Reply To:

Name - Reply Comment

Last Updated : 2024-04-25 06:31:00

1 April 2014 05:21 am - 1 - {{hitsCtrl.values.hits}}

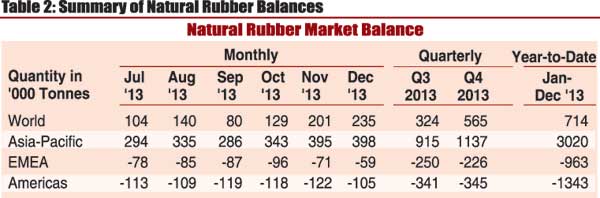

.jpg) A recent report released (March) by the International Rubber Study Group (IRSG) indicates that the stock balance of the global natural rubber industry at the end of 2013, specifically that of the Asia Pacific region, is in a position of production exceeding that of consumption by 3,020,000 tonnes, which may be a worrying factor to the producers in terms of natural rubber (NR) prices in the immediate future.

A recent report released (March) by the International Rubber Study Group (IRSG) indicates that the stock balance of the global natural rubber industry at the end of 2013, specifically that of the Asia Pacific region, is in a position of production exceeding that of consumption by 3,020,000 tonnes, which may be a worrying factor to the producers in terms of natural rubber (NR) prices in the immediate future.

sanjeewaw Saturday, 21 February 2015 09:54 PM

Dear Sir,Do you have the figure of Global Rubber Industries by Sectors?This is for my acedemic use.Thanks!Sanjeewa Weerakkodi

Add comment

Comments will be edited (grammar, spelling and slang) and authorized at the discretion of Daily Mirror online. The website also has the right not to publish selected comments.

Reply To:

Name - Reply Comment

US authorities are currently reviewing the manifest of every cargo aboard MV

On March 26, a couple arriving from Thailand was arrested with 88 live animal

According to villagers from Naula-Moragolla out of 105 families 80 can afford

Is the situation in Sri Lanka so grim that locals harbour hope that they coul