27 Feb 2026 - {{hitsCtrl.values.hits}}

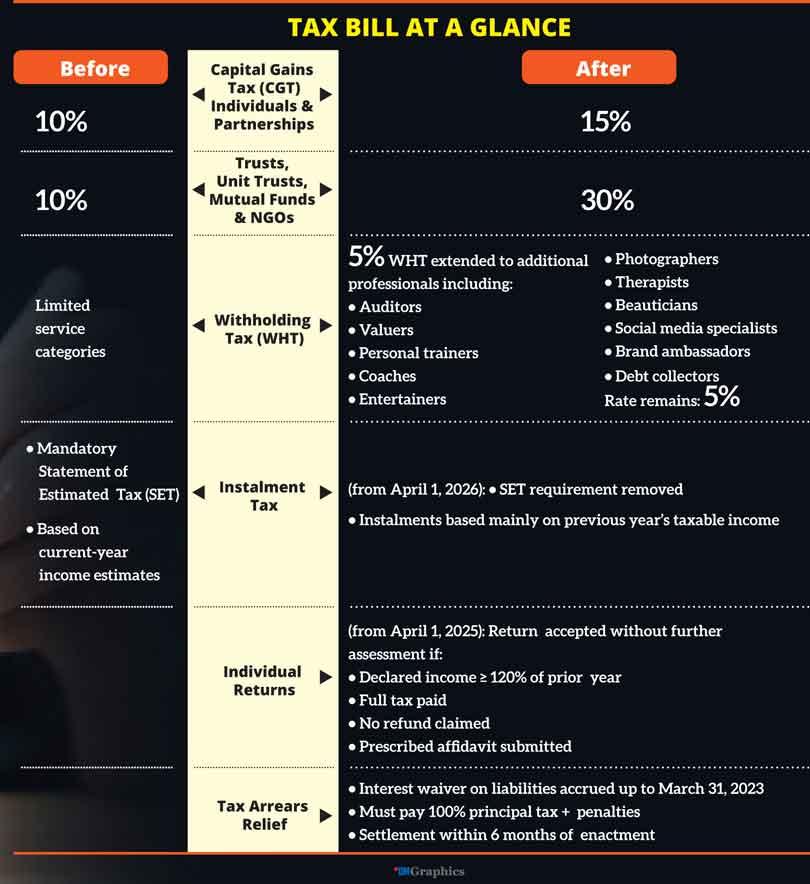

CGT rate for individuals, partnerships would rise to 15 per cent from the current 10 per cent

CGT rate for individuals, partnerships would rise to 15 per cent from the current 10 per cent

Changes will take effect only after Parliamentary approval

A Bill to amend the Inland Revenue Act No. 24 of 2017 was published in a Gazette Extraordinary on February 24

Is an increase in Capital Gains Tax (CGT), the tax paid on profits from selling assets such as land, buildings or shares

The Bill also includes a one-time concession for taxpayers with outstanding liabilities

The Bill also proposes to bring more service providers under the 5 per cent withholding tax system

BY Mirror Business desk

The Government has tabled sweeping changes to Sri Lanka’s tax framework, proposing higher taxes on capital gains, a wider net for withholding tax and a one-off relief window for those with unpaid dues.

A Bill to amend the Inland Revenue Act No. 24 of 2017 was published in a Gazette Extraordinary on February 24, by the Minister of Finance, Planning and Economic Development, Anura Kumara Dissanayake. The proposals will take effect only if Parliament passes the Bill and it is formally enacted.

One of the most significant proposals is an increase in Capital Gains Tax (CGT), the tax paid on profits from selling assets such as land, buildings or shares.

Under the draft law, the CGT rate for individuals and partnerships would rise to 15 per cent from the current 10 per cent. For trusts, unit trusts, mutual funds and non-governmental organisations, the rate would increase sharply to 30 per cent from 10 per cent.

In simple terms, if a person sells property or shares at a profit after the law is enacted, a larger portion of that gain would go to the tax authorities than before.

The Bill also includes a one-time concession for taxpayers with outstanding liabilities.

The Commissioner General of Inland Revenue would be allowed to waive interest that has built up on unpaid or late-paid taxes up to March 31, 2023, under the Inland Revenue Act, the Surcharge Tax Act and the Debt Repayment Levy. However, this relief is conditional. Taxpayers must settle the full original tax amount and any penalties within six months of the new law coming into force.

For businesses and individuals burdened by accumulated interest, this could reduce the total amount payable but only if they act within the specified timeframe.

From April 1, 2026, the requirement to file a Statement of Estimated Tax (SET) would be removed. Instead of estimating income each year and filing a separate statement, taxpayers would generally pay instalments based on their previous year’s taxable income.

If the previous year’s income was nil, or if income in the current year is expected to be significantly lower, adjustments would be allowed. The change is aimed at reducing paperwork and simplifying compliance.

Another proposal seeks to provide certainty to compliant individual taxpayers.

From April 1, 2025, individuals who declare and pay tax on at least 120 per cent of their previous year’s taxable income, make full payment without claiming a refund, and submit a prescribed affidavit confirming compliance would have their returns accepted as filed. In effect, the Inland Revenue Department would not issue additional or amended assessments for those returns.

This could reduce the risk of prolonged tax queries for taxpayers who meet the conditions.

The Bill also proposes to bring more service providers under the 5 per cent withholding tax system. This means that when they are paid for their services, 5 per cent of the payment would be deducted at source and remitted to the Inland Revenue Department (IRD).

Those newly covered would include professionals and freelancers such as auditors, valuers, personal trainers, coaches, entertainers, photographers, therapists, beauticians, social media specialists, brand ambassadors and debt collectors,among others.

For many self-employed individuals, this would mean part of their tax is collected upfront rather than being paid later.

The draft law also proposes enhanced capital allowances for certain investments approved by the Board of Investment, revised rules on allowable deductions and tax residency, and specific provisions affecting sectors such as insurance and collective investment funds.

Taken together, the proposed amendments are part of the continued effort by the Government to widen the tax base, strengthen compliance and improve revenue collection, while offering targeted relief to clear older tax arrears.

However, it must be noted that the final impact on households and businesses will depend on the version of the Bill that is ultimately passed by Parliament.

14 Jun 2026 1 hours ago

14 Jun 2026 3 hours ago

14 Jun 2026 4 hours ago

14 Jun 2026 4 hours ago