Reply To:

Name - Reply Comment

Last Updated : 2024-04-23 17:11:00

8 June 2020 03:09 am - 1 - {{hitsCtrl.values.hits}}

Black economy, Tax evasion, Prevention of Money Laundering Act

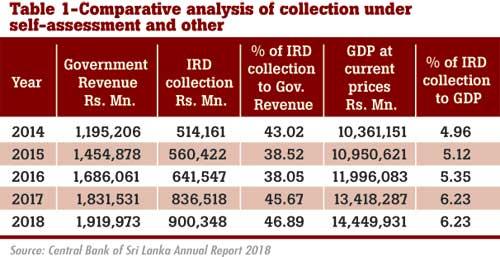

In the year 2018, the Gross Domestic Product (GDP) of Sri Lanka is Rs. 14,449,931 million and the contribution of  the Department of Inland Revenue (IRD) for the GDP was Rs.900, 348 Million and Revenue collection of the Department of Inland Revenue as a percentage of GDP is 6.23 for the said year. Following figures show the revenue for the last five years’ period ending from 2018

the Department of Inland Revenue (IRD) for the GDP was Rs.900, 348 Million and Revenue collection of the Department of Inland Revenue as a percentage of GDP is 6.23 for the said year. Following figures show the revenue for the last five years’ period ending from 2018

Accordingly, it is seen that as the main revenue collector of the government, Inland Revenue’s tax collection hovered around 5 per cent of the GDP and there is a declining trend if we peruse the records from the 1990s onwards.

On the other hand, the tax collection as a percentage of the GDP is far less when it is compared with that of the other Asian countries to their GDP as well as with the developed countries in the world. The following table of figures shows the tax/GDP ratio of the other countries.

Source: data.worldbank.org

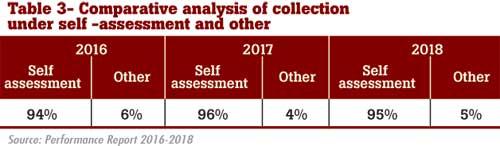

When the total tax collection is analysed further, it can be divided into two categories as self-assessment and “the other”. Self-assessment means the taxes paid by the taxpayers on their own to the banks and the “other” category includes the taxes collected by way of investigations and the arrears collection of taxes for previous years. The table below shows it as follows.

When the total tax collection is analysed further, it can be divided into two categories as self-assessment and “the other”. Self-assessment means the taxes paid by the taxpayers on their own to the banks and the “other” category includes the taxes collected by way of investigations and the arrears collection of taxes for previous years. The table below shows it as follows.

Source: Performance Report 2016-2018

At a glance of the above figures, one can see that the taxes collected by way of investigations by the IRD (“other”) are trivial when it is compared to the collection of taxes by way of self-assessment paid by the taxpayers on their own. On the other hand, the cost of the tax collection has gone up rapidly over the last two decades. Table 5 shows the cost of tax collection for the period from 2012 to 2018

Source: Performance reports of the Department of Inland Revenue

Above table -5 shows the productivity ratio of the IRD. That is to collect Rs 100/=, the expenditure is 36 cents in 2012 and the said ratio in the year 2018 was 58 cents. There is a considerable increase in the context of expenditure with regard to the collection of taxes over 7 years from 2012 to 2018.

There was a cadre of 875 officers in the executive grade as at 31/12/2009 and the said number of officers was increased to 1232 as at 31/12/2014. It was a considerable increase made to increase the tax collection among other things. The cadre in the grade of executive-level shows a 51.89% increase since 2009. This is a good omen from the aspect of officers in the Inland Revenue but it does not show output wise result as a whole.

Physical infrastructure facilities such as computers and other facilities required for the performance of duties have been provided. Performance reports of the IRD show that capacity building programs of officials have also been provided in foreign countries immensely.

There are many reasons for this declining trend in government tax revenue despite the overall increase in GDP and per capita income over the last two decades. According to the Report of the Taxation Commission 1990, some of the reasons are as follow;

Unplanned ad hoc tax incentives in the form of various tax holidays, relief and concessions, duty waivers.

Narrow tax base and coverage, the total number of taxpayers being about 3% of the population;

Increase in allowable expenses under the provisions of the Inland Revenue Act;

The existence of a large informal economy resulting in large scale tax evasion and avoidance.

In recent years, there has been a growing interest in what is now popularly termed as an underground economy that financial activities in the underground economy are described by a variety of terms such as informal, parallel, unofficial, and black etc.

-The informal credit market or the extent of black money has been estimated at approximately Rupees 13billion or about 6per cent of GDP. It is difficult in the absence of relevant data to quantify, on a definite basis the quantum of foreign money held undeclared by resident persons abroad or the informal foreign exchange market and the entire underground economy.

A complicated tax system and weakness in tax administration and the administrative mechanism

Black Economy

Black EconomyAccording to the aforesaid reasons, underground economy and the narrow tax base are prominent and the tax base may have been narrowed because of the large amount of money transactions taking place without coming to eyes of the tax authorities. It is a common knowledge that in the context of the present-day world, there is a shadow economy apart from the visible economy.

The black economy is a situation where the money earned by way of illegal methods and which are not declared for tax purposes.

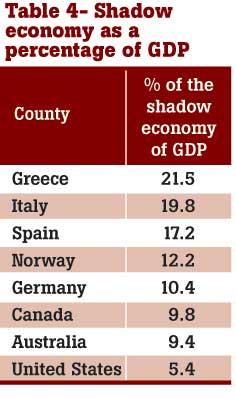

The shadow economy is a situation where work is done for cash to avoid incurring tax and without following standard business practices. In such a situation, the government has no control over them because their dealings in trade are not recorded. As a result, revenue authorities have no clue concerning such a segment of persons. This could be anything from paying tradesman for a baby doll in undeclared cash to the illegal drug trafficking or arms dealings, counterfeit trade and money laundering. The World Economic Forum’s (WEF) council on illicit trade 2012-2014 estimates the global shadow economy to be worth US Dollars 650 billion. Shadow economy as a percentage of GDP in selected Countries (2017) will give a gross idea about the issue at present.

In that context, it is seen that all over the world shadow economy or the black economy prevail unabated willingly  or unwillingly. Sri Lanka is not an exception. Tax evasion in Sri Lanka is not a new phenomenon. The 1955 taxation Commission referred to the prevalence of widespread evasion and remarked that “when evasion is widespread it brings the whole system into disrepute and even the honest man is tempted to conceal his true income and delay payment as much as possible. The 1966 Taxation Inquiry Commission also carried a reference to the prevalence of widespread evasion and added that the precise extent of evasion is impossible to assess. According to the Report of the taxation Commission, 1990 the share of the informal market accounted for 6 per cent as at the end of 1989. The informal economy goes hand in hand with the tax evasion. Therefore shadow economy or the underground economy where tax evasion is rampant is an area where tax authorities are supposed to pay attention to a high priority.

or unwillingly. Sri Lanka is not an exception. Tax evasion in Sri Lanka is not a new phenomenon. The 1955 taxation Commission referred to the prevalence of widespread evasion and remarked that “when evasion is widespread it brings the whole system into disrepute and even the honest man is tempted to conceal his true income and delay payment as much as possible. The 1966 Taxation Inquiry Commission also carried a reference to the prevalence of widespread evasion and added that the precise extent of evasion is impossible to assess. According to the Report of the taxation Commission, 1990 the share of the informal market accounted for 6 per cent as at the end of 1989. The informal economy goes hand in hand with the tax evasion. Therefore shadow economy or the underground economy where tax evasion is rampant is an area where tax authorities are supposed to pay attention to a high priority.

Tax evasion can take diverse forms. These include non-declaration or under-declaration of income and assets, over-statement of expenditure or exemptions, fictitious expenses, concealment of sales, stocks, and debtors, fictitious creditors etc. Tax evasion is a violation of the tax laws, where a taxable person reduces the tax liability by illegal means. This may be accompanied by the deliberate omission of income or turnover, the fraudulent claims of expenses and allowances. There are some amounts of persons in the informal sector who are not filing tax returns at all. Anyway, tax evasion can give two results. One is the loss of revenue for the state. Second is the evaded income which is spent on goods and services and thereby generates inflationary pressure and raises the prices of real property. It also distorts the fundamental objectives of a fair and equitable tax system.

Tax avoidance, on the other hand, denotes tax saving through legal means. Tax avoidance has been defined as the “art of dodging without actually breaking the law”. In an extended meaning, the term is used to describe the tax-saving by the adoption of various tax sheltering devices.

These devices take the form of artificial arrangements of personal and business affairs to take advantage of loopholes or anomalies in the law. Reducing the payment of tax should not be encouraged either by evasion or avoidance. But one cannot be stopped if he or she uses the mechanism to reduce payment of taxes by avoidance by using the loopholes in the mechanism.

"The shadow economy is a situation where work is done for cash to avoid incurring tax and without following standard business practices. In such a situation, the government has no control over them"

Nevertheless, there is a close connection between these two terms but at the same time, there is a considerable difference as well. According to Denis Winston Healey, “the difference between tax avoidance and tax evasion is the thickness of a prison wall.

According to economists, the Sri Lankan economy consists of a considerable amount of shadow economy or a black economy where a considerable amount of the trade transactions are not recorded and they bypass the tax authorities. It is in this background that the Government has introduced an Act to prevent money laundering in Sri Lanka.

The Prevention of Money Laundering Act No. 5 of 2006 provides the necessary measures to combat and prevent money laundering and provides for matters connected therein or incidental thereto. Taking action by the government to enact a law to prevent money laundering itself proves that there is money laundering where there are a black economy and tax evasion. This article attempts to evaluate how the tax evaders in the shadow economy are tackled by using the existing tax laws in the process of implementing the laws introduced to prevent money laundering in the country.

The Prevention of Money Laundering Act No. 5 of 2006 provides the necessary measures to combat and prevent money laundering and provides for matters connected therein or incidental thereto. Taking action by the government to enact a law to prevent money laundering itself proves that there is money laundering where there are a black economy and tax evasion. This article attempts to evaluate how the tax evaders in the shadow economy are tackled by using the existing tax laws in the process of implementing the laws introduced to prevent money laundering in the country.

The tax evasion on a large scale diminishes public respect and jeopardises the system. It is unfair to the honest taxpayers who must, as a result, bear a larger share of the tax burden. Therefore the tax administration must take concerted measures to curb the incidence of tax evasion. Money laundering is a threat to the good functioning of a financial system.

Though the Prevention of Money Laundering Act has no direct authority given to the Inland Revenue, the legal statutes enacted by the state to prevent the money laundering can be effectively used by the Inland Revenue in the process of taxing the person who is evading tax payments in the country.

Central Bank of Sri Lanka(CBSL) bond scandal which is also referred to as CBSL scam was a financial laundering scam which happened on 27 February 2015 and caused losses of more than US Dollars 11 Million to the nation. The bond scam is also regarded as the largest reported scam in Sri Lanka. During the inquiry of bond Commission, it was transpired that the crucial issues such as tax evasion, money laundering, bank malpractices, must be addressed by regulatory agencies such as the CBSL and Inland Revenue Department. To date, these agencies do not appear to have demonstrated any interest in addressing these issues. There are various cases of money laundering situations reported in the printed and electronic media and criminal High Courts in the Country.

Infamous VAT fraud case which was heard in the Colombo High Court involved a sum of Rs. 357 Million and during which time it was transpired in the High Court that the accused had purchased numerous immovable properties using the proceeds fraudulently obtained from the Department of inland Revenue. In the case of Infamous drug dealer Wele Suda, it was transpired that large sums of monies earned by sale of illegal drugs and it was transpired that several lands had been purchased by using illegal money. These are classic examples to be considered under the Money laundering Act and tax evasion and there are no reports available to say that tax evasion case has been filed in courts after the 1990s.

The writer is an Attorney At Law and Former Assistant Commissioner, Dept. of

Inland Revenue

Econ-Mutt Tuesday, 09 June 2020 08:21 AM

There are so many "Way Forwards" but, I am sure we will go "Backwards"

Add comment

Comments will be edited (grammar, spelling and slang) and authorized at the discretion of Daily Mirror online. The website also has the right not to publish selected comments.

Reply To:

Name - Reply Comment

On March 26, a couple arriving from Thailand was arrested with 88 live animal

According to villagers from Naula-Moragolla out of 105 families 80 can afford

Is the situation in Sri Lanka so grim that locals harbour hope that they coul

A recent post on social media revealed that three purple-faced langurs near t