04 Jun 2025 - {{hitsCtrl.values.hits}}

Taxes are very important in building a robust economy and play a vital role in implementing good fiscal policies. Government policies on taxation that are governed by any country play a key role in determining a country’s vulnerability in providing health, education, etc., for its public. Any government in the world, whether it is developed or not, needs sufficient revenue to overcome financial difficulties.

Taxes are very important in building a robust economy and play a vital role in implementing good fiscal policies. Government policies on taxation that are governed by any country play a key role in determining a country’s vulnerability in providing health, education, etc., for its public. Any government in the world, whether it is developed or not, needs sufficient revenue to overcome financial difficulties.

Therefore, they change their tax policies and introduce a new way of tax collection using modern technologies. Narrowing the tax GAP and widening the tax base are the common Goals of the government when formulating tax policies for the public.

When considering the situation in Sri Lanka, two-thirds of revenue still comes from indirect taxes. Over time, the direct tax base has been eroded by high thresholds and multiple exemptions. Therefore, enhancing the Tax compliance strategy aiming at Taxpayer Registration is an essential factor for development.

Legal Provisions in progress

TIN registration – Taxpayer Registration and Taxpayer Identification Numbers

TIN registration – Taxpayer Registration and Taxpayer Identification Numbers

Tax registration, filing return, payment on time, declaration of Income, expenditure, assets and liabilities are key components of Tax compliance. The Inland Revenue Act No. 24 of 2017 outlines specific provisions for tax registration. Section 102 of this Act has also been mandated to individuals who are liable to tax must furnish a return of income. They must register with the Commissioner General within thirty days after the end of the basis provided for that year.

After fulfilling basic requirements, as per section 103 of IRD Act, the Commissioner General assigns a unique TIN (Taxpayer Identification Number) which is very unique to the Registered Taxpayers. The Inland Revenue Act also emphasises that the Minister, with the Commissioner General’s consent, to specify additional classes of persons who are obliged to register. The Extraordinary Gazette notification issued in May 2024 under No. 2334/21 has identified fourteen categories of professions to issue TIN registration with tax types. The same gazette notification under part B also identified two special categories to register as a class.

They are,

i. Who is at the age of 18 years or above as of December 31, 2023, or

ii. Who reaches the age of 18 years on or after January 01, 2024 and reaches the age of 18 years.

In the IRD Act No. 24 of 2017 taxpayer has been defined as follows.

“taxpayer” means— (a) a person who is required to pay tax under this Act, including a person who has zero chargeable or taxable income or a loss for a year of assessment;

or

(b) a person who is required to withhold tax and pay it to the Department;”

Taxpayer identification number

The Commissioner General assigns a unique TIN to every taxpayer, which shall be used in all correspondence relating to the administration of this Act.

Therefore, issuing a TIN registration for persons above 18 years old is a mandatory requirement in Sri Lanka.

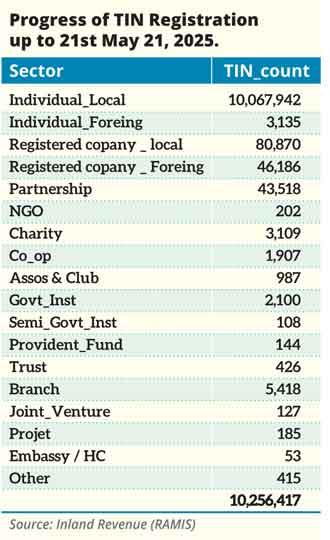

Progress of TIN Registration up to May 21, 2025.

Process of TIN Registration

In order to increase the Tax base in a country, it is required to expand facilities for registration when the registration process is a mode of simplification and easy access, anyone can enjoy the benefits of this.

Various types of registration in IRD and registration channels

Currently, IRD supports the registration process through various registration channels:

A. TIN could be obtained online via e-services portal of IRD (e-Services-->Access to e-Services -->Taxpayer Registration) TIN will be sent by email.

B. Offline application by visiting the Primary Registration Unit of the Inland Revenue Head Office located at Sir Chittampalam A. Gardiner Mawatha, Colombo 02 or from any Metropolitan or Regional Office.

C. Offline application by sending a filled application form along with supporting documents through post to the Commissioner General, Inland Revenue Department, Sir Chittampalam A Gardiner Mawatha, Colombo 02. The TIN certificate will be sent to the applicant through post.

D. Bulk registration option available with IRD officials for forced registration

Conclusion

Having a TIN certificate for a person does not imply that he/she must pay Income Tax. As per the recent amendments to the Inland Revenue Act. People who have a total income of more than 1.8 million annually or Rs. 150,000 monthly from an Income source are eligible to pay their taxes according to the law.

The effective operation of a tax system mainly depends on a comprehensive system of taxpayer registration and identification of taxpayer entity. This system will help not only in increasing compliance but also in exchanging information, including 3rd party reports. Therefore, levels of registration in a country is a mirror of a good tax system. When many registration and follow the obligation with a compliance mechanism, it is an important thing to minimise the tax burden faced by individuals of a country.

Registration is one of the major factors in any country for developing its tax base and collecting high revenue for that purpose, We need a good, sophisticated tax information system. Exchanging information, process and linking with agencies are also vital in the registration process. Increasing the automated tax process helps to reduce the scope for manual intervention in the process. This process leads to save time and unnecessary workloads in setting their registration. A favourable process of communication always leads to build a strong trust with citizens a strong trust always shows a multiple approach to a good tax system. When citizens understand their responsibility, they will help the government by paying taxes and a transparent mechanism is needed. Many countries in the world are now using digitalised cards to identify not only for tax purposes but also for every activity. This will bring many benefits to the country. Simplifying the process for taxpayer requirements is always helpful for both tax administration and taxpayers.

Source

Tax administration 2022

Comparative information on OECD

11 Jun 2026 13 minute ago

11 Jun 2026 30 minute ago

11 Jun 2026 55 minute ago

11 Jun 2026 1 hours ago

11 Jun 2026 1 hours ago