infrastructure. For investors, these are not abstract league tables; they are concrete indicators of predictability and operational ease. For small states lacking other advantages, performance on these metrics is a critical baseline. Miss it, and investors walk away.

Sri Lanka’s path to increasing exports and FDI

Sri Lanka is surrounded by countries that have more land, more labour and larger domestic markets. Therefore, to compete with them in exports and FDI, Sri Lanka needs to focus on its business environment: faster approvals and automation; reliability and consistency; clean governance; and world-class skills and infrastructure to optimise scarce resources. Sri Lanka’s ambitious target of generating $25 billion in merchandise exports by 2030, requires an annual export growth rate of 12%, which seems improbable without reform. Unless Sri Lanka reduces the cost of doing business, growth will remain subdued at the 1.4% annual average recorded between 2015 and 2024, and the country risks missing its export target yet again.

Such underperformance squanders the immense opportunity offered by the country’s geographic position. A world-class business environment would finally allow the country to act as a reliable hub for investors, using its proximity to major sea routes and the fast-growing Indian sub-continent, much as Singapore did in its region to achieve its own prosperity.

Sri Lanka: Falling Behind When It Should Be Leading

Paradoxically, in the efficiencies that should set us apart from bigger players, we continue to find ourselves falling behind our lager competitors. On the World Bank’s Government Effectiveness index, we have slipped from 112th in 2010 to 127th by 2023, behind India (70th) and Vietnam (95th). The Corruption Perceptions Index shows our ranking declined from 91st in 2010 to 121st in 2024. Meanwhile, on the Global Innovation Index, we stand at 89th, well behind China (11th), India (39th), and Vietnam (44th).

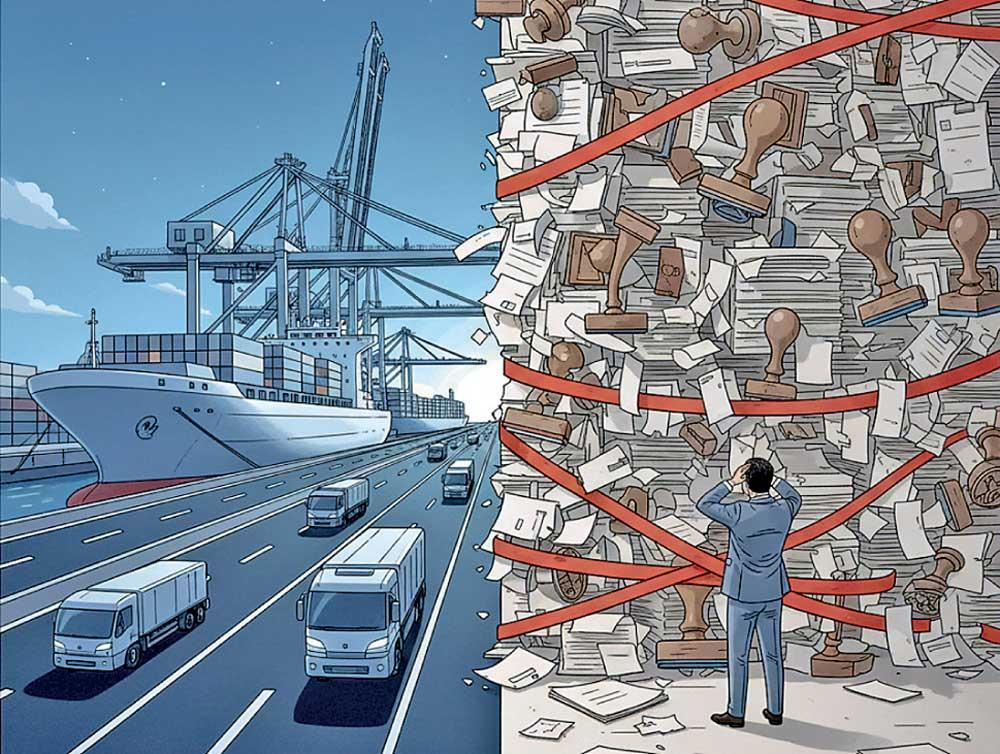

‘Trade single window’

The shortcomings in execution are most evident in the ‘Trade Single Window’, an online portal intended to reduce time and costs. Conceived nearly three decades ago, it remains unfinished. In contrast, our neighbours are moving swiftly: India, despite far greater coordination challenges, launched its single window in 2016; ASEAN has already interconnected national systems into a regional Single Window; and Bangladesh has mandated the end of all manual permits after January 2025.

While reluctant to finance this soft infrastructure, Sri Lanka has eagerly borrowed billions for highways and ports, assuming concrete and tax concessions would attract capital. This is a miscalculation. Multinationals will not invest if highways end at a customs shed where consignments queue for days, manual processes slow approvals, and rules change without notice. Ports are irrelevant if cargo gets stuck at the border. Tax holidays make no difference if the costs and delays of trade are high and predictability is low. International research is clear: investors consistently prioritise an efficient, predictable business environment over tax breaks, especially where fundamentals are weak.

We’re running out of time before investors walk away for good. Neighbours are sprinting ahead by digitising ports, curbing corruption, and enabling 24-hour clearances. Vietnam is developing eco-industrial parks, while India is advancing its public sector digitalisation programme.

Beyond Catching Up: Sri Lanka Must Leapfrog to Lead

The fix is not complicated: replace ribbon-cutting optics with regulatory reform. Enforce legal deadlines for approvals, treat digital infrastructure as capital, and publish a credible, funded timetable for trade facilitation initiatives like the single window. As Lee Kuan Yew said, Singapore had to be “better organised, and more efficient than others in the region.” If Sri Lanka is only as good as its neighbours, there is no reason for business to be based here. Its competitiveness will depend instead on whether it can build the systems that make its physical infrastructure deliver. If it fails to do so, the advantage of geography will count for little, and the opportunities before it will continue to slip away.

Mathisha Arangala is a Lead Economist at Verité Research’s International Economics Research Programme.

04 Jun 2026 3 hours ago

04 Jun 2026 3 hours ago

04 Jun 2026 4 hours ago

04 Jun 2026 4 hours ago

04 Jun 2026 4 hours ago