21 May 2026 - {{hitsCtrl.values.hits}}

Murtaza Jafferjee, CFA, chairman of the Advocata Institute and CEO of JB Securities

Colombo, May 21 (Daily Mirror) - On 15 May 2026, President Anura Kumara Dissanayake, who also serves as Sri Lanka’s finance minister, issued an order under the Customs Ordinance imposing a 50% surcharge on imports classified under HS Code 87.02 (vehicles for the transport of ten or more persons including the driver), HS Code 87.03 (passenger motor vehicles), and HS Code 87.04 (vehicles for the transport of goods). Two-wheelers and three-wheelers have been exempted from the measure.

It is evident that the decision had leaked at least a day or two before it came into effect, as reflected by the unusually high number of letters of credit opened during that period. In financial markets, this would be characterized as front running — a form of market abuse whereby parties act on privileged information before it becomes public. There should be a proper investigation into how this information was leaked and who benefited from it.

One may infer that the President was advised to take such action due to rising pressure on the Sri Lankan rupee, as the foreign exchange market has witnessed an unusually rapid rate of depreciation in recent days.

Exchange rates are determined at the margin. They are influenced not only by those who need to convert currency for immediate transactions, but also by participants acting on expectations of future currency movements, e.g. foreign investors selling out of the GSEC market. During periods of heightened uncertainty and volatility, speculative behavior tends to intensify. Sellers of foreign exchange may delay conversions in anticipation of a weaker rupee, thereby constraining supply, while demand for foreign currency rises as businesses and individuals seek to lock in prevailing exchange rates before further depreciation occurs. These are classic manifestations of “animal spirits” in action, as famously described by John Maynard Keynes.

These dynamics can become self-reinforcing and ultimately self-fulfilling, exacerbating market imbalances and leading to exchange rate overshooting beyond levels justified by underlying fundamentals.

It is precisely during such periods of disorderly market conditions and excessive volatility that central banks typically intervene — not necessarily to defend a specific exchange rate level, but to stabilize expectations, restore market confidence, and prevent destabilizing speculative spirals.

The balance of payments (BoP) is the record of all economic transactions between a country and the rest of the world over a period of time. In simple terms, it tracks the flow of money into and out of the country. It is broadly divided into two parts. The current account records flows arising from normal economic activity such as exports and imports of goods and services, remittances, tourism earnings and income payments. The financial account records transactions that affect the country’s external balance sheet, namely changes in what the country owes to foreigners and what foreigners owe to the country. This includes foreign borrowing, foreign direct investment and purchases or sales of financial assets.

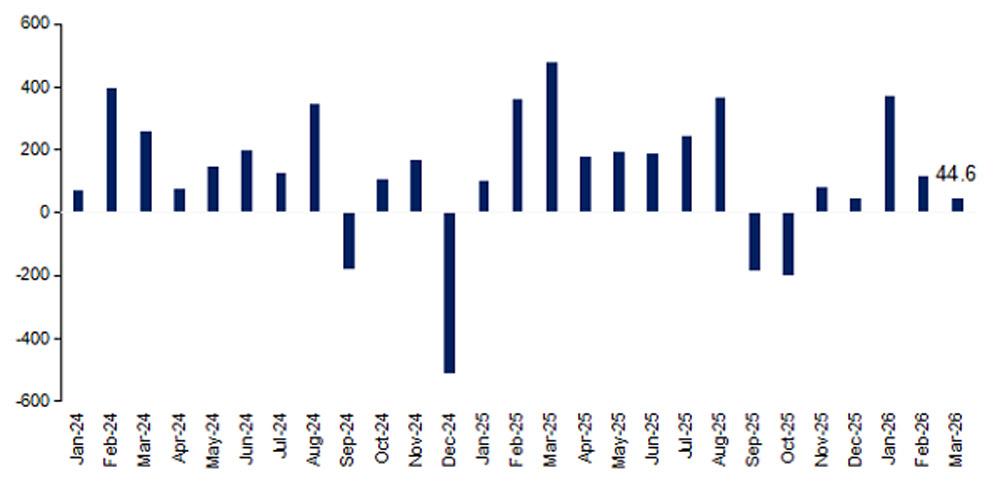

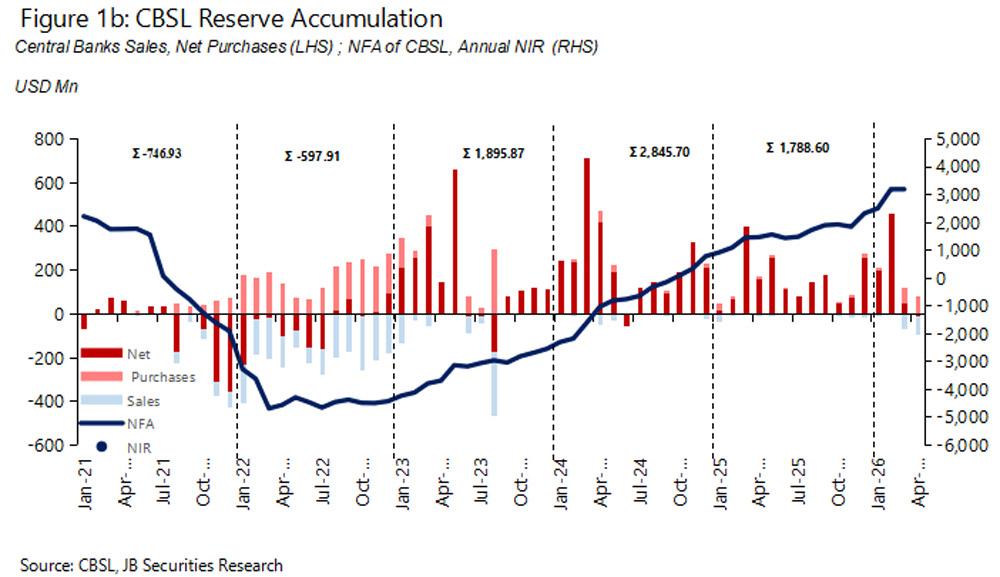

Fig. 1a illustrates the monthly current account balances since January 2024. The country’s recent macroeconomic framework has enabled the external account to record surpluses in most months. Fig. 1b illustrates the Central Bank’s purchases and sales of foreign currency in the domestic market. Net foreign reserves — a proxy for net international reserves (NIR), defined as gross reserves adjusted for reserve liabilities and used by the IMF as a key measure of reserve adequacy — improved from negative USD 4.7 bn in March 2022 to positive USD 3.2 bn in March 2026, representing a swing of USD 7.9 bn in just four years, a remarkable turnaround.

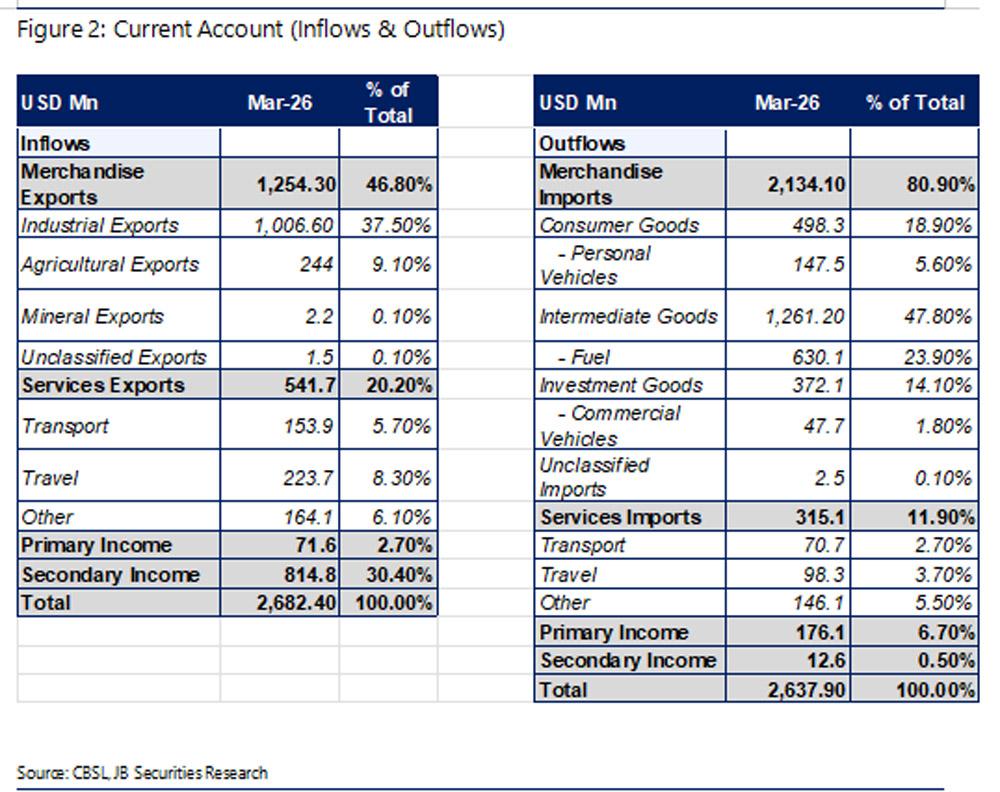

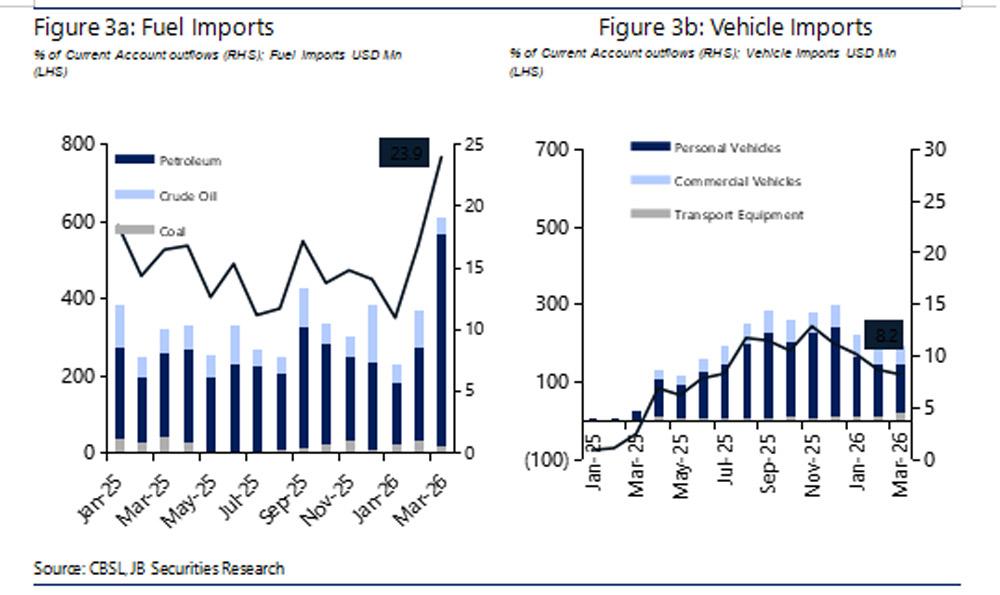

Fig. 2 illustrates the current account position for the month of March (with April data expected next week). Despite an almost 50% increase in the fuel import bill, the current account still recorded a surplus, supported by strong remittance inflows, the tail end of the tourist season, and lower vehicle imports, which collectively offset the higher fuel bill. Fuel imports increased to over USD 630 mn per month from around USD 400 mn previously. Vehicle imports, which peaked at nearly USD 300 mn per month in December, declined to around USD 200 mn, largely due to personal vehicle imports contracting from USD 240 mn to USD 147 mn. See Fig 3a and Fig 3b.

Vehicle demand has been contracting during this year due to satiation of pent up demand and unaffordability due to very high taxation.

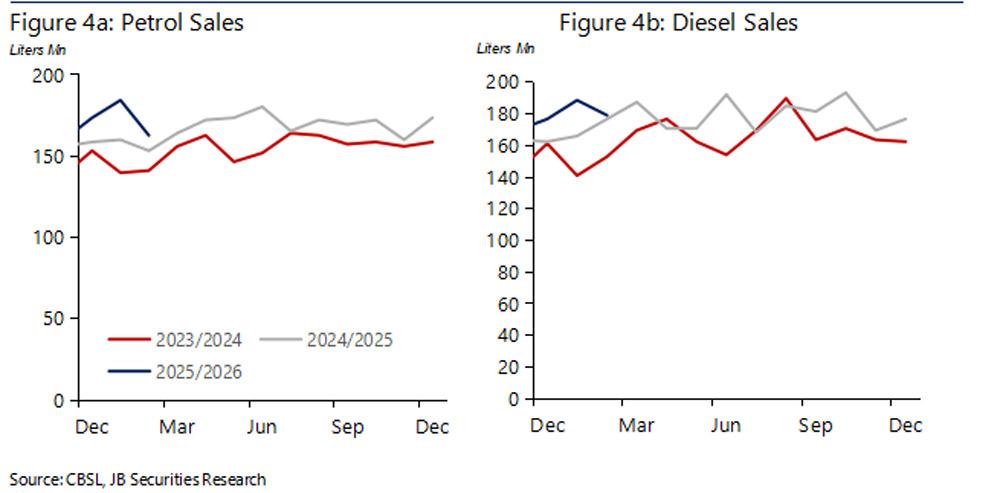

On the contrary fuel demand has been growing strongly due to strong economic momentum – See Fig 4a and Fig 4B.

Fuel is not a perfectly inelastic product; different categories of consumption exhibit different demand dynamics. Commercial fuel consumption, which is more strongly driven by economic incentives and cost considerations, is likely to respond fastest to price changes. Preliminary indications suggest that diesel consumption has already declined by around 13%, while the contraction in petrol consumption so far appears marginal.

Households and firms consume bundles of goods and services, meaning relative prices also matter. While fuel may not have perfect direct substitutes, there are indirect substitutes and behavioural adjustments that influence consumption patterns. When prices rise and incomes weaken, households tend to reduce discretionary expenditure and economise on non-essential travel and consumption.

By suppressing the price mechanism through subsidies, the market’s ability to efficiently allocate scarce resources is weakened, resulting in distorted consumption and investment decisions.

The conventional narrative has long been that diesel is the “poor man’s fuel”, reflecting the greater reliance of lower-income groups on public transport. However, the last Household Income and Expenditure Survey (HIES) conducted in 2019 indicated that around 60% of households owned some form of vehicle — a proportion that has likely increased since then, although the vehicle stock itself may have aged considerably following import restrictions.

Diesel consumption no longer significantly exceeds petrol consumption (excluding power generation), with diesel demand now only marginally higher than petrol demand, unlike the situation 25 years ago. The rapid expansion of the vehicle fleet — particularly the addition of nearly 5 million two-wheelers and 1.2 million three-wheelers — has fundamentally altered Sri Lanka’s fuel consumption profile.

Petrol 92 currently carries a quantity-based tax of LKR 72 per litre, compared to LKR 50 on auto diesel. Both fuels are also subject to VAT and SSCL, bringing the cumulative tax incidence to approximately LKR 137 per litre for petrol and LKR 112 per litre for diesel. These excise taxes are, in essence, corrective taxes intended to account for negative externalities associated with fuel consumption. The higher tax burden on petrol is also defensible on policy grounds, given that petrol-powered vehicles are predominantly personal vehicles that impose greater external costs through congestion, accidents, and urban road usage.

While the precise quantum of these taxes may not have been determined through a rigorous scientific framework, the broader policy rationale remains coherent. Higher fuel taxation is intended to discourage excessive consumption and moderate demand for imported fuel. The fact that these taxes also constitute a major source of government revenue is secondary, though significant — generating approximately LKR 12 bn per month from petrol and LKR 9 bn from diesel under normal conditions.

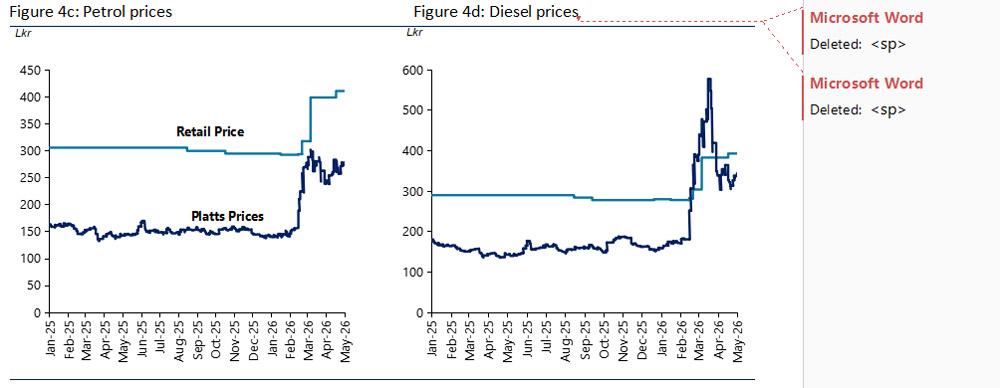

Based on my estimates, the subsidy promised to fuel distributors is insufficient to fully compensate them for their costs (see Fig. 4c and 4d). Sri Lanka’s fuel distribution market now consists of four players. CPC accounts for approximately 58% of the market, while the remaining three operators collectively account for around 42%. These include marquee foreign investors, with both Sinopec and RM Parks reportedly assured a distribution margin of 4%.

Attempting to operate on the assumption that these firms will eventually be permitted to recoup losses once global oil prices decline reflects the same flawed logic that contributed to Sri Lanka’s eventual bankruptcy. Deferred losses do not disappear; they merely accumulate as contingent liabilities. As the popular song goes, “if tomorrow never comes.”

According to the same 2019 HIES, the top 20% of households accounted for 51% of national income and 46.7% of total expenditure, while the bottom 20% received only 4.6% of income and accounted for 6.1% of expenditure. Based on an earlier household survey, the World Bank estimated that around 70% of the direct and indirect benefits of fuel subsidies — primarily arising from tax subsidies and under-recovery pricing — accrued to the top 30% of households.

Estimates also indicate that a typical Honda scooter consumes only around 29% of the fuel used by a small crossover vehicle such as the Toyota Raize for the same distance travelled; for larger SUVs, the proportion is even smaller. Rich households who consume more fuel benefit more from price subsidies.

Various studies suggest that bus usage has gradually declined over the years due to rising personal vehicle ownership — a trend reflected in the growing congestion on Sri Lankan roads. Buses are estimated to account for only around 15% of total diesel consumption, while the railways account for roughly 2%, including both passenger and freight operations. Consequently, the bulk of diesel consumption today is attributable to wider commercial and private economic activity rather than public passenger transport alone.

In April, the Government announced a LKR 100 bn relief package over a three-month period, of which LKR 60 bn was allocated for fuel subsidies. The diesel subsidy amounts to approximately LKR 100 per litre, effectively offsetting most taxes, including VAT. For businesses able to claim input tax credits on fuel, diesel can effectively be purchased below its true economic cost. The petrol subsidy is lower at around LKR 20 per litre, implying only a partial reduction of the corrective taxes embedded in retail prices.

To place the magnitude of the subsidy in context, the Government has estimated monthly expenditure on the Aswasuma welfare programme at around LKR 25 bn at the upper end. Aswasuma provides direct cash transfers to approximately 1.7 million households. The fuel subsidy alone therefore amounts to nearly 80% of the monthly fiscal cost of the country’s primary targeted welfare programme.

My household is likely to receive more than 50 times the benefit received by a household in the poorest decile, whether directly through fuel consumption or indirectly through lower prices for goods and services. In economics, outcomes matter more than intentions.

Motor vehicles in Sri Lanka are already subject to a complex and extraordinarily high tax structure. This includes quantity-based taxation through excise duties, as well as ad valorem taxes such as customs duty, currently levied at 30%, and a luxury tax imposed on the incremental value above a specified threshold. Both the threshold and the applicable rate vary depending on the vehicle’s power source, with electric vehicles benefiting from higher thresholds and lower rates relative to hybrids and internal combustion engine vehicles. In addition, Value Added Tax (VAT) and the Social Security Contribution Levy (SSCL) are imposed on the import value together with the accumulated duties and levies. As a result, the total tax burden ranges from roughly 90% at the lower end for some two-wheelers to well above 300% for large internal combustion engine vehicles.

The new 50% surcharge effectively raises the customs duty rate from 30% to 45%. Because VAT at 18% and the 2.5% SSCL are applied on top of the enhanced duty-inclusive value, the cascading effect increases the tax burden by approximately 18.05% of the CIF value. This pushes total taxation on many vehicles from around 120% to 140% of CIF, equivalent to roughly 8.5% of the final retail selling price.

At these levels, Sri Lanka’s vehicle taxation regime is likely among the highest in the world. Outside highly space-constrained city-states such as Singapore — where punitive vehicle taxation is deliberately used to discourage private vehicle ownership alongside the provision of world-class public transport — few countries impose such an extreme fiscal burden on motor vehicles.

If you tax something heavily, you will generally get less of it; if you subsidize something — including through preferential or lower taxation relative to other goods — you will tend to get more of it. Tax policy therefore shapes economic behavior and resource allocation.

In the case of demerit goods — goods considered socially harmful because they impose costs on individuals or society, such as cigarettes and alcohol — it is prudent fiscal policy to impose corrective taxes. These taxes are intended to internalize the social and health costs associated with their consumption and thereby discourage excessive use.

Vehicles, however, are not demerit goods. They are productive economic assets that enable mobility, logistics, trade, and commerce across the economy. Over taxing vehicles takes away economic freedom of your people, it also increases the gap between the haves and have nots for mobility is fundamental to ones economic wellbeing.

Historically, vehicle taxation has been particularly lucrative because it exploits certain behavioral preferences among wealthier consumers. Many individuals derive utility from vehicle ownership beyond pure transportation value, including social status, prestige, and personal identity rather than relying on the vitality of their personality. In addition, vehicles came to be perceived by many households as a quasi-real asset during past episodes of macroeconomic instability and high inflation, where nominal vehicle prices retain value over time although it is a depreciating asset.

In 2025, taxes collected from vehicle imports — largely during the last seven months of the year — generated approximately LKR 905 billion from roughly USD 2 billion in imports. The increase in indirect taxes, dominated by vehicle-related taxation, was one of the largest contributors to GDP growth, accounting for an estimated 16.2 percent contribution. It was also the primary reason government tax revenue (LKR 5.05 tn) exceeded budgeted target (LKR 4.59 tn) — a relatively rare occurrence.

Although vehicles are imported, they catalyze substantial domestic economic activity once brought into the country. They trigger a broad downstream economic ecosystem including trading, financing, insurance, leasing, registration, repairs, maintenance, fuel distribution, logistics, and accessory sales. Suppressing this ecosystem too aggressively risks weakening growth and government revenue simultaneously.

That would be particularly damaging at a time when the economy is already facing external shocks arising from the Gulf conflict, including higher energy prices, weaker tourism receipts, elevated fertilizer costs, and pressure on tea export earnings.

Sri Lanka’s road to economic ruin has often been paved with good intentions pursued through deeply flawed policy choices. As John F. Kennedy is reported to have said, “The ignorance of one voter in a democracy impairs the security of all.” In Sri Lanka’s case, economic illiteracy among the electorate has arguably been one of the most important drivers of long-term economic underperformance, as populist politics has too often crowded out sound economic policymaking.

A basic understanding of economics should therefore be treated as foundational civic knowledge, much like science or mathematics. Citizens do not need to become economists, but they should understand core concepts such as taxation, inflation, debt, productivity, trade-offs, incentives, and the consequences of unsustainable fiscal and monetary policies.

Without a population capable of critically evaluating economic promises, democratic systems become vulnerable to short-term populism at the expense of long-term national welfare. Those entrusted with reforming the education system should take heed of this reality and ensure that economic literacy becomes an integral part of school education for the future wellbeing and resilience of the country.

04 Jun 2026 5 hours ago

04 Jun 2026 5 hours ago

04 Jun 2026 6 hours ago

04 Jun 2026 6 hours ago

04 Jun 2026 6 hours ago