18 Oct 2023 - {{hitsCtrl.values.hits}}

Raising government revenue is critical for Sri Lanka to recover from the current economic crisis and create a more sustainable economic environment. However, taxes should be paid by those who can bear the burden.

Raising government revenue is critical for Sri Lanka to recover from the current economic crisis and create a more sustainable economic environment. However, taxes should be paid by those who can bear the burden.

Personal Income Taxes (PIT) is an effective instrument in generating revenue as well as in reducing inequality through revenue redistribution. In Sri Lanka, there has been a steady decline in revenue from PIT, from 0.9 percent of GDP in 2000 to 0.2 percent of GDP in 2022. Revenue collection is lower than that of even other low-income economies.

Furthermore, the PIT tax revenue as a percentage of direct tax revenue declined from 40 percent in 2000 to 9.3 percent in 2022, although GDP per capita increased from US $ 869 in 2000 to US $ 3,474 in 2022.

Advanced economies raise approximately 9 percent of GDP from PIT, while emerging economies and low-income economies raise only 3.1 percent and 2.1 percent of GDP, respectively.

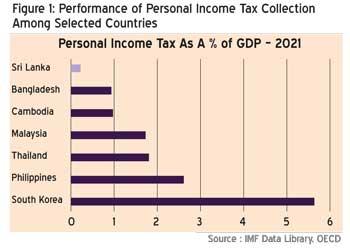

Sri Lanka reported the lowest contribution of PIT as a percentage of GDP in 2021, both among advanced economies in Asia such as South Korea as well as developing economies such as Bangladesh, Malaysia and Vietnam (See Figure 1).

Narrow tax base

The narrow tax base is one of the main reasons for Sri Lanka’s low PIT revenue performance. A narrow base not only limits revenue generation but it also makes revenue collection reliant on a small segment of the population.

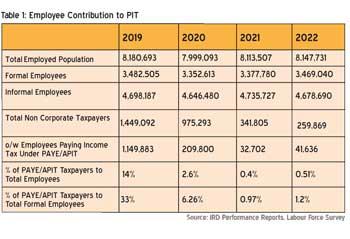

The number of income tax payers under the Pay As You Earn (PAYE)/Advanced Personal Income Tax (APIT) scheme as a percentage of the total employed population shows a relatively small proportion of the workforce contributing to income taxes (see Table 1). In 2019, the proportion of taxpaying employees was 33 percent. This proportion declined to less than one percent in 2021, due to abolishing of PAYE taxes, with effect from January 1, 2020.

A voluntary APIT system was introduced with effect from April 1, 2020, where employees can opt in. This shift not only led to a revenue decline but also created monitoring gaps. With effect from January 1, 2023, it was mandated for employers to deduct APIT from employees’ income, reverting to the original PAYE scheme.

The large informal sector also contributes to the narrow tax base and low PIT performance. According to the Labor Force Survey 2022, the informal sector accounts for around 58 percent of total employment (see Table 1).

A large portion of the economy operating outside formal regulation enables tax evasion and avoidance. Transforming the current informal self-employment system to a modern formal employee-employment system would be one way to improve tax revenue collection.

Two alternative recommendations are proposed to capture informal economic activities into the tax net. Establishing a universal online payments system would reduce cash transactions in the economy, enabling better monitoring and secondly, by introducing a unique digital identification system that connects tax accounts with income sources, bank accounts, motor vehicle and land registration, etc. Authorities could cross check information provided in income tax returns as well as identify individuals who do not file returns.

Tax-free threshold and tax slabs/brackets

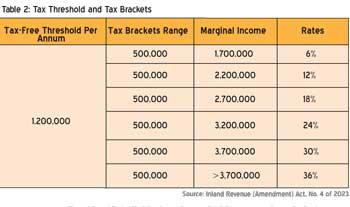

In the recent amendment to the Inland Revenue Act, the tax-free threshold for income was reduced from Rs.3 million per annum to Rs.1.2 million per annum. Further, the tax brackets were reduced from Rs.3 million to Rs.0.5 million. Accordingly, the incremental tax rate for each additional Rs.0.5 million of income was set at 6 percent (see Table 2).

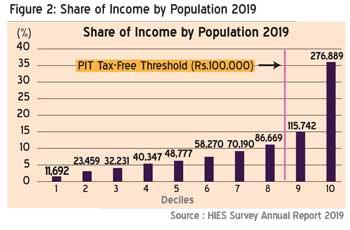

Applying the current tax-free threshold, income taxes are applicable to approximately the top 15 percent of households, where around 36 percent of total income is concentrated (see Figure 2).

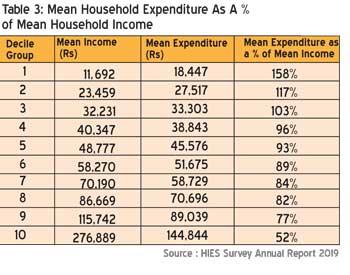

According to the national poverty line for July 2023, the minimum monthly expenditure per person required to meet the basic needs is Rs.15,978. Hence, the total cost for a family of four is approximately Rs.65,000 per month. Assuming salaries and wages remain unchanged at 2019 levels, more than two-thirds of income is spent by households up to the ninth decile, (see Table 3).

Any additional financial burden, including income taxes, could further reduce the disposable income of households up to the ninth income decile. Hence, information on household income and expenditure patterns must be considered when setting income tax thresholds.

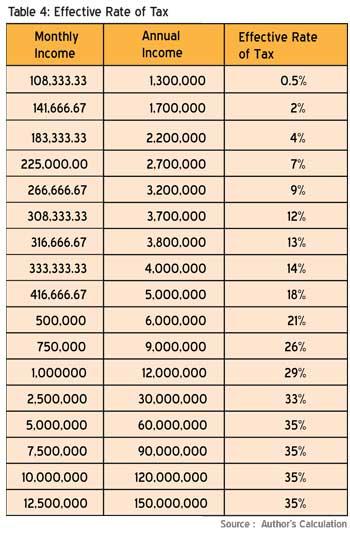

Although the current tax system applies differential tax rates based on income brackets, an analysis of the effective tax rates paid within these brackets indicates a less than progressive tax system. An individual crossing the tax-free threshold of Rs.1.2 million per annum (equivalent to a monthly income of Rs.100,000) pays an effectives tax rate of one percent, which gradually increases to 12 percent until the highest income bracket is reached at over Rs.3.7 million (which is equivalent to a monthly income of Rs.308,333). All the income levels above this income would be taxed at the highest nominal marginal rate of 36 percent.

However, after a particular income level, the effective tax rate flattens (see Table 4). This implies that individuals in the highest income categories effectively pay less taxes. Expanding the income tax brackets would introduce more fairness and progressivity into the tax system.

The fairness of the tax system is further exacerbated as those whose main income sources are subject to capital gains are taxed at only 10 percent versus those whose income are subject to PIT, who are taxed at a higher rate of 36 percent.

As wages and salaries rise to keep up with inflation, individuals may find themselves earning more in nominal terms but their purchasing power remains relatively unchanged. Adjusting thresholds for inflation ensures that employees are not disproportionately burdened by bracket creep where taxpayers are pushed into higher brackets due to inflation.

A proper rationale and scientific basis for determining thresholds, tax slabs and tax rates is needed to increase revenue collection and ensure fairness in the tax system. Also, the proposed tax system should generate the estimated tax revenue by the end of the year.

Frequent ad hoc policy changes

Tax policy is frequently subjected to change, without proper economic rationale. For instance, the tax slabs for PIT have been revised nine times while the tax-free threshold was revised five times since 2000. Frequent and ad hoc policy changes complicate tax administration and reduce tax compliance.

Conclusion

The country has failed to meet the first quarter targets for revenue under the International Monetary Fund’s Extended Fund Facility programme. Raising government revenue will be critical to remaining within the programme. Improving revenue collection from income taxes will be critical to achieving the revenue targets, while broadening the tax base will ensure the burden of taxation falls on the broadest shoulders.

(Roshan Perera is a Senior Research Fellow at the Advocata Institute. She can be contacted via [email protected]. Thashikala Mendis is a Data Analyst at the Advocata Institute. She can be contacted via [email protected]. Janani Wanigaratne is a Research Consultant at the Advocata Institute. She can be contacted via [email protected].)

24 Jun 2026 1 hours ago

24 Jun 2026 4 hours ago

23 Jun 2026 6 hours ago

23 Jun 2026 7 hours ago

23 Jun 2026 7 hours ago