Reply To:

Name - Reply Comment

Sovereign debt restructuring can be pre-emptive or post-default. A default is inherently costly, as it can result in a sustained loss of access to capital markets. That leaves pre-emptive restructuring when a country deems itself unable to service outstanding debt.

Sovereign debt restructuring can be pre-emptive or post-default. A default is inherently costly, as it can result in a sustained loss of access to capital markets. That leaves pre-emptive restructuring when a country deems itself unable to service outstanding debt.

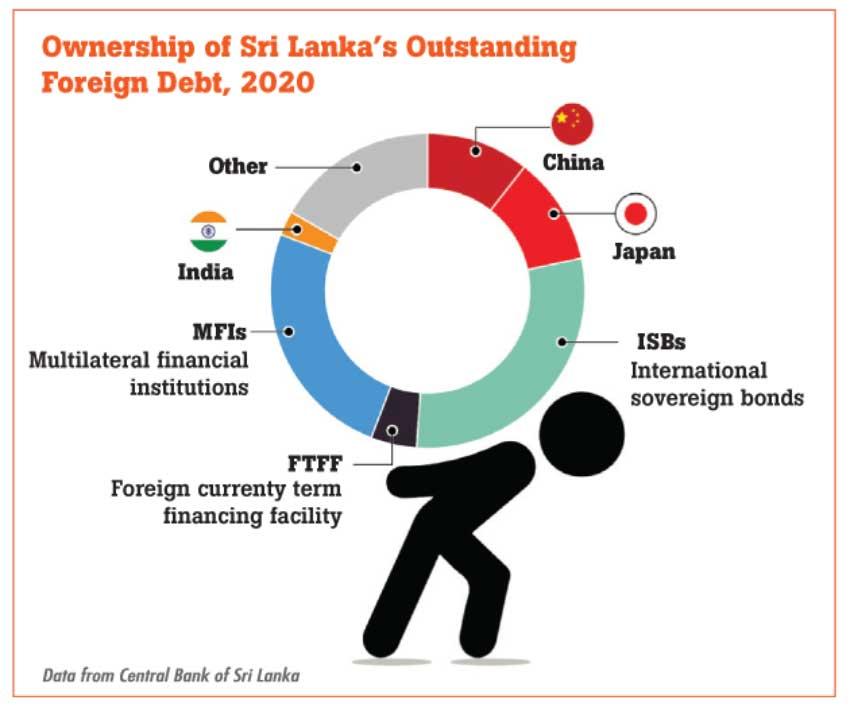

The complex creditor landscape of today though makes governments reluctant to entertain sovereign debt restructuring. The landscape of sovereign borrowing has evolved from a small group made up of multilateral organisations, a few commercial banks and the ‘Paris Club’ of rich countries to something much more complicated.

In recent decades, emerging markets and developing economies have borrowed proportionately more from international bond markets with their dispersed private investors and tapped new non-Paris Club lenders like China. From the sovereign’s perspective, this makes a potential debt restructuring operation particularly complicated.

The first step in any restructuring is calculating how much a country owes and to whom. This involves sharing detailed information on all categories of sovereign debt denominated in foreign currency, including collateralised liabilities and the debts of state-owned enterprises. The adoption of an IMF programme may be conditioned as part of a restructuring to underwrite the data, economic plan and the promise of macroeconomic and fiscal supervision.

Lenders will weigh the upfront losses of a debt standstill and restructuring against the total magnitude of losses in the event of a default. In entering restructuring talks, though they will also demand to do so on the principle of comparable treatment of creditors in any proposed debt reprofilings and restructurings.

Lenders will be mindful that any relief offered does not give preferential treatment to other creditors, especially in the face of new geopolitical power rivalries. This would typically mean that a country in distress asks for debt relief from friendly governments to whom it owes money and then seeks a comparable deal from private lenders.

Holdout problem

Over the past decades, there has been progress in governance frameworks to deal with sovereign debt crises but considerable gaps persist. In the COVID-19 era, the G-20 Common Framework for Debt Treatments applies only to low-income countries (LICs) and even then, does not compel the participation of private creditors. The emerging markets that have undergone debt restructuring most recently (e.g. Argentina and Ecuador) are categorised in academic research as countries with a track record of serial default – i.e. more than two default spells or episodes.

Given research evidence that the countries that have defaulted on their debt obligations in the past are more likely to default again in the future, creditors have an added incentive to enter into negotiations in such cases.

All told, with the creditor landscape transformed, debt restructuring is still very much a matter of ad hoc negotiations between a sovereign and its creditors.

The creditors are aware of their special legal protection that comes down to a question of money due but not paid. At the same time, creditors too have virtually no choice but to negotiate, as there will be inadequate assets to satisfy every creditor’s claims even with a successful legal remedy.

In the extreme, ‘vulture funds’ have used litigation as an investment strategy to buy the debt at a hefty discount and pursue full payment through the courts. Confronted with this reality, a negotiated resolution should appeal to both creditors and debtor country.

At the centre of such a coordinated effort will be creditor (especially bondholder) committees. The composition of such committees – inclusive of large institutional investors, hedge funds, etc. – is critical to obtain a relatively quick resolution. However, there are no guarantees of fast and efficient mechanisms and countries still risk fighting creditor lawsuits from those who may hold out.

Such potential holdout creditors may not necessarily take the view that what is good for the many is always good for the few. A disgruntled holdout creditor has the leverage to cause disturbing headlines, especially when countries resume bond market access once again at some point.

Holdout creditors can be reined in through exit consents – where a majority of holders can amend terms or as more commonly used now, employ collective action clauses (CACs) in bond agreements to bind minority holders. In the latter case, a specified supermajority of holders (usually 75 percent) can bind a minority to the terms of a debt restructuring.

But much depends on whether a debtor country’s outstanding stock of international sovereign bonds contains these clauses. Some countries have also adopted anti-vulture fund legislation that limits holdout creditor recovery as a deterrent.

Net benefit calculation

High uncertainty during a restructuring and the risk of prolonged negotiations means debt restructuring is still the last resort, to be done only if you must. A restructuring is a costly exercise with reputational downsides, loss of market access and more expensive debt issuances, weighed down further by concerns about adverse legal implications. For policymakers, a decisive step can be taken after a careful net benefit calculation of whether a country’s economic conditions are likely to deteriorate further without a restructuring or whether a timely restructure may reduce the total magnitude of upfront losses and return debt to a sustainable level at the lowest cost to both the country and its creditors.

(Dr. Dushni Weerakoon is Executive Director of the Institute of Policy Studies of Sri Lanka (IPS) and Head of its Macroeconomic Policy research. She joined the IPS in 1994, after obtaining her PhD and has written and published widely on macroeconomic policy, regional trade integration and international economics. She has extensive experience working in policy development committees and official delegations of the Government of Sri Lanka. She holds a BSc in Economics with First Class Honours from the Queen’s University of Belfast, UK and an MA and PhD in Economics from the University of Manchester, UK. She can be reached at [email protected])