Reply To:

Name - Reply Comment

- Microfinance grew 400 percent from 2000 to 2018.

- Only one microfinance company and 13 NGOs are registered under the Microfinance Act

- The CLS entails a 12-month payback period at 14 percent interest rates

The entrapment of rural communities, especially rural women, in a vicious debt cycle generated by thousands of unregulated microfinance organizations has reached  epidemic proportions, affecting almost three million people island-wide. Once seen as an instrument of rural upliftment, microfinance loans have now gained notoriety for encouraging multiple borrowings and charging exorbitant interest rates from 40 to 220 percent. Such unethical and predatory lending practices have left millions entangled in a cyclical debt trap that has threatened their very lives and livelihoods. To date at least 170 persons have committed suicide due to being unable to repay their loans, evoking dark memories of the agricultural crisis two decades ago that saw hundreds of paddy farmers committing suicide due to being unable to sell their harvests for a price that covered their production costs.

epidemic proportions, affecting almost three million people island-wide. Once seen as an instrument of rural upliftment, microfinance loans have now gained notoriety for encouraging multiple borrowings and charging exorbitant interest rates from 40 to 220 percent. Such unethical and predatory lending practices have left millions entangled in a cyclical debt trap that has threatened their very lives and livelihoods. To date at least 170 persons have committed suicide due to being unable to repay their loans, evoking dark memories of the agricultural crisis two decades ago that saw hundreds of paddy farmers committing suicide due to being unable to sell their harvests for a price that covered their production costs.

Since gaining Independence in 1948, successive governments have initiated various poverty alleviation programmes such as food coupons, Janasaviya, Samurdhi, GamiDiriya, GramaShakthi and the current Gamperaliya and Enterprise Sri Lanka. These schemes have traditionally targeted the rural population, which remains the highest in Sri Lanka, with the last census in 2011 showing that 77 percent of people live outside urban areas. Furthermore, the World Bank has categorized Sri Lanka as a higher middle-income country based on its per capita income of over 4000 US dollars. If Sri Lanka is a higher middle-income country, and most of its population lives in rural areas, and most government programmes have aimed at rural upliftment, then the rural economy should be one of the strongest areas. But this is not the case.

Globally and in Sri Lanka microfinance had promised to boost income generation for the poor. It grew rapidly in the 1980s, and by 2006 had over 100 million recipients in 80 countries. This was the golden era of microfinance, prompting Nobel Laureate Muhammad Yunus to declare at the 1997 Washington Micro-credit Summit that microfinance could create a poverty-free world. In Sri Lanka microfinance has had a long history, providing coping options for the poor during economic shocks and personal difficulties. It accelerated after 2005, and studies show that in Sri lanka it grew 400 percent from 2000 to 2018. By then over 2.8 million citizens were on microfinance schemes, of which 2.4 million, or 84 percent, were women.

Most women borrowers are married with children, and they borrow to fulfill their daily consumption needs. The money rarely goes towards any livelihood development. Cash for healthcare, education, weddings, funerals, coming-of-age ceremonies and alms-givings are met by local microfinance loaners. And so microfinance’s promise of bringing start-up capital, credit and savings to the poor has proven to be a failed project.

According to the Central Bank (CB) a variety of institutions provide microfinance in Sri Lanka, such as licensed banks, licensed finance companies, Co-operative Rural Banks (CRB), Thrift and Credit Co-operatives Societies (TCCS), Divinaguma banks, microfinance companies and Non-Governmental Organisations (NGO). These are supposed to serve people who lack collateral to take loans from regular banks. So savings are not a precursor to accessing credit, and no background checks are conducted. Borrowers only need to produce their National Identity Card (NIC) to secure loans. This leads to multiple borrowings and accumulated debt, which inevitably exceeds household income. Predatory lending ensues, focusing on lending rather than saving. The motive is high interest rates with high-frequency installments, shifting microfinance from an investment model to a consumption model.

The crisis has seen many borrowers resorting to extreme measures to pay off their debt, like pawning their gold and jewellery. Additionally, there is the stigma and insecurity of male collectors invading female homes. Reports of sexual harassment and abuse abound, and such abusive behaviour by collectors has led to suicides as well.

A case in point is the debt crisis overtaking Karadikundru, a fishing village in the Kilinochchi District. The women of Karadikundru kept track of their loans by the day of the week. There was the Monday loan, Tuesday loan, Wednesday loan and so on.

Each loan had its own collector, and each collector represented one of the numerous microfinance organizations. Of the village’s 56 families, 30 are plagued by rising indebtedness. Unable to cough up a weekly average of Rs. 1500, the women have been blacklisted by the Sri Lanka Credit Information Bureau (CRIB). Some have been threatened with legal action. But unable to cope, the women simply refuse to pay. Their collective action has temporarily stopped the collectors. But they still remain trapped in a never-ending crisis of disempowerment and economic peril.

Part of the problem is that most microfinance companies function unregulated, even though required by law to register under the 2016 Microfinance Act. This makes keeping track of numbers in the non-banking financial sector virtually impossible, and even the Central Bank (CB) lacks exact figures. However, according to a UN estimate, backed by the government, at present about 15,000 microfinance organisations operate throughout the country. In contrast, the Microfinance Practitioners’ Association (MFPA) has just 64 registered organisations on their website.

Part of the problem is that most microfinance companies function unregulated, even though required by law to register under the 2016 Microfinance Act. This makes keeping track of numbers in the non-banking financial sector virtually impossible, and even the Central Bank (CB) lacks exact figures. However, according to a UN estimate, backed by the government, at present about 15,000 microfinance organisations operate throughout the country. In contrast, the Microfinance Practitioners’ Association (MFPA) has just 64 registered organisations on their website.

Most microfinance companies are registered under the Companies Act of 2007. Speaking to , Vidura Munasinghe of the Law and Society Trust (LST) said, “The MFPA accepts there are between 8000 to 10,000 microfinance organisations, but most are registered under the Companies Act. There are so many companies, we don’t really know what they are engaging in.”

The problem with the Microfinance Act is that registration is mandatory only for companies that accept deposits. Though microfinance companies deduct money from loans and retain them as savings, such deposits are overlooked and they continue to function unregistered. Further, many Non-Governmental Organizations (NGOs) also engage in the microfinance business. Presently, only one microfinance company and 13 NGOs are registered under the Microfinance Act.

There are three types of credit organisations. The first are known banks and financial institutions, which are increasingly moving from traditional lending to the more lucrative microfinance model. The second are microfinance wings operated by NGOs that also provide training and seek markets. The third are former bank agents or employees who form collectives and invest capital, and use their local networks to lure villagers. “Villagers don’t consider from whom they are borrowing. These are agents of established banks whose businesses have changed from banking to microfinance,” Mr. Munasinghe explained. In fact research shows that most borrowers have a poor understanding of the high interest rates extracted from them, and focus instead on paying their installments.

The answer to microfinance could lie in the co-operative movement, which began in Sri Lanka in the early 20th century when the British used them for agricultural policy and to distribute essential items. Farmers could take low-interest loans, which they could repay to avoid permanent indebtedness. In 1947, there were over 6,500 societies with 1.1 million members. The population then was 6.8 million.

From the 1950s to the 1970s co-operatives grew further as rural development and import substitution strengthened.

Even the World Bank (WB) stressed the importance of co-operatives for agricultural credit. “Cooperatives provide a large share of agricultural credit on reasonable terms,” the WB noted in the 1950s, adding that co-operatives effectively utilized resources to improve cultivation methods. It even recommended doubling the number of credit, marketing and producer co-operatives to save cultivators and fishermen from being exploited by traders and money lenders.

After 1956, Agriculture Minister Philip Gunawardena sought more state intervention for co-operatives. He promoted rural development through Multi-Purpose Co-operative Societies (MPCS) which carried out consumer services as well as provided agricultural credit. He also envisioned a centralised and state-owned co-operative development bank, and this materialized when the People’s Bank was formed in 1961, amalgamating capital in various rural co-operative banks. Although these policies helped co-operatives grow, they also made them more dependent on the state, which ultimately undermined the movement. After 1977, the mandate of the People’s Bank changed from providing financial support and credit to co-operatives to becoming a state-owned commercial bank without any relationship to the co-operatives.

In Jaffna, the British initiated credit co-operatives with leadership from the Vellala caste. Later, producer co-operatives were formed for lower caste occupations like fisheries and toddy tapping. These co-operatives, with their strong organizing and corelation to credit and consumer needs, thrived in the North. Furthermore, Jaffna’s vibrant educational and literate culture contributed to more co-operation, with teachers, principals and retired public servants joining the movement.

Jaffna had the first co-operative Central Bank, the first co-operative hospital, the first co-operative marketing society, the first co-operative union for agricultural producers, the first Harbour Services Union and the first District Fisheries Union. While nationally the state promoted co-operatives such as MPCSs, in Jaffna, co-operatives evolved with more autonomy.

Though co-operatives cannot fully resolve the rural economic crisis they can help reconstruct an alternative development vision and plan. In the Northern Province (NP), this involves providing considerable debt relief to those caught in the microfinance crisis. The Co-operatives Loan Scheme (CLS) aided by a Rs. 500 million grant from the Finance Ministry, and implemented through the network of co-operatives in the five Northern districts aims to mitigate the microfinance burden. The CLS involves the collaboration of CRBs, TCCSs, CB personnel and officials from the Northern Province Department of Co-operative Development (DCD).

The CLS offers a Rs. 20,000 loan which contrasts sharply with the microfinance model. It entails a 12-month payback period of monthly repayments at 14 percent interest rates. Each monthly installment of Rs. 1,800 is estimated as four days of income per month of a rural woman wage worker. Only one loan is granted per individual, with two guarantors. Guarantors can be from the same household, but must have an account with the lending CRB or TCCS. After 3 months of regular payments, one guarantor can apply for a loan with two new guarantors. The second guarantor can apply for a loan after 6 months, allowing a household to obtain Rs 60,000 in CLS loans annually. Each CLS recipient is asked to save at least Rs. 100 monthly at the co-operative’s current minimum savings rate. Of the total CLS loans disbursed, 75 percent go to women, and 25 percent are to new members. The credit has wide reach, covering 20,000 households across the NP.

In this backdrop, Daily Mirror, visited the Karainagar CRB in Jaffna to seek the views of CLS recipients on the new scheme. This is what they had to say:

Loheswaran Thanujah is 32-years-old and a mother of four. At night she engages in offshore fishing with her husband, catching prawns, crabs and fish. During the day she works in a crab factory, boiling, separating and packing crabs for a daily wage of Rs. 500. Her income from fishing varies from Rs. 3000 to Rs. 200 a day, depending on the catch. She either sells her catch to traders, or directly to customers at the Valathalei junction. “I used the CLS to buy 10 fishing nets. Earlier we had just one net. With a bigger loan we could buy 60 nets,” she said.

Loheswaran Thanujah is 32-years-old and a mother of four. At night she engages in offshore fishing with her husband, catching prawns, crabs and fish. During the day she works in a crab factory, boiling, separating and packing crabs for a daily wage of Rs. 500. Her income from fishing varies from Rs. 3000 to Rs. 200 a day, depending on the catch. She either sells her catch to traders, or directly to customers at the Valathalei junction. “I used the CLS to buy 10 fishing nets. Earlier we had just one net. With a bigger loan we could buy 60 nets,” she said.

K. Natgunarajah is 49-years-old, and has a son and daughter. He has been farming for over three decades, growing rice and ginger seasonally.  “Farming is not reliable because we solely depend on the rain as there are no rivers here,” he explained. He also breeds goats for milk, and used the CLS to buy a goat and a calf, which he estimates to be worth Rs. 45,000. Not having a permanent and steady income, Natgunarajah also hires out a tractor and three-wheeler when hard-pressed for money. He had no problem settling the CLS money, but said the amount was insufficient to cover his livelihood needs.

“Farming is not reliable because we solely depend on the rain as there are no rivers here,” he explained. He also breeds goats for milk, and used the CLS to buy a goat and a calf, which he estimates to be worth Rs. 45,000. Not having a permanent and steady income, Natgunarajah also hires out a tractor and three-wheeler when hard-pressed for money. He had no problem settling the CLS money, but said the amount was insufficient to cover his livelihood needs.

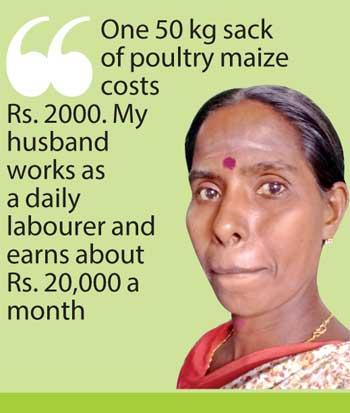

Sathgunanathan Susiladevi is 45-years-old and a mother of four. She has been running a poultry farm for 10 years. She obtained 50 chicks from a  Samurdhi livelihoods development scheme and used the CLS to build a shed and buy poultry maize. “One 50 kg sack of poultry maize costs Rs. 2000. My husband works as a daily labourer and earns about Rs. 20,000 a month. We sell about 20 eggs per day to traders,” she said, adding that they could repay the CLS money. However she needs extra income to extend their house and educate their children.

Samurdhi livelihoods development scheme and used the CLS to build a shed and buy poultry maize. “One 50 kg sack of poultry maize costs Rs. 2000. My husband works as a daily labourer and earns about Rs. 20,000 a month. We sell about 20 eggs per day to traders,” she said, adding that they could repay the CLS money. However she needs extra income to extend their house and educate their children.

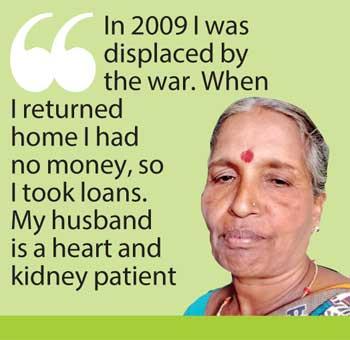

Ambalavan Vijeyalakshmi is 56-years-old and does multiple jobs to look after her invalid husband and two campus-going children. She runs a poultry farm, prepares coconut oil, weaves coconut leaves for thatching and also engages in crop-share paddy farming. She has taken six different microfinance loans and is Rs. 600,000 in debt. “In 2009 I was displaced by the war. When I returned home I had no money, so I took loans. My  husband is a heart and kidney patient and needed medicine,” she said. Vijeyalakshmi took more loans to repay her initial loans, and currently pays Rs. 40,000 a month in installments. “I took microfinance loans because unlike banks they didn’t ask for surety or endorsements from public servants. But now I’m trying to get out of this debt,” she said, adding that she hoped the CLS would help her achieve this.

husband is a heart and kidney patient and needed medicine,” she said. Vijeyalakshmi took more loans to repay her initial loans, and currently pays Rs. 40,000 a month in installments. “I took microfinance loans because unlike banks they didn’t ask for surety or endorsements from public servants. But now I’m trying to get out of this debt,” she said, adding that she hoped the CLS would help her achieve this.

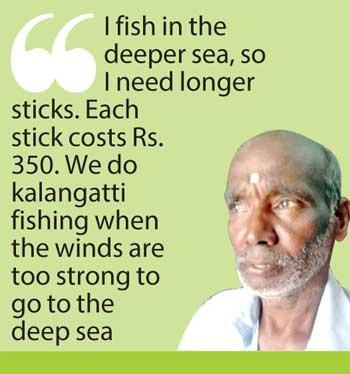

P. Ganeshu is 64-years-old, and has been fishing since he was 18. He does both offshore and deep sea fishing, and also some seasonal crop-share farming. He used the CLS to purchase nets and repair his 17-foot long motor boat, but said the Rs. 20,000 was not enough to cover all costs.  Ganeshu, who was displaced twice during the war, in 1990 and 2002, engages in kalangatti lagoon fishing, where fish are trapped in nets bound to sticks planted in the water. “I fish in the deeper sea, so I need longer sticks. Each stick costs Rs. 350. We do kalangatti fishing when the winds are too strong to go to the deep sea,” he explained. He earns between Rs. 20,000 to 30,000 a month, but his daily expenses average about Rs. 500. “I think the CLS should be more than Rs. 20,000, and there should be a rewards and incentives for those who make repayments on time,” he said.

Ganeshu, who was displaced twice during the war, in 1990 and 2002, engages in kalangatti lagoon fishing, where fish are trapped in nets bound to sticks planted in the water. “I fish in the deeper sea, so I need longer sticks. Each stick costs Rs. 350. We do kalangatti fishing when the winds are too strong to go to the deep sea,” he explained. He earns between Rs. 20,000 to 30,000 a month, but his daily expenses average about Rs. 500. “I think the CLS should be more than Rs. 20,000, and there should be a rewards and incentives for those who make repayments on time,” he said.

Jeyaratnam Wasantha Kumari is the manager of the Karainagar CRB which was established in 1972 under the People’s Bank. “The CRB was started to give loans and encourage low income earners to save,” she said. “Since 1990 it has come under the DCD. All members and employees are Karainagar locals, and we are part of the 1300 members of the MPCS covering nine GS divisions,” she added.

In addition to the CLS, the CRB grants different loans to fishermen, poultry and agriculture farmers as well as government servants. They grant short-term loans of Rs. 100,000 at 15 percent interest rates, repayable over two years. “We are flexible with repayments. We extend repayment periods without a penalty, but interest accumulates,” she explained, adding that about 10 percent of recipients default or delay on repayment.

The CRB also advices members on how to manage their savings. “When someone has over Rs. 10,000 in savings we encourage them to open Fixed Deposits (FD) at eight percent interest,” she said, adding that a minimum Rs. 100 is needed to open a savings account. Commenting on the CLS loan, she said, “We have given out 255 debt relief loans, of which only one person has not been able to repay the loan.” Ms Jeyaratnam said the CLS was helping the community who were suffering under microfinance debt, and they hoped to increase the loan to Rs. 50,000. “But this depends on available funds and approval from the MPCS board,” she said.