Reply To:

Name - Reply Comment

By First Capital Research

The secondary market yesterday registered high trading volumes, with buying interest emerging at the long-end, post T-bond auction. Long-end yields slightly edged down, following the T-bond auction.

The secondary market yesterday registered high trading volumes, with buying interest emerging at the long-end, post T-bond auction. Long-end yields slightly edged down, following the T-bond auction.

Prior to the T-bond auction,buying interest was observed towards short-end maturities, where 15.02.2028, 15.03.2028 and 09.05.2028 traded in the range of 9.10%-9.00%.

Over 2029 segment, both 15.10.2029 and 15.12.2029 traded at 9.60%. Post T-bond auction, buying sentiment shifted the gear towards the long-end.

Among the long-term tenors that were traded, 01.06.2033 changed hands at 10.65%. Both 15.06.2034 and 15.06.2035 traded at 10.85%, while 01.07.2037 traded at 11.00%.

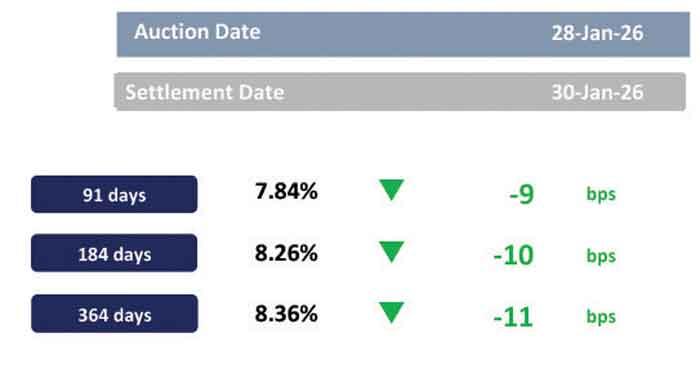

At the T-bond auction held yesterday, PDMO raised a total of Rs. 179.1bn against an offer of Rs. 205.0bn. Both 01.03.2030 and 15.06.2034 maturities were accepted in full, with Rs. 60.0bn and Rs. 80.0bn respectively.

However, only a portion of 01.07.2037 tenor was accepted at Rs. 39.1bn, against the offer of Rs. 65.0bn. Weighted average yields for the three maturities stood at 9.72%, 10.92% and 11.08% respectively.

On the external front, the LKR depreciated against the USD, closing at Rs. 309.65/USD compared to Rs. 309.61/USD seen previously. Overnight liquidity in the banking system contracted to Rs. 194.26bn from Rs. 211.53bn recorded previously.