Reply To:

Name - Reply Comment

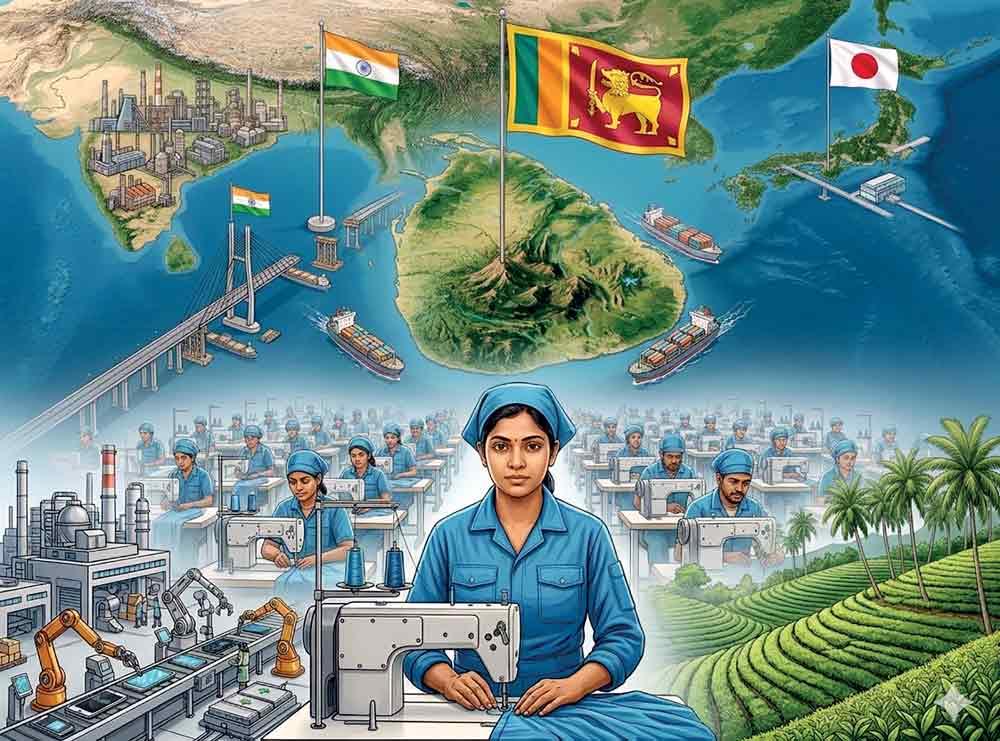

A potential catalyst lies in an India–Sri Lanka export-oriented industrial corridor supported by Japanese investment. This trilateral initiative, proposed by the Japanese government, should be pursued in earnest. Japan brings capital, technology, and industrial discipline; India provides scale and manufacturing ecosystems; Sri Lanka offers geography and connectivity.

A potential catalyst lies in an India–Sri Lanka export-oriented industrial corridor supported by Japanese investment. This trilateral initiative, proposed by the Japanese government, should be pursued in earnest. Japan brings capital, technology, and industrial discipline; India provides scale and manufacturing ecosystems; Sri Lanka offers geography and connectivity.

“Modern manufacturing is no longer national—it is organised through geoeconomic networks.”

“Economic outcomes are no longer determined primarily by efficiency, but by strategic alignment and geopolitical positioning.”

“Neither tourism nor traditional exports can substitute for industrial depth.”

“The objective is integration into India’s supply chains, not competition with them.”

“Sri Lanka has missed previous industrial transitions... The difference now is whether the country chooses to act while the window is still open.”

The global manufacturing landscape is undergoing a radical transformation, shifting from national production to complex geoeconomic networks where strategy, finance, and technology converge. As supply chains fragment into “trusted” ecosystems, the traditional models of efficiency are being replaced by strategic alignment and geopolitical positioning. Sri Lanka stands at a critical crossroads, currently constrained by a narrow reliance on apparel, tea, and tourism sectors increasingly vulnerable to automation and external shocks. To escape this structural trap, the nation must move beyond market access to true supply chain integration. By leveraging its geography through a trilateral partnership with India and Japan, Sri Lanka can secure its place in precision niches like electronics and medical devices before the strategic window closes.

As Apple Inc. marks its 50th anniversary, its trajectory offers a clear lesson: modern manufacturing is no longer national—it is organised through geoeconomic networks. Production, technology, finance, and strategy now move together, shaping where and how value is created.

Apple did not build production in a single geography. It drew on Japan’s precision manufacturing systems, scaled through China’s industrial depth, and is now diversifying production to India, reflecting the reorganisation of global supply chains. These networks were anchored by firms such as Foxconn, while companies like BYD emerged from within this ecosystem and now compete with it.

This evolution illustrates a deeper shift: globalisation is no longer a uniform system but a set of overlapping, competing production architectures.

A Fragmenting Geoeconomic Order

The global economy is entering a phase of geoeconomic fragmentation, where trade, investment, technology, and security are increasingly interlinked. Economic outcomes are no longer determined primarily by efficiency, but by strategic alignment and geopolitical positioning.

“China Plus One,” “friend-shoring,” and “trusted supply chains” now define investment behaviour. Distinct production ecosystems are emerging—China consolidating, the United States and its partners reshaping trusted supply chains, India expanding, and Japan and Europe aligning production networks.

At the same time, opportunities with China will continue to exist across trade, investment, and selected industrial cooperation, reflecting the increasingly multi-polar and non-exclusive nature of global supply chains.

In this environment, geography and trust carry as much weight as cost.

Sri Lanka’s Structural Constraint

Sri Lanka entered global manufacturing through apparel, supported by quota access to Western markets.

China also began with labour-intensive exports, including garments, but used them as a transition platform into electronics and advanced manufacturing. Sri Lanka, by contrast, remained anchored to a narrow industrial base.

That distinction now defines the constraint.

Even apparel manufacturing is increasingly exposed to automation, robotics, and AI-driven production systems, alongside consolidation and the reorganisation of global supply chains. Apparel companies are therefore increasingly likely to reassess their location decisions in response to competitiveness constraints, including cost pressures and tightening labour availability.

Tea, while remaining an important export, reflects the structural limitation of reliance on a narrow, land-based sector with limited scalability and weak linkages to broader industrial transformation.

Tourism and Narrow Export Cycles

Sri Lanka’s export economy has been shaped by a pattern of reliance on a narrow set of dominant sectors at a time, rather than broad-based diversification.

Tourism, particularly since 2009, has expanded and integrated Sri Lanka into global service networks. Yet it remains highly vulnerable to external shocks and domestic instability.

Neither tourism nor traditional exports can substitute for industrial depth.

The Missing Variable: Competitiveness

At the core of Sri Lanka’s challenge lies competitiveness—not as an abstract concept, but as a set of practical constraints that shape investment decisions.

The country faces persistent weaknesses in human capital, infrastructure quality, logistics efficiency, and energy costs. In addition, the high cost of infrastructure development—including construction and materials—raises the upfront capital required for industrial investment, reducing Sri Lanka’s attractiveness relative to competing locations.

Equally important is the credibility of the policy environment. Frequent changes in tax and investment regimes have weakened investor confidence and increased perceived risk.

Without addressing these underlying constraints, industrial strategy will remain aspirational rather than operational.

A Narrow but Real Opportunity

A potential catalyst lies in an India–Sri Lanka export-oriented industrial corridor supported by Japanese investment. This trilateral initiative, proposed by the Japanese government, should be pursued in earnest.

Japan brings capital, technology, and industrial discipline; India provides scale and manufacturing ecosystems; Sri Lanka offers geography and connectivity.

Special economic and export-oriented industrial zones within this framework could anchor Sri Lanka’s integration into regional value chains across the Palk Strait, while positioning the country as a logistics centre and energy hub linked to southern India’s industrial expansion.

The objective is integration into India’s supply chains, not competition with them.

From Apparel to Selective Industrialisation

Sri Lanka cannot compete broadly across manufacturing. Its opportunity lies in selective participation in specific segments of global value chains, rather than attempting scale-driven industrialisation.

A handful of world-class apparel manufacturers already possess the organisational capability, export experience, and compliance standards that could be leveraged into adjacent sectors.

Practical entry points include electronics assembly (such as cable harnesses and PCB-level assembly), automotive subcomponents (including wiring systems and light engineering parts), and medical devices (particularly disposables, diagnostics, and contract manufacturing). These represent selective, capability-aligned entry points within existing or emerging value chains.

In addition, industrial services linked to logistics—final assembly, testing, packaging, and re-export processing—could form an important part of this ecosystem. The emphasis must be on precision niches within larger supply chains, aligned closely with India’s expanding manufacturing base.

Strategic Minerals: A Re-emerging Advantage

Sri Lanka’s mineral base adds a further dimension.

Before the Second World War, Sri Lanka was a leading exporter of high-purity vein graphite. While that position has declined, the resource remains globally significant.

Together with ilmenite, phosphate, and quartz, these materials have applications across energy storage, advanced materials, electronics, and industrial manufacturing.

Integrated into regional value chains, including downstream processing where viable, they could support a more diversified industrial base rather than remain primary exports.

Currencies, Tariffs, and Trade Architecture

The evolving production system is mirrored by changes in global finance.

The Bretton Woods system continues to underpin global trade, but its dominance is gradually fragmenting. Regional currencies such as the Indian Rupee and the Chinese Renminbi are playing a growing role in cross-border transactions.

At the same time, digital systems and cryptocurrency are beginning to influence how trade is settled and financed.

Trade policy itself is also being redefined. Tariffs and rules of origin are no longer peripheral tools; they shape where investment flows and how deeply countries are integrated into supply chains.

Trade agreements must now serve as instruments of supply chain integration, not merely market access. This will require negotiating agreements that align tariffs, rules of origin, and investment frameworks with Sri Lanka’s role in regional value chains, particularly with India.

Conclusion: A Closing Window

Sri Lanka faces a narrowing strategic moment within a rapidly changing geoeconomic order.

It can continue along its current path—relying on remittances, tourism, and a constrained industrial base.

Or it can reposition itself within emerging regional production networks while the system is still in transition.

This will require a national consensus that has often proved elusive.

Sri Lanka has missed previous industrial transitions.

The difference now is not the absence of opportunity.

It is whether the country chooses to act while the window is still open.

The writer Milinda Moragoda is the Founder of the Pathfinder Foundation.