Reply To:

Name - Reply Comment

Last Updated : 2024-04-23 22:35:00

16 August 2013 04:12 am - 1 - {{hitsCtrl.values.hits}}

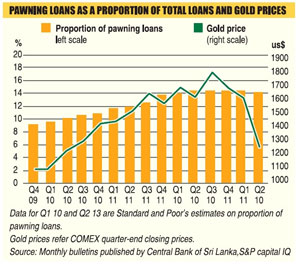

Loose regulatory guidelines with regard to gold-backed loans have been identified a key contributor to a ‘runaway growth’ in pawning loans, exposing the Sri Lankan banking industry to higher loan defaults, international credit agency Standard & Poor’s (S&P) said in a special report.

Loose regulatory guidelines with regard to gold-backed loans have been identified a key contributor to a ‘runaway growth’ in pawning loans, exposing the Sri Lankan banking industry to higher loan defaults, international credit agency Standard & Poor’s (S&P) said in a special report. “Such regulations make banks vulnerable to volatility in gold prices during the restricted period.”

“Such regulations make banks vulnerable to volatility in gold prices during the restricted period.”Lynette Friday, 14 March 2014 03:31 AM

Greetings from Carolina! I'm bored to tears at work so I decided to browse

your website on my iphone during lunch break.

I love the info you provide here and can't wait to take a look when I

get home. I'm surprised at how quick your blog loaded on my phone ..

I'm not even using WIFI, just 3G .. Anyhow, amazing site!

Add comment

Comments will be edited (grammar, spelling and slang) and authorized at the discretion of Daily Mirror online. The website also has the right not to publish selected comments.

Reply To:

Name - Reply Comment

On March 26, a couple arriving from Thailand was arrested with 88 live animal

According to villagers from Naula-Moragolla out of 105 families 80 can afford

Is the situation in Sri Lanka so grim that locals harbour hope that they coul

A recent post on social media revealed that three purple-faced langurs near t