03 Dec 2025 - {{hitsCtrl.values.hits}}

By First Capital Research

Owing to the persistence of uncertainties triggered by adverse weather conditions, the secondary market witnessed yet another day of limited activity yesterday.

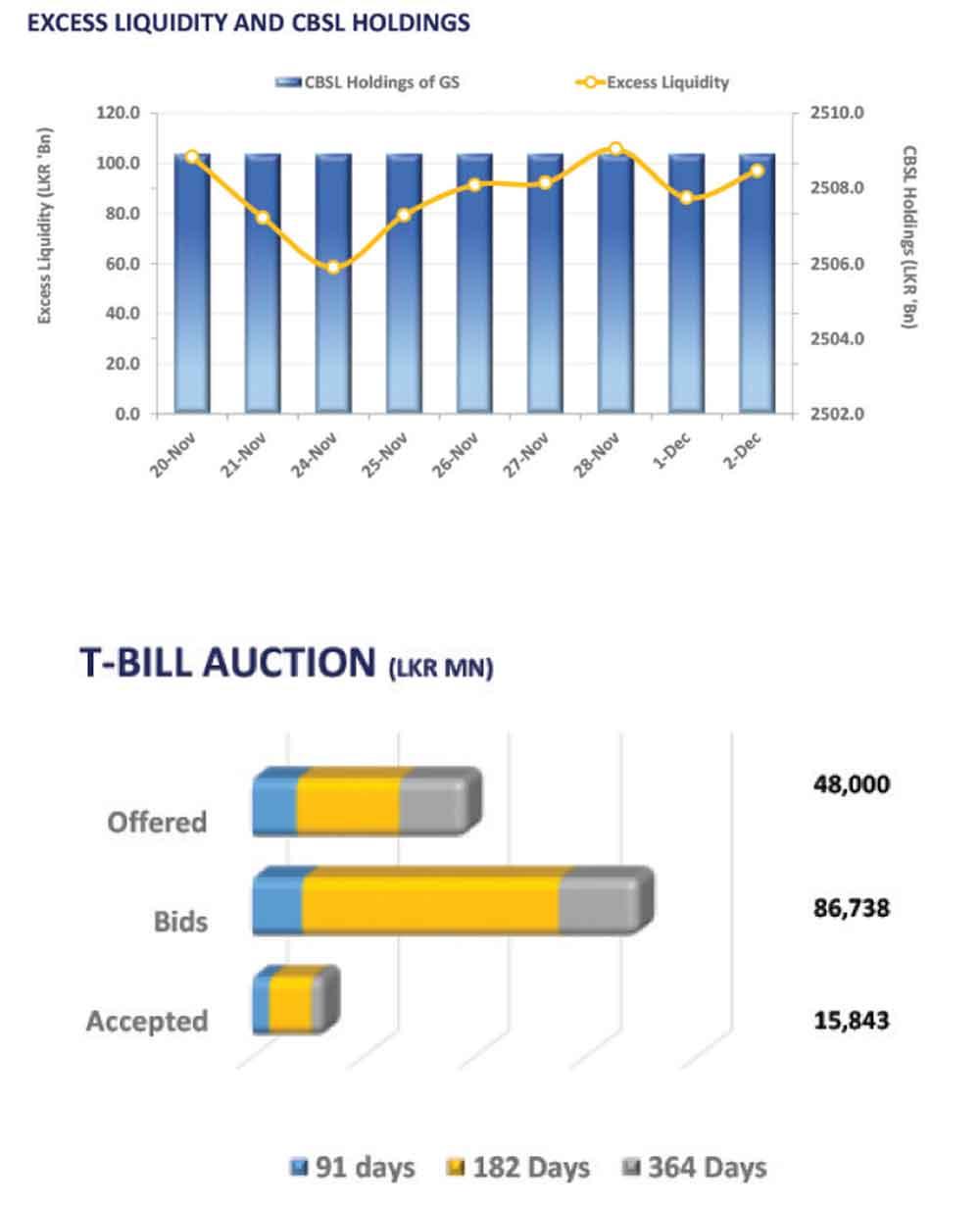

However, similar to Monday, some selling pressure was evident. Moreover, CBSL conducted its weekly T-Bill auction today, raising a mere fraction of the original offer while weighted average yields held largely steady.

Yesterday, the Central Bank appeared cautious in its acceptance of bids raising Rs. 15.8bn against the initial offer of Rs. 48.0bn. The 3M T-bill raised Rs. 3.9bn while the weighted average yield inched 1-bps down to 7.51%. The 6M and 12M bills raised Rs. 9.3bn and Rs. 2.6bn respectively, while weighted average yields held steady at 7.91% and 8.03%.

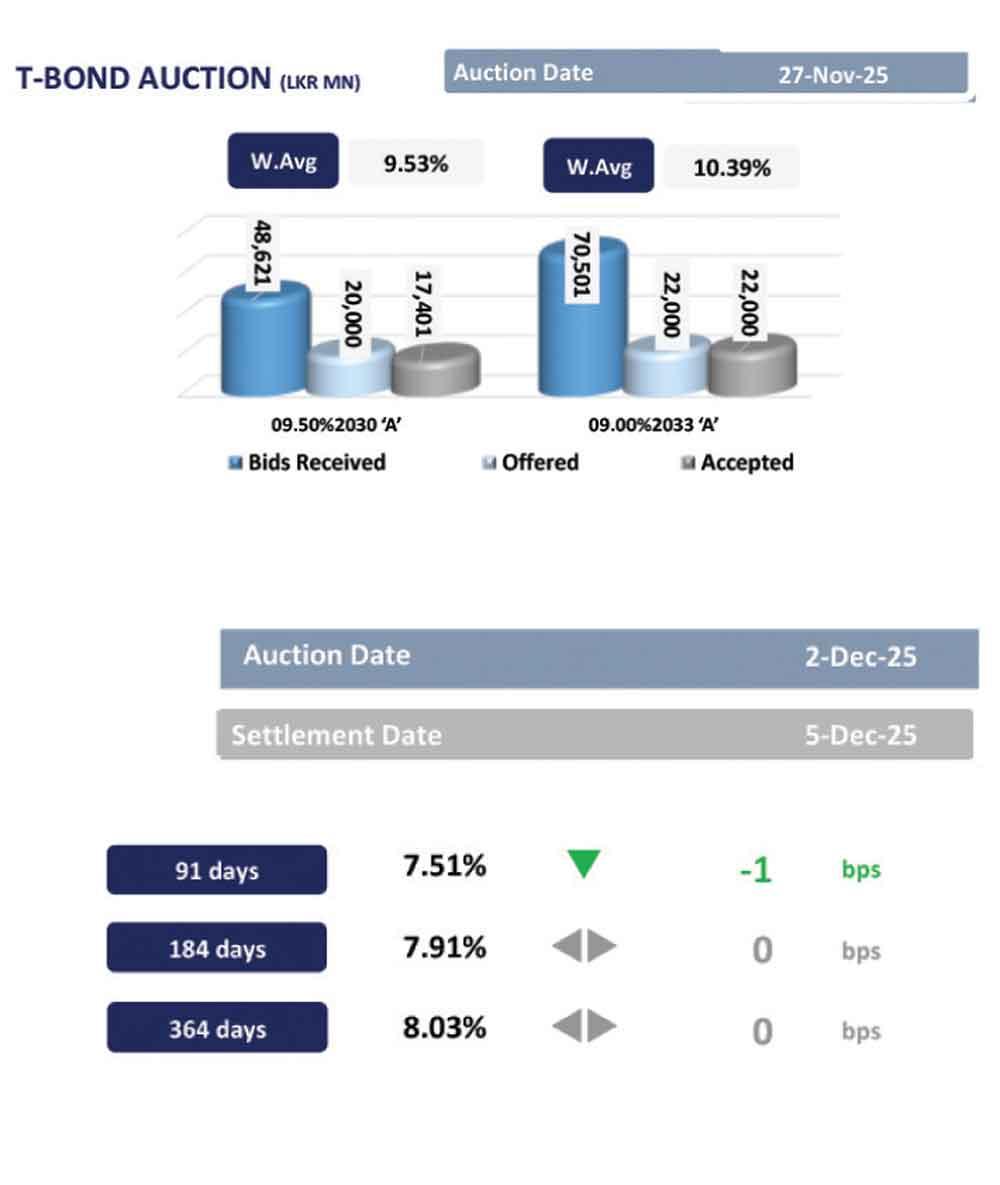

At the short end of the curve, 15.10.2029 and 15.12.2029 traded between 9.60% to 9.70% while 01.07.2030 traded at 9.70%. Moving ahead, 15.03.2031 was seen changing hands between 9.99% to 10.07% and 15.12.2032 traded at a rate of 10.35%.

In terms of 2033 maturities 01.06.2033 and 01.11.2033 were seen trading between 10.50% to 10.55%. Finally, 15.09.2034 traded at 10.65% while 15.06.2035 traded higher at 10.72%.

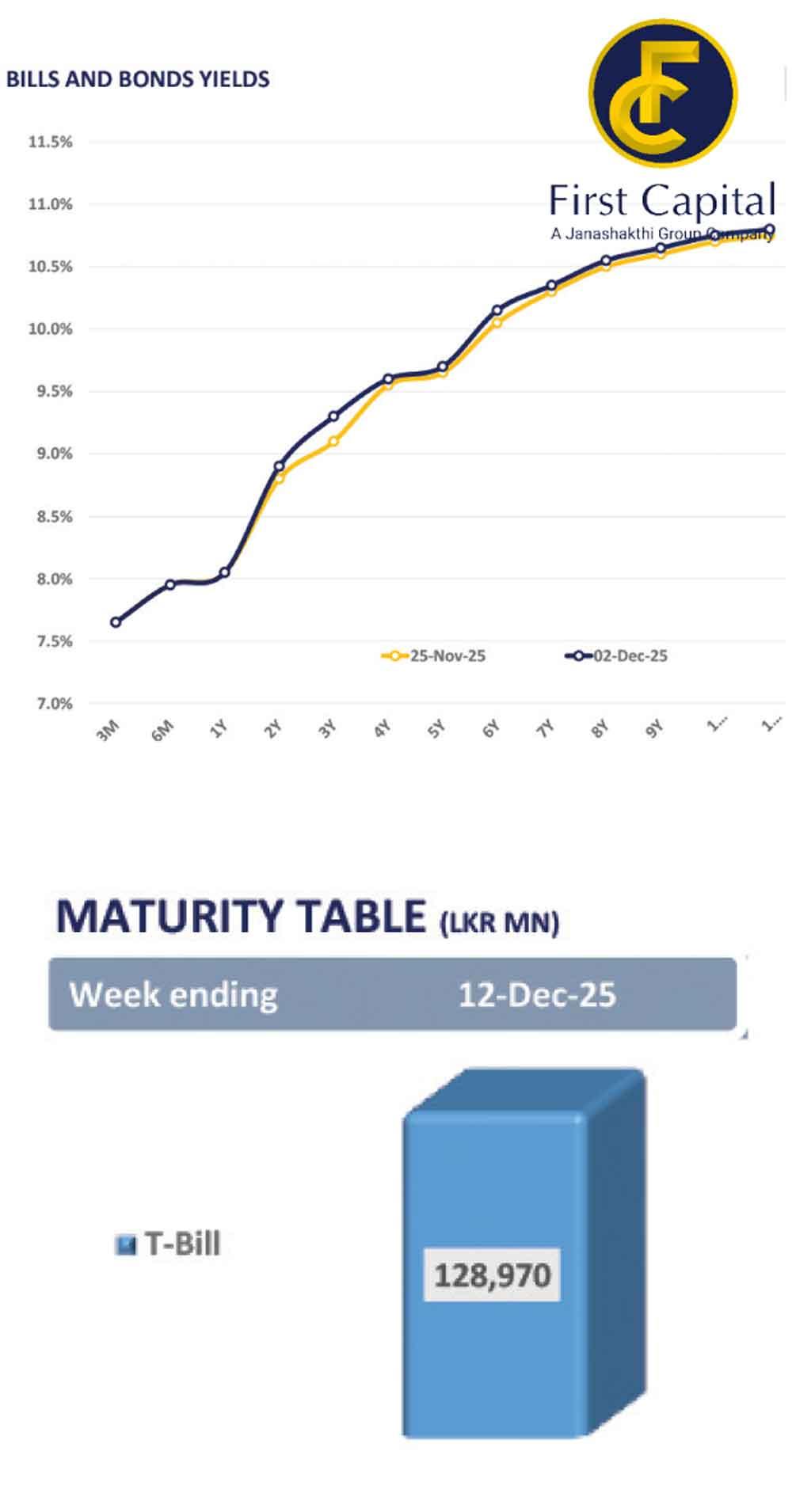

On the external front, the LKR depreciated against the USD, closing at Rs. 308.51/USD compared to Rs. 308.07/USD seen previously. Overnight liquidity in the banking system expanded to Rs. 97.0mn from Rs. 86.3mn recorded on the previous day.

14 Jun 2026 4 hours ago

14 Jun 2026 6 hours ago

14 Jun 2026 7 hours ago

14 Jun 2026 14 Jun 2026

14 Jun 2026 14 Jun 2026