Reply To:

Name - Reply Comment

Last Updated : 2024-04-19 21:46:00

29 April 2013 06:30 pm - 0 - {{hitsCtrl.values.hits}}

.jpg) Rubber industry analysts have said some time ago that, natural rubber (NR) prices are likely to take a dip after 2012 due to the acceleration in normal production on account of massive new planting undertaken across the major natural producing countries of the world during 2005-08. This effect, however, will taper off after 2020.

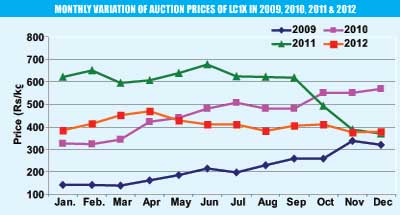

Rubber industry analysts have said some time ago that, natural rubber (NR) prices are likely to take a dip after 2012 due to the acceleration in normal production on account of massive new planting undertaken across the major natural producing countries of the world during 2005-08. This effect, however, will taper off after 2020. New planting

New planting Sharp fluctuations in commodity prices, which are not unique to rubber (See figures 1 & 2), are creating significant business challenges that can affect virtually everything from production costs and product pricing to earnings and credit availability.

Sharp fluctuations in commodity prices, which are not unique to rubber (See figures 1 & 2), are creating significant business challenges that can affect virtually everything from production costs and product pricing to earnings and credit availability.

Add comment

Comments will be edited (grammar, spelling and slang) and authorized at the discretion of Daily Mirror online. The website also has the right not to publish selected comments.

Reply To:

Name - Reply Comment

On March 26, a couple arriving from Thailand was arrested with 88 live animal

According to villagers from Naula-Moragolla out of 105 families 80 can afford

Is the situation in Sri Lanka so grim that locals harbour hope that they coul

A recent post on social media revealed that three purple-faced langurs near t