27 Jan 2025 - {{hitsCtrl.values.hits}}

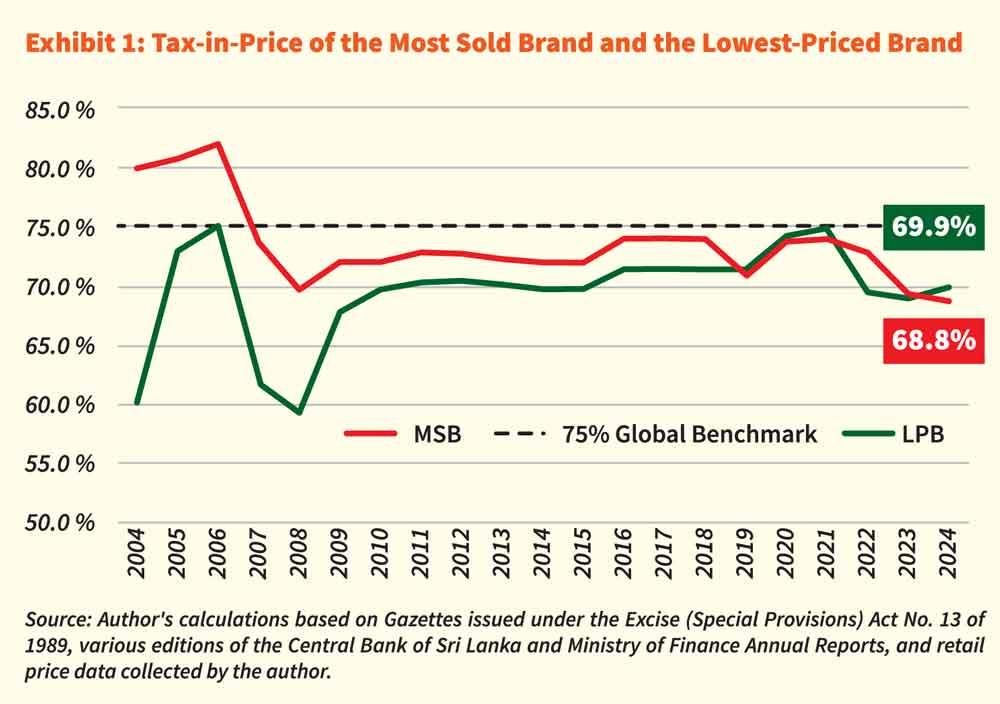

The tax-in-price for cigarettes in Sri Lanka has reduced dramatically since 2020, falling below both the international benchmark of 75 percent and past norms in Sri Lanka. It fell to 68.8 percent for the most sold brand (MSB) and 69.9 percent for the lowest priced brand (LPB). Rs.9.4 billion in tax revenue was lost in 2024 on the MSB alone and transferred instead as profit to the producer.

The tax-in-price for cigarettes in Sri Lanka has reduced dramatically since 2020, falling below both the international benchmark of 75 percent and past norms in Sri Lanka. It fell to 68.8 percent for the most sold brand (MSB) and 69.9 percent for the lowest priced brand (LPB). Rs.9.4 billion in tax revenue was lost in 2024 on the MSB alone and transferred instead as profit to the producer.

This insight updates an analysis published in 2018 titled ‘The Hidden Side of Cigarette Pricing’ (de Mel, Fernando, & Munas, 2018). It revealed that, from 2014 to 2016, the net-of-tax price per cigarette increased at a much faster rate than the tax-in-price per cigarette. This insight extends the analysis to cover the period from 2017 to 2024.

Tax-in-price refers to the tax levied on a cigarette, expressed as a percentage of price. This accrues to the government. Net-of-tax price is the selling price minus the tax-in-price. It is the revenue from the cigarette that accrues to the supply chain.

The government’s revenue loss is not a result of excessively high taxes on cigarettes; rather, it is due to what has been shown here as the double ambush on cigarette taxation – which then increases the profits of the producer at the expense of government revenue

This insight finds a significant reduction in the tax-in-price of cigarettes, occurring primarily after 2020—during the economic crisis and alongside the International Monetary Fund programme. In contrast, the tax-in-price of other products subjected to Value Added Tax (VAT) more than doubled during the same period.

Drunken man syndrome in cigarette taxation

In the last four years, Sri Lanka’s policies on cigarette taxation have been akin to Martin Luther’s allegory of a drunkn man, who, after falling off his horse on one side, clambers back up on the horse, only to fall off it on the other.

After having ‘fallen’ and lapsing for almost 25 years to make adequate increases in cigarette prices, Sri Lanka ‘clambered back up’ to align the price of the MSB with its targeted affordability benchmark. However, in doing so, it ‘fell off the other side’ by ceding the benefit of the price increase to the producer’s profits at the expense of government revenue. This was by allowing the tax-in-price of the MSB to reduce from 74.0 percent in 2016 to 68.8 percent by 2024, falling short of the benchmark tax-in-price of 75 percent recommended by the World Health Organisation (WHO) and United Nations Development Programme (UNDP).

In the case of the lowest-priced brand (LPB) of cigarettes, tax policies fell off both sides of the allegorical horse at the same time. In 2020, the LPB’s price was significantly below the affordability benchmark price (adjusted for length) and the tax-in-price stood at just 71.4 percent. By 2024, both these policy mistakes were compounded: the LPB became even more affordable (falling off on one side) and its tax-in-price reduced further to 69.9 percent (falling off on the other side as well).

This reduction in cigarette taxes has resulted in a significant revenue loss. In 2024, just the MSB, accounted for over half of the total sales of cigarettes. The calculated revenue lost from the under-taxation of it was Rs.9.4 billion.

Economic goals of cigarette taxation

Globally, there is consensus on two simple goals of cigarette taxation. One is to reduce consumption, in line with economic and health policy goals, by maintaining or reducing the affordability of cigarettes. Two is to achieve the global benchmark target for the percentage of the tax in the price of a cigarette (tax-in-price). The methods to achieve these goals have been extensively studied and are supported by a plethora of research publications, both internationally and within Sri Lankan universities and think tanks.

Twofold policy failure

The analysis in the next section, supported by precise calculations, illustrates how Sri Lanka has failed to meet both of the above economic goals of cigarette taxation.

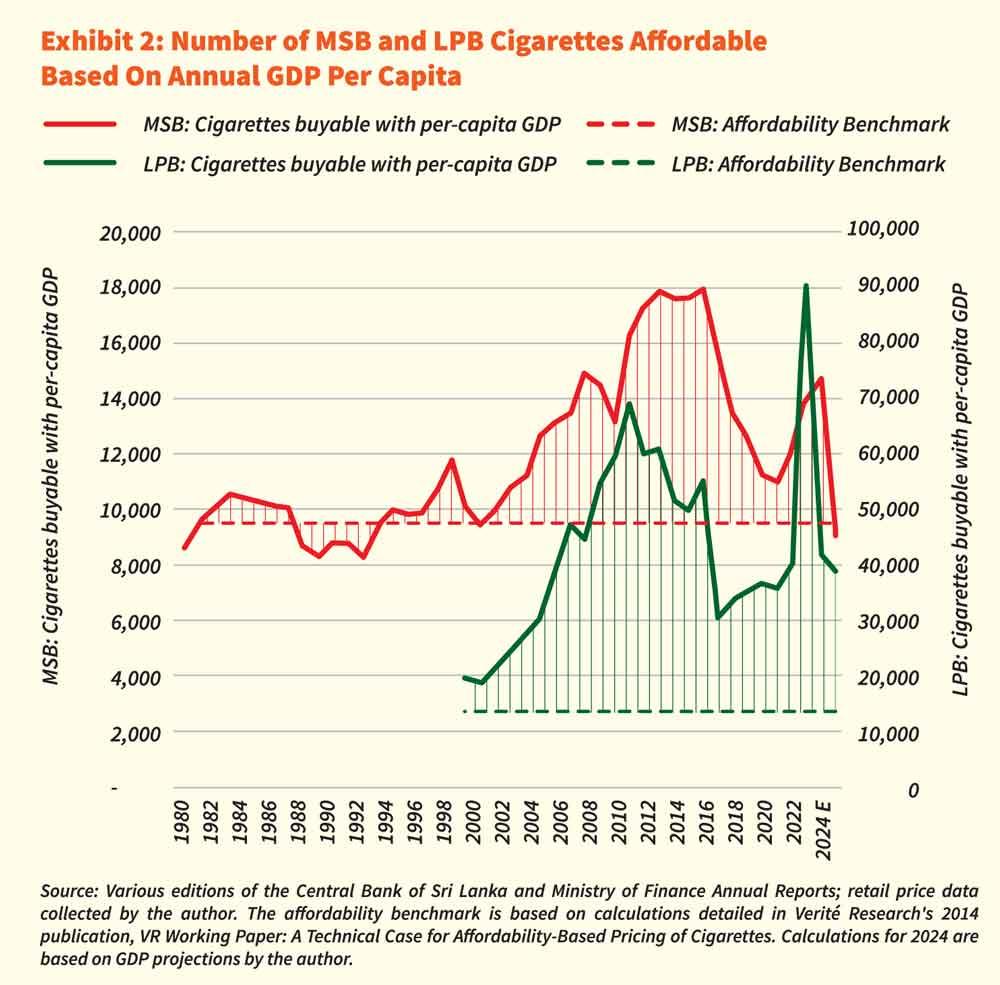

The first goal of reducing/maintaining affordability was achieved for the MSB in 2024, after two decades of radically increased affordability. However, other cigarette brands remain significantly more affordable, that is, well below their benchmark price – which is to have the same price per unit of length as the MSB.

The lower price per unit-length compared to the MSB, has led to the collective market share of non-MSB cigarettes more than doubling in the past seven years, as consumers are encouraged to switch their consumption from the MSB cigarette to other cigarettes that are kept relatively underpriced. Data shows that the MSB’s market share, which ranged between 79 percent and 88 percent (averaging 82.7 percent) between 2010 and 2018, declined drastically in the next five years to 53.7 percent by 2023.

Such gaming of tax policy, by cigarette manufacturers, is well-documented in the literature. It is why the WHO Framework Convention on Tobacco Control (FCTC) recommends reducing or eliminating multiple tax bands on cigarettes. This recommendation has been echoed by various Sri Lankan organisations, including the Institute of Policy Studies, regarding the five different tax bands on cigarettes in Sri Lanka (IPS, 2022).

The second goal of achieving a benchmark target for the tax-in-price was significantly advanced in 2016, due to a determined position taken by the then-president. However, the analysis reveals significant regression since then and especially after 2020. While the tax-in-price for most products subject to VAT has more than doubled since the economic crisis for cigarettes, it has actually decreased.

The tax-in-price can reduce because the excise tax is levied as a specified amount, unlike VAT and TT, which are levied as a percentage of price. Therefore, the percentage of excise tax-in-price decreases as the price increases—unless the excise tax is increased to match the price increase.

This means that, in addition to consumption being shifted to the radically underpriced cigarettes, the tax revenue share from each cigarette was also reduced – diminishing government revenue in two ways. Moreover, the data shows that profits for the producer have increased due to the higher net-of-tax price, at the government’s expense.

Double ambush: What the data reveals is a double ambush on government revenue from cigarettes: (1) the tax-in-price was reduced on all cigarettes and (2) market share shifted to cigarettes on a lower tax band, which are marketed at a lower price per unit length than the MSB.

As a result of this double ambush, the government is set to collect less revenue from cigarette taxes in 2024 compared to 2023. Cigarettes may be the only product in the market where tax revenue has declined in 2024, while the supplier’s revenues and profits have increased.

Movements in affordability relative

to benchmark

The theoretical basis for the affordability benchmark for the MSB, used by the National Authority of Tobacco and Alcohol (NATA), was published in a 2014 working paper based on historical data from 1980 (de Mel & Fernando, 2014).

MSB: The benchmark affordability level was constructed around the MSB, using the actual affordability level maintained in the 20-year period between 1980 and 2000 (with limited deviation). After that, the deviations escalated, making it much more affordable. The benchmark affordability level was achieved again only in 2024 (see Exhibit 2).

LPB: The benchmark affordability levels for other cigarettes are calibrated to the MSB by setting the price of other cigarettes relative to the price of the MSB to be the same as their length relative to the length of the MSB. It means, for example, that a cigarette that is half the length of the MSB should be not less than half the price of the MSB. The LPB also increased in affordability after the turn of the century; however, unlike the MSB, it has not reverted to the benchmark affordability level. Instead, its affordability has increased radically since 2017, the period evaluated in this insight (see Exhibit 2).

Movements of tax-in-price relative

to benchmark

In July 2018, Verité Research published an insight titled ‘The Hidden Side of Cigarette Pricing: A Case Study on Sri Lanka’ (de Mel, Fernando, & Munas, 2018). It showed that from 2014 to 2016, the monopoly producer of cigarettes in Sri Lanka raised prices much faster than the government raised taxes, which led to a reduction in the tax-in-price during that period. This insight updates the analysis from 2017 to the end of 2024, extending the tax-in-price analysis over a full decade.

For cigarettes, the benchmark for tax-in-price – the percentage of the price of a cigarette that should be collected in taxes – is set at 75 percent. This internationally recognised standard for tobacco taxation has been developed and published for all countries by the World Bank (Jha & Chaloupka, 1999), World Health Organisation (WHO, 2010, 2014, 2015, 2017, 2019, 2021) and United Nations Development Programme (UNDP and WHO, 2019). It is also supported by the FCTC, a global treaty of the WHO, to which Sri Lanka became a signatory in 2003 (de Mel, Fernando, & Munas, 2018).

Updated evaluation: from 2017 to 2024

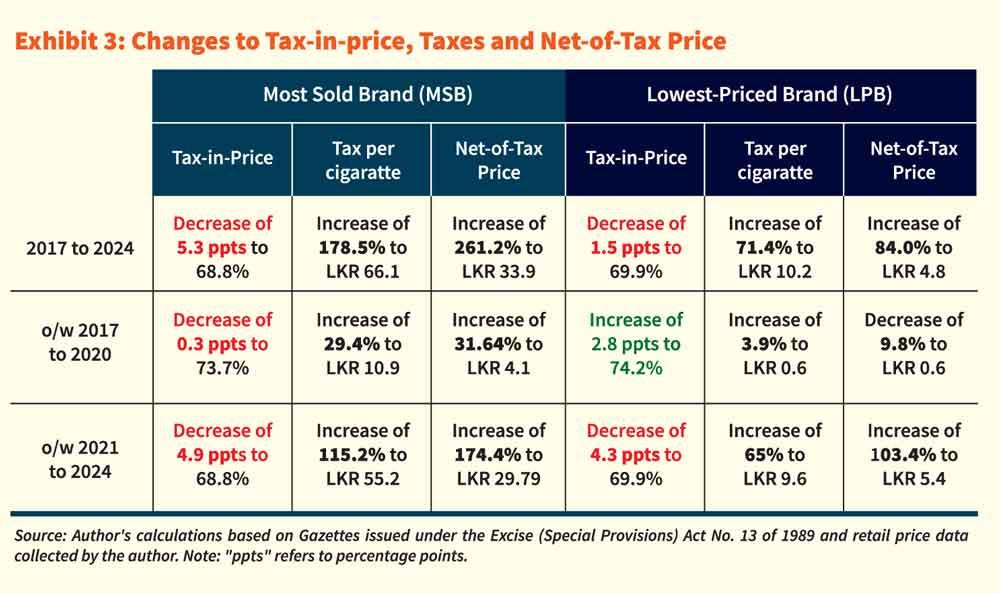

The data and evaluation described in this section are summarised in Exhibit 3.

MSB cigarette: During this period, the tax-in-price of the MSB reduced from 74.0 percent to 68.8 percent. The MSB cigarette thus benefitted from a tax reduction of 5.2 percentage points on the price. As a result, the company’s profits increased at the expense of revenue to the government. While the price of the MSB cigarette increased by 200.0 percent, the total taxes on that cigarette rose by only 178.5 percent.

In 2024 alone, the government lost Rs.9.4 billion in revenue from the reduction of the tax-in-price on the MSB cigarette. This entire amount is effectively a direct transfer from the government to the profits of the producer. Sales data available up to September of the year was annualised to arrive at the full estimate for 2024.

LPB cigarette: The tax-in-price for the LPB decreased from 71.4 percent to 69.9 percent during this period. Therefore, the LPB cigarette received a tax reduction of 1.5 percentage points on the price. As with the MSB, this reduction of the tax-in-price boosted the profits of the producer, at the expense of revenue to the government. The price of the LPB increased by 75.0 percent while the tax on the cigarette rose by only 71.4 percent.

Most backsliding after 2020: The data indicates that the most significant backsliding in achieving a tax-in-price close to the benchmark levels occurred after 2020, precisely when the Sri Lankan economy was going into crisis and the government was in dire need of more revenue.

From 2017-2020: The tax-in-price for the MSB decreased only slightly from 74.0 percent to 73.7 percent, while for the LPB, it increased from 71.4 percent to 74.2 percent, bringing it closer to the policy benchmark of 75 percent.

From 2021-2024: The tax-in-price for the MSB decreased significantly from 73.7 percent to 68.8 percent, a reduction of 4.9 percentage points. Similarly, for the LPB, the tax-in-price reduced from 74.2 percent to 69.9 percent, a decline of 4.3 percentage points.

At the time of writing this insight, popular media has carried opinions stating that the government is losing revenue due to taxes on cigarettes being too high. This insight shows that such claims have got the analysis of cigarette taxation policy precisely upside down. The government’s revenue loss is not a result of excessively high taxes on cigarettes; rather, it is due to what has been shown here as the double ambush on cigarette taxation – which then increases the profits of the producer at the expense of government revenue.

The consequence of this double ambush can be quantified from numbers in annual reports of the monopoly producer, Ceylon Tobacco Company (CTC). They show that from 2017-2024 levies paid to the government on cigarettes (including taxes on tobacco leaf) increased by 27.5 percent. In contrast, the net-of-tax revenue for CTC (total revenue minus government levies) increased by 92.4 percent.

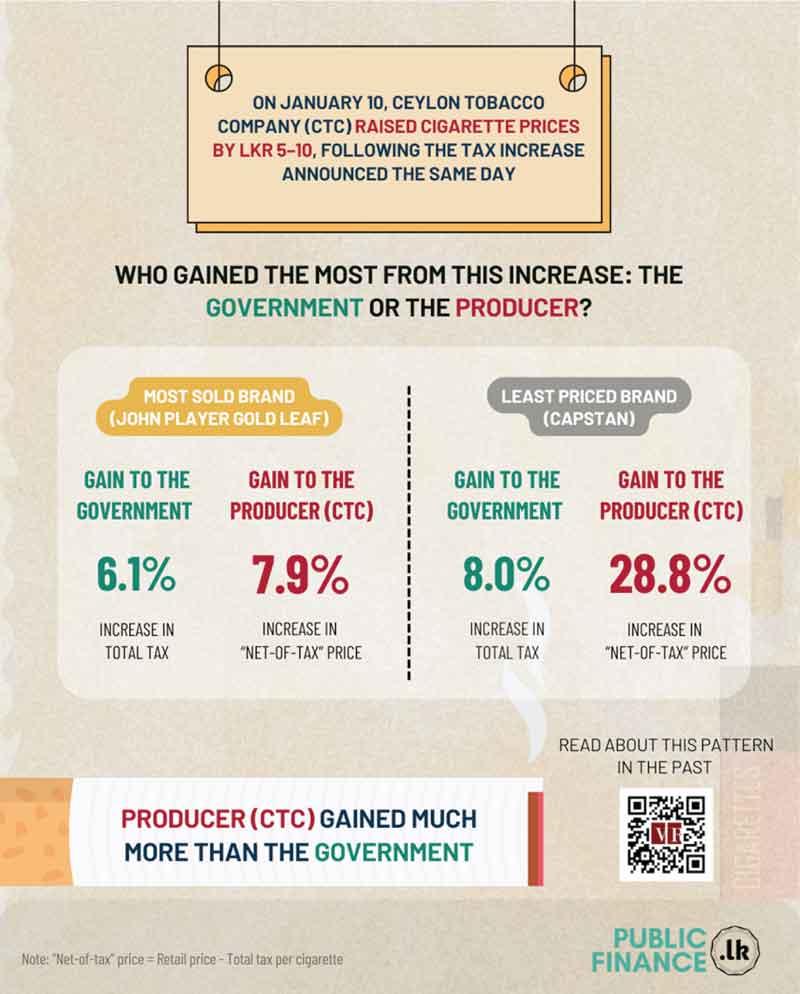

As this insight is being finalised for publication, the excise tax levy for all categories of cigarettes have been increased by 5.9 percent. In turn, CTC has increased retail prices by Rs.5 for the LPB and Rs.10 for the MSB.

Therefore, this has not taken the government any closer to achieving its second goal. In fact, it has resulted in a further tax-in-price decrease for both MSBs (from 68.8 percent to 68.4 percent) and LPBs (from 70.0 percent to 66.1 percent). That is because the net-of-tax price for LPBs increased by 28.8 percent, while the total tax on them (including VAT) increased by only 8.0 percent.

17 Jun 2026 6 hours ago

17 Jun 2026 6 hours ago

17 Jun 2026 7 hours ago

17 Jun 2026 7 hours ago

17 Jun 2026 8 hours ago